Could it pay to play defense?

Could it pay to play defense?

“Defense, defense, defense!” I shout watching the Knicks try to make it to game 7. The chant heard at all ball games is one with multiple meanings. Because it’s not just defense, but defense to find the opportunity for offense.

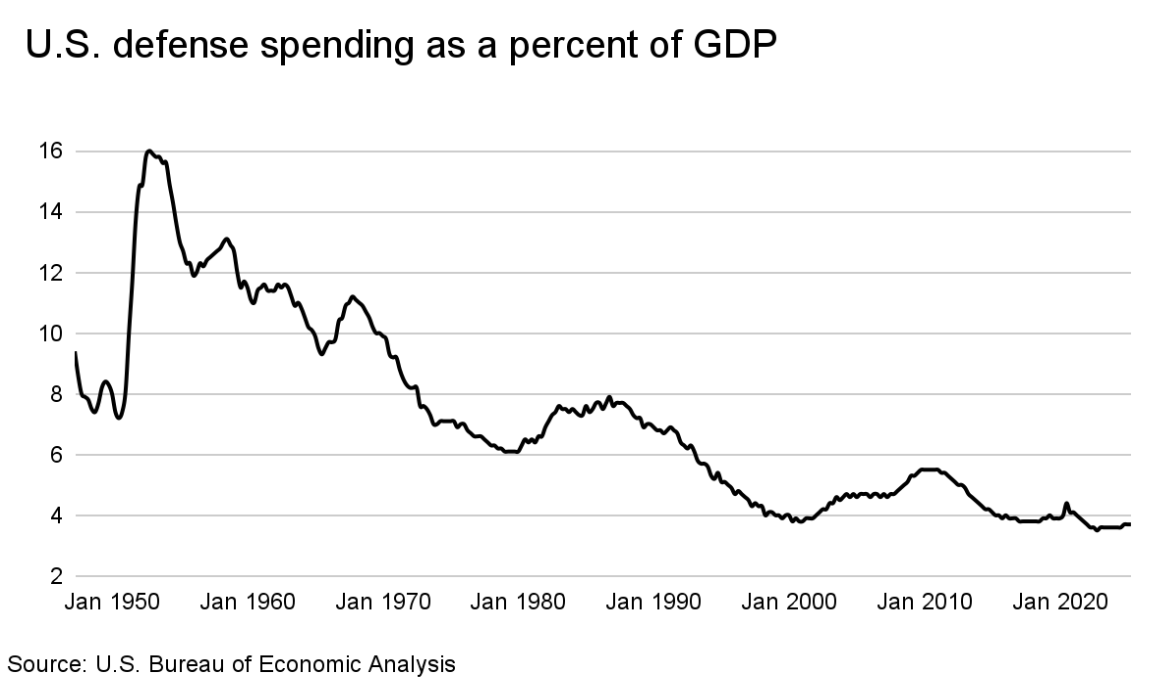

In the US, defense—and spending on it—has not been a focus in decades. We’ve actually spent within the same range on defense, as a % of GDP, since around 2000. When the federal deficit began moving to a surplus status in the late 90s, it was partly because of what was called the peace dividend. The end of the Cold War brought about a perception that defense spending could be cut—and so it was.

