Were earnings that resilient?

Were earnings that resilient?

“He loves us so much.” is all I could think as I walked away from dropping our dog off with a sitter for the weekend. He watched me and whined, waiting for me to come back. That’s the thing about dogs. You feel their love consistently.

Markets can be less consistent with their love—earnings growth expectations as well.

Reading commentary from others on the state of the markets, much of it warns of the known risks; tariffs, potential inflation, a potentially weakening job market and so on. But all of them—every last one I’ve read—tout earnings results and the resiliency they have shown. In several places, stats such as % surprising on the upside relative to expectations, are compared to historical rates. For example, a piece from JPMorgan on Monday stated: “S&P 500 companies so far have surprised on earnings by 7.9%, vs. 4.8% avg last 4Qs.”

But should their resiliency have been a surprise?

Well, two things are true: 1) Liberation day on April 2, with the announcement of tariffs, took growth expectations down, inflation expectations up, and markets down.

2) 7 days later they were mostly paused through July 9, which then was pushed to August 1. This means none of the tariffs were really around while companies operated from March 31 to June 30.

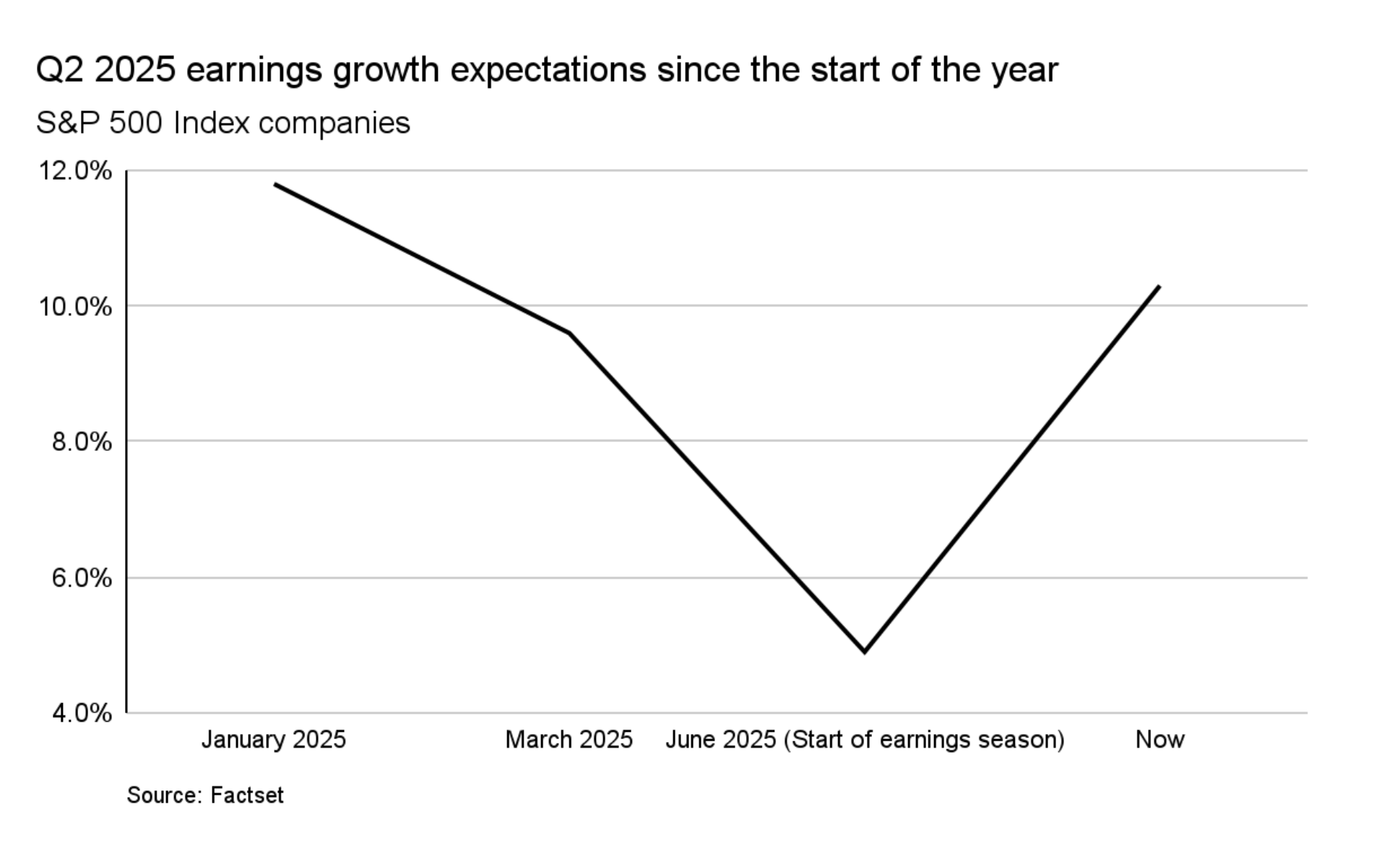

Below, you can see how earnings growth for the S&P 500 companies is landing close to where they were originally estimated on March 30th, before Liberation Day—around the 10% mark now and up from 5% at the start of earnings season. The low expectations made for easy beats.

