Anatomy of sentiment

Anatomy of sentiment

Our thoughts and perceptions can shape our reality. The same holds true in markets. Since markets are a collection of human thoughts and the movement of money, how we perceive the world dictates how we spend and invest and thus the markets—even when reality doesn’t quite align with perception. In investing, we call this sentiment. It’s the collective mood of consumers and businesses, influencing financial decisions on a massive scale.

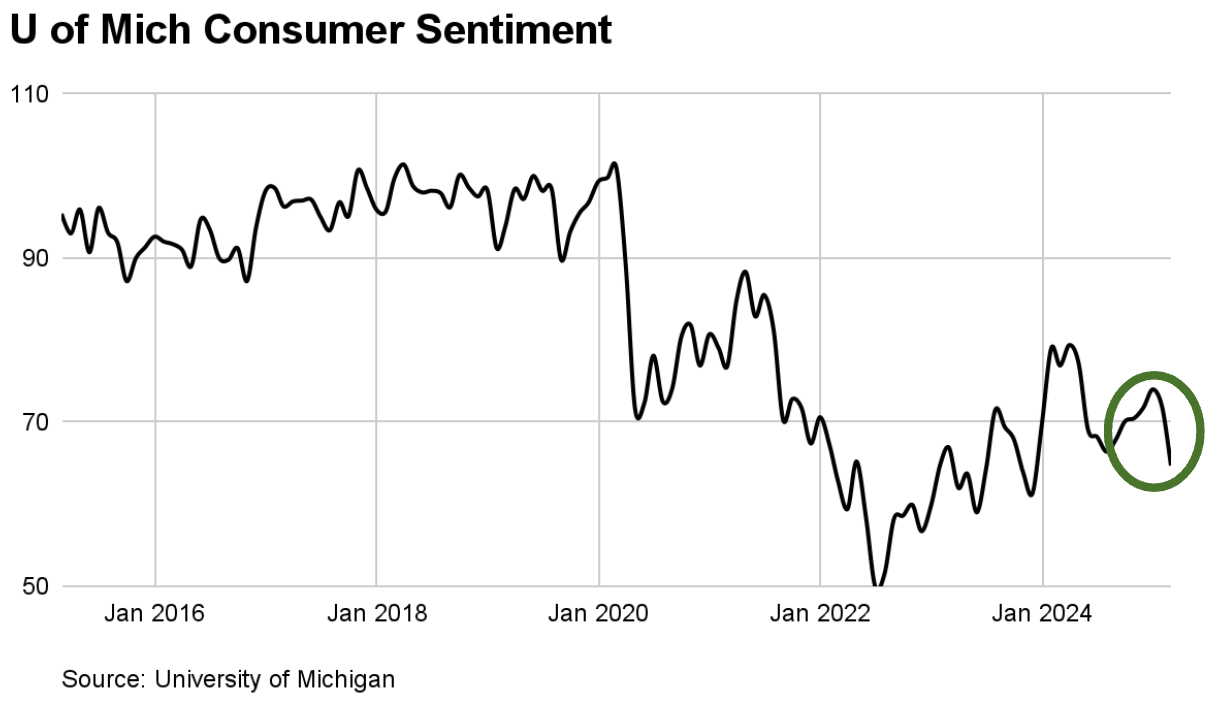

One of the key data points used to measure consumer sentiment is the University of Michigan Consumer Sentiment Index, which captures how people feel about their personal finances and income outlook—but doesn’t necessarily reflect the actual state of the economy.

Consumer sentiment recently took a hit (chart below) despite a so-far-stable labor market. Concerns over job security and rising prices—fueled by recent government layoffs and uncertainty from tariffs—are making people more cautious. Many surveyed have declared they will make fewer big purchases, from cars and electronics to travel.

