Earnings look fine—but pay attention to cash

Earnings look fine—but pay attention to cash

For what it's worth, the Q1 earnings season delivered some pretty good results. Both revenue and earnings largely came in above expectations, with companies reporting earnings about 6% above estimates. The biggest sector drivers of earnings growth are Healthcare and Communication Services.

On the flip side, sectors like Energy, Materials, Consumer Discretionary, Staples, and Real Estate have posted negative EPS growth—a clear reminder that not all parts of the market are firing equally.

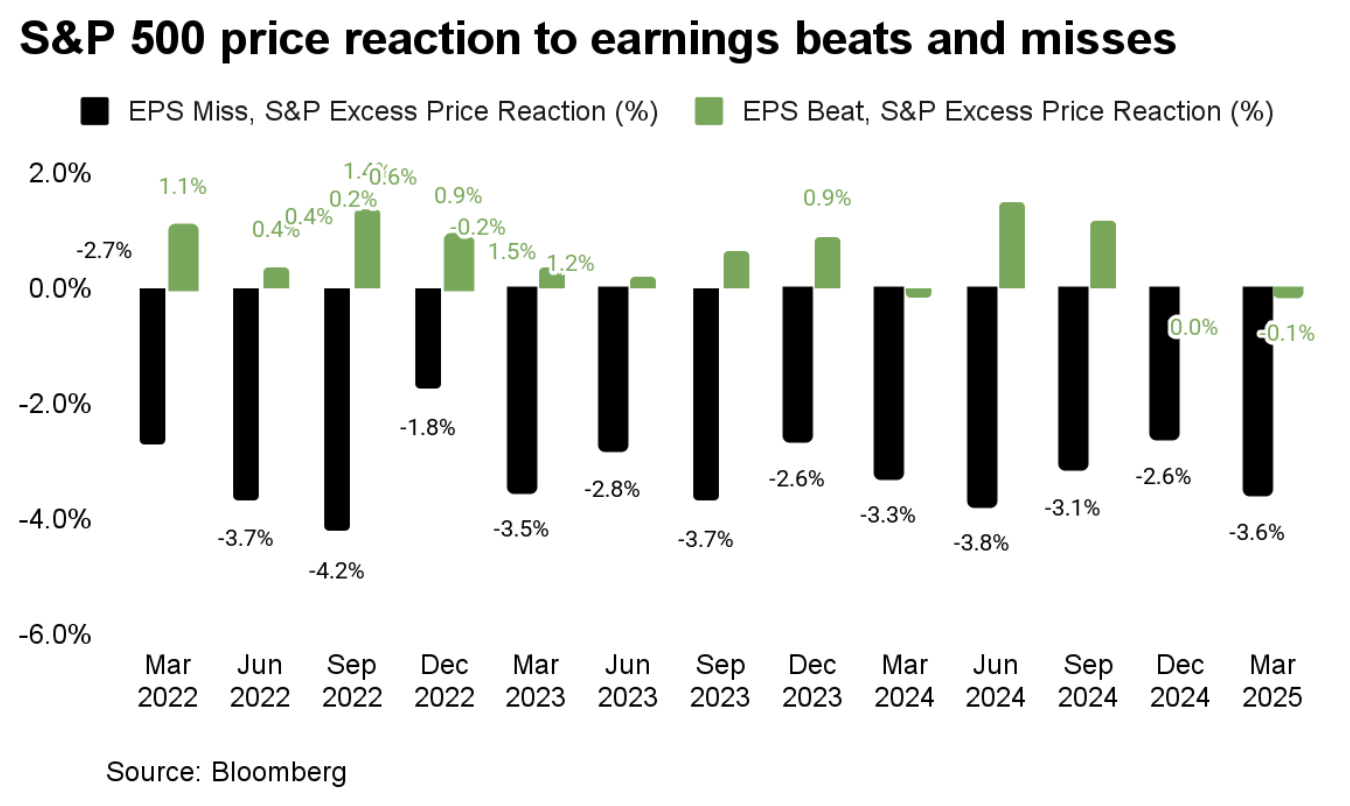

Interestingly, companies that beat earnings saw a decline of -0.1% in their stock prices, while those that missed saw their stocks drop an average of -3.6%. This shows a bias towards reacting negatively right now—no matter the results.