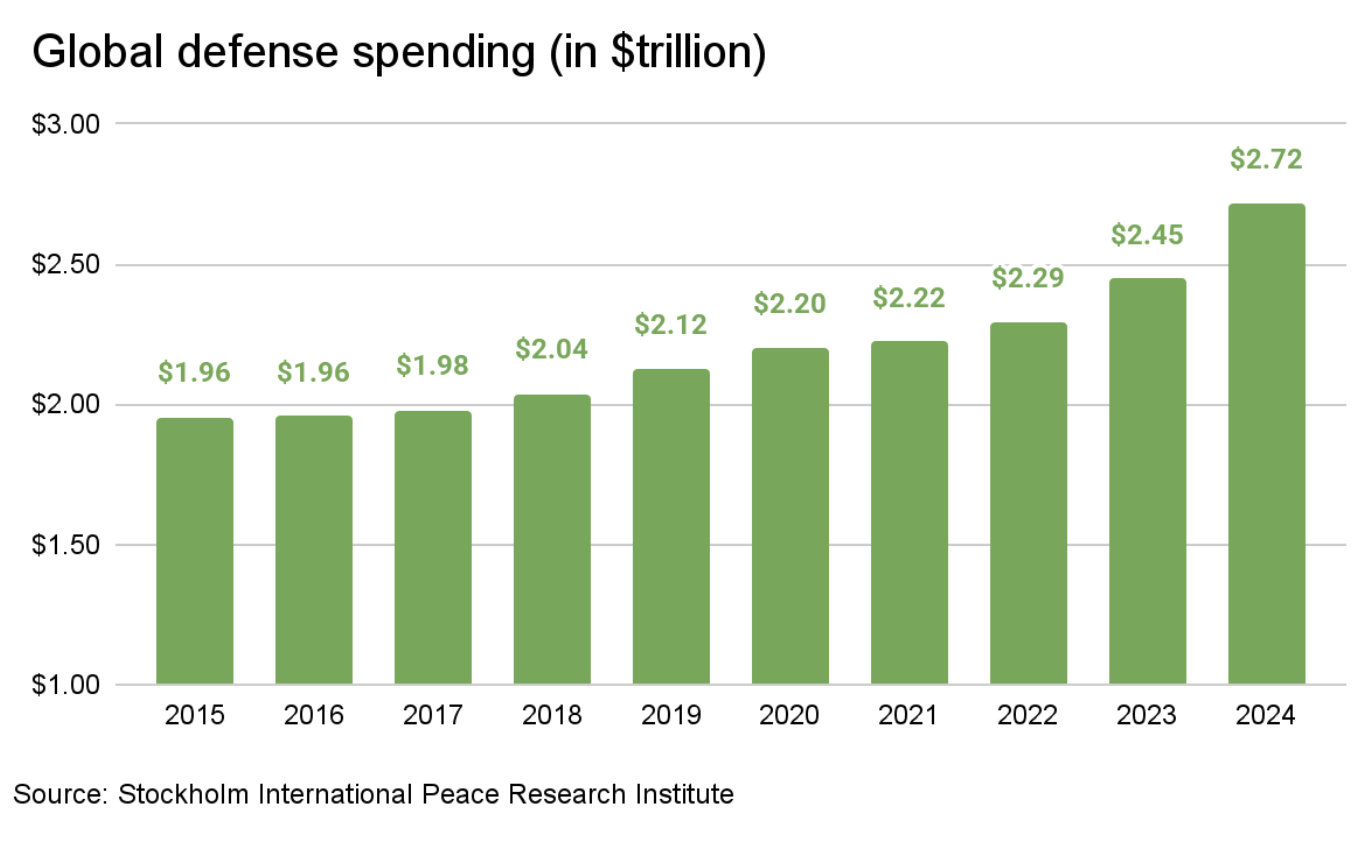

But that is starting to shift back in focus as defense spending across the world picks up. According to the Stockholm International Peace Research Institute, global defense spending hit a record $2.72 trillion in 2024. And the trajectory continues to point upward.

The preliminary fiscal 2026 US budget proposes raising the base defense spending to more than $1 trillion, a 13% increase from the 2025 budget of around $900 billion. Meanwhile, NATO members are reportedly coalescing around a much more ambitious target of 5% of GDP, up from the current ~2% guideline.