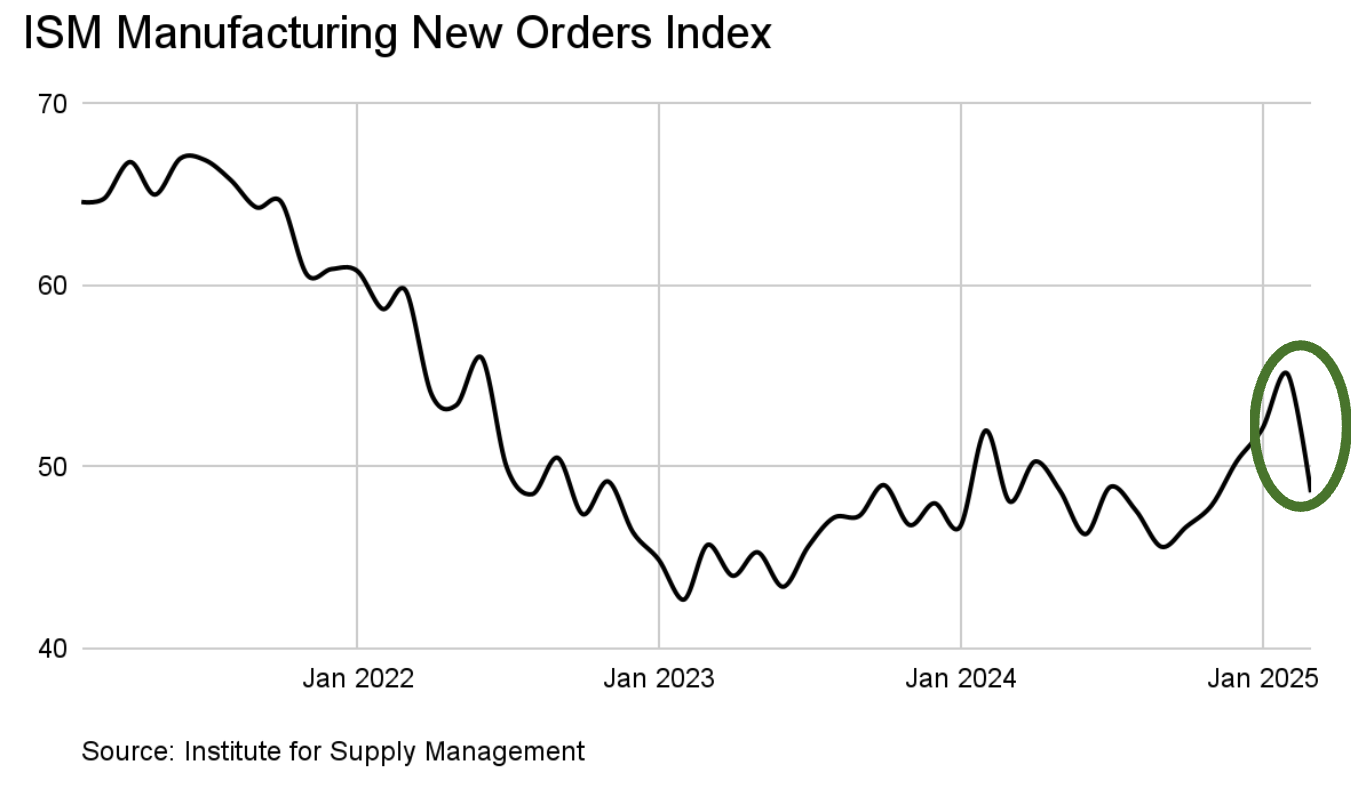

And even though manufacturing is a smaller part of the economy (10%), it still matters—especially as an indicator of future business activity. The ISM Manufacturing New Orders Index, which tracks demand for future production, ticked above 50 in January, signaling expansion. But the reason behind it wasn’t a surge in real demand—it was a rush to place orders ahead of potential tariffs.

Since then, the uncertainty over tariffs has led businesses to pause new orders, sending manufacturing sentiment right back into contraction territory.