Why such a negative skew?

For one, the bar was set low going into this season, so a miss may suggest something more serious under the surface.

Second, there’s still macro uncertainty (and thus risk) ahead—from tariffs to geopolitics—therefore investors likely aren’t eager to reward short-term beats without stronger forward guidance.

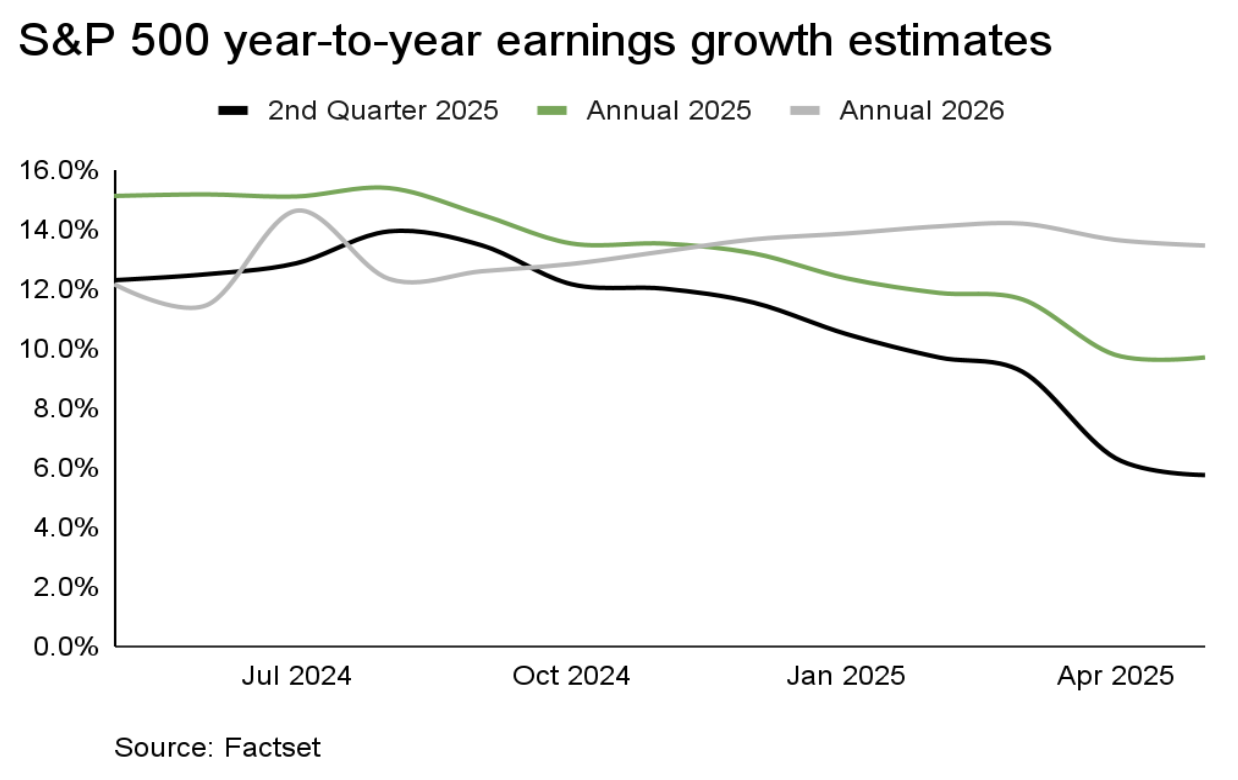

And overall, guidance has been on the weaker side. Many companies have trimmed their outlooks or skipped guidance entirely because of the unknowns related to tariffs. As a result, Q2 earnings growth estimates have fallen by over 50% from their peak in August 2024, and full-year 2025 forecasts are now tracking toward 10% growth—down from nearly 12.5% at the start of the year.

Look to free cash flow

In a market short on clarity, one thing still holds true: cash is king. Specifically, free cash flow (FCF)—the cash left over after a company pays for capital expenditures. It’s what powers dividends, fuels buybacks, and helps strengthen balance sheets. And while the many complexities surrounding tariffs continue to play out, free cash flow can be a useful guidepost. For investors, it makes sense to stay positioned in companies that generate steady cash while we wait for more visibility.