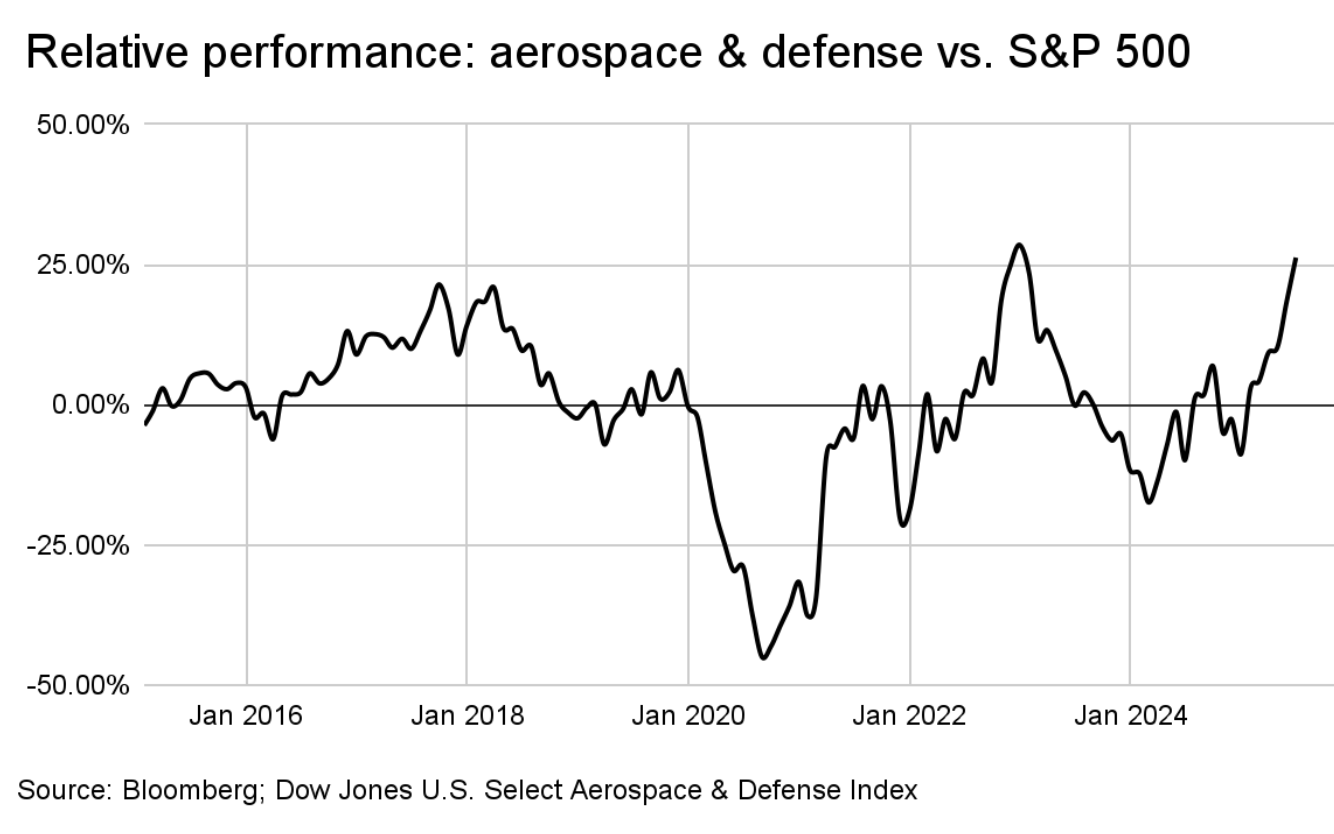

All of this pushes defense and aerospace stocks higher. The sub-sector is up over 24% year-to-date, which reflects growing investor confidence that government funding will continue to flow.

Is this an opportunity?

With valuations stretched, like the entire market, we believe it’s about being selective.

The median forward P/E in the defense space is trading at a 25% premium to its 10-year average, while forward earnings growth expectations sit at just 4.5%. That’s not particularly compelling—but this doesn’t factor in the possibility of another wave of global defense investment that we mentioned earlier.

Some of the most compelling opportunities lie in firms with strong international order backlogs and leadership in high-demand areas.fFrom our reading, this seems to be producers of missile systems, hypersonics, fighter jets, and joint all-domain operations (i.e. tools that connect and coordinate capabilities across air, land, sea, space, and cyber). These segments could benefit if the defense budget grows, particularly with 17% of the currently proposed $150 billion defense reconciliation bill earmarked for integrated air and missile defense.

Keep in mind, this is also a sentiment-driven space. Earlier this year, a single comment from President Trump threatening to renegotiate certain contracts was enough to send shares of defense contractors lower. Even if the broader budgets stay intact, headline risks remain.

What to watch going forward

The ongoing US budget negotiations and the upcoming NATO summit later this month could be key catalysts for the defense sector. The details are still unfolding, but the direction is clear: companies with diversified global exposure and strong alignment to high-priority areas such as air and missile defense and joint all-domain operations, are likely to benefit most. Investors should stay focused on geopolitical tensions and changes in defense budgets.

Meanwhile, I’ll retire my NY Knicks defense chants —until next year.