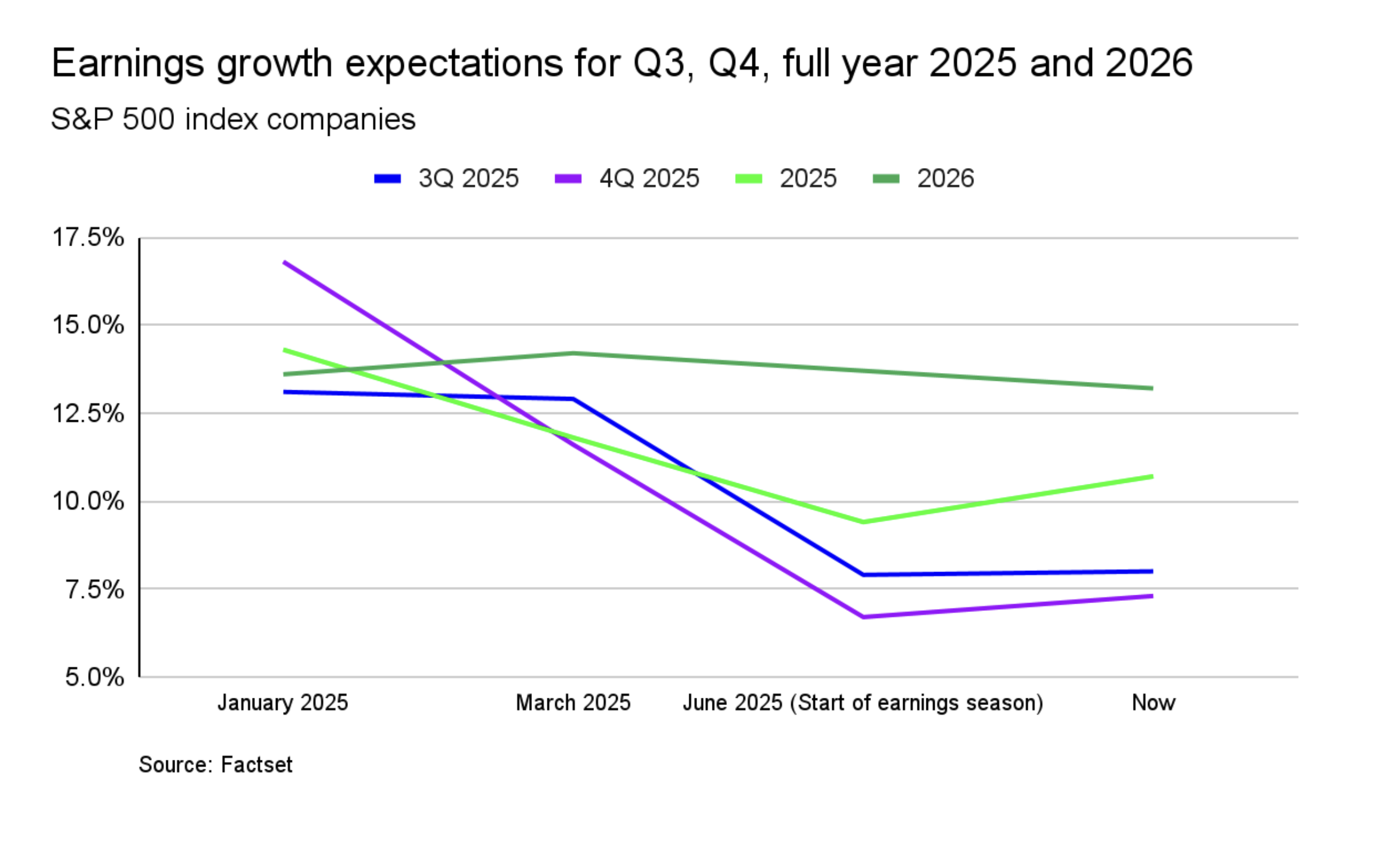

Given that tariffs, albeit overall at lower rates than on April 2, are in effect for Q3 and there are signs of a moderating labor market, I believe it’s fair to expect some type of near-term pullback. Especially because earnings growth expectations for Q3 and beyond have stayed robust at 7% or more:

Beyond earnings, the other wildcard is the Fed:

The Fed has been on a pause, watching to see whether inflation ticks back up due to tariffs. Since July’s payroll numbers came in weaker than expected last Friday, and prior months were revised lower—a rate cut in September became possible again.

And if job growth continues to soften, the Fed could opt for an “insurance” cut of 25 to 50 basis points. Interestingly, as of August 5, the Q3 GDP estimate is solid at 2.5% annualized. Historically, when the Fed has made insurance cuts, in 1995, 1998, or 2019, markets have rallied strongly over the following year. An environment of moderate growth and easier policy has typically favored mid-caps and cyclical stocks.

But, so far, the pull of inflation has been stronger than the pull from the labor market. We get CPI data next week. It will be important.

Perhaps as important as having a dog that loves you.