At the index level, free cash flows appear stable—and even growing (see chart below). Looking at FCF margins, or the percentage of revenue converted into free cash flow, we’re seeing expansion in sectors like Consumer Discretionary and Technology, where these margins now sit comfortably above their three-year averages.

The next question might be: Are companies actually redistributing this cash back to shareholders? For the most part, yes—but they’re being more cautious, likely to preserve flexibility in case tariff or policy risks escalate.

Potential free cash flow destinations: dividends and buybacks

Dividend growth, which tends to peak in Q1, slowed but remained in line with the range of expectations. In Q1 2025, US common dividend increases totaled $19.5 billion, up 37% from Q4 but down 14.1% from Q1 2024. Meanwhile, dividend cuts rose to $4.2 billion, a 68% jump from the prior quarter, though still below last year’s levels.

Despite the caution, the outlook is solid. The S&P 500 is on pace for a record year of dividend payments, with a 6–7% increase expected in 2025.

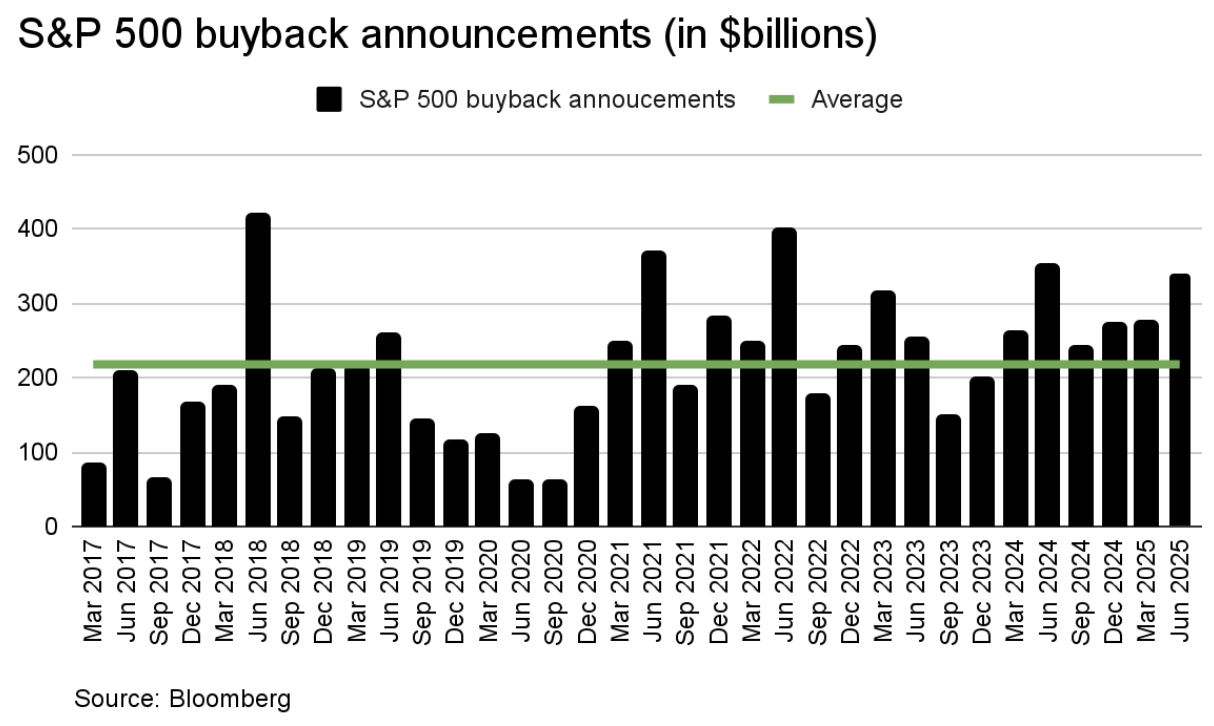

Another way companies increase shareholder value is through buybacks—where they go into the market and purchase shares of their own stock. And buyback activity is picking up, with Q2 announcements already 23% above Q1 levels. That suggests companies are taking advantage of lower valuations to repurchase stock at a discount.

In a market where earnings beats aren’t moving the needle and forward guidance is anything but clear, free cash flow is emerging as the metric that matters. It's not just about who’s profitable—it’s about who’s flexible. Companies with strong FCF can navigate uncertainty, quietly returning capital to investors, while preserving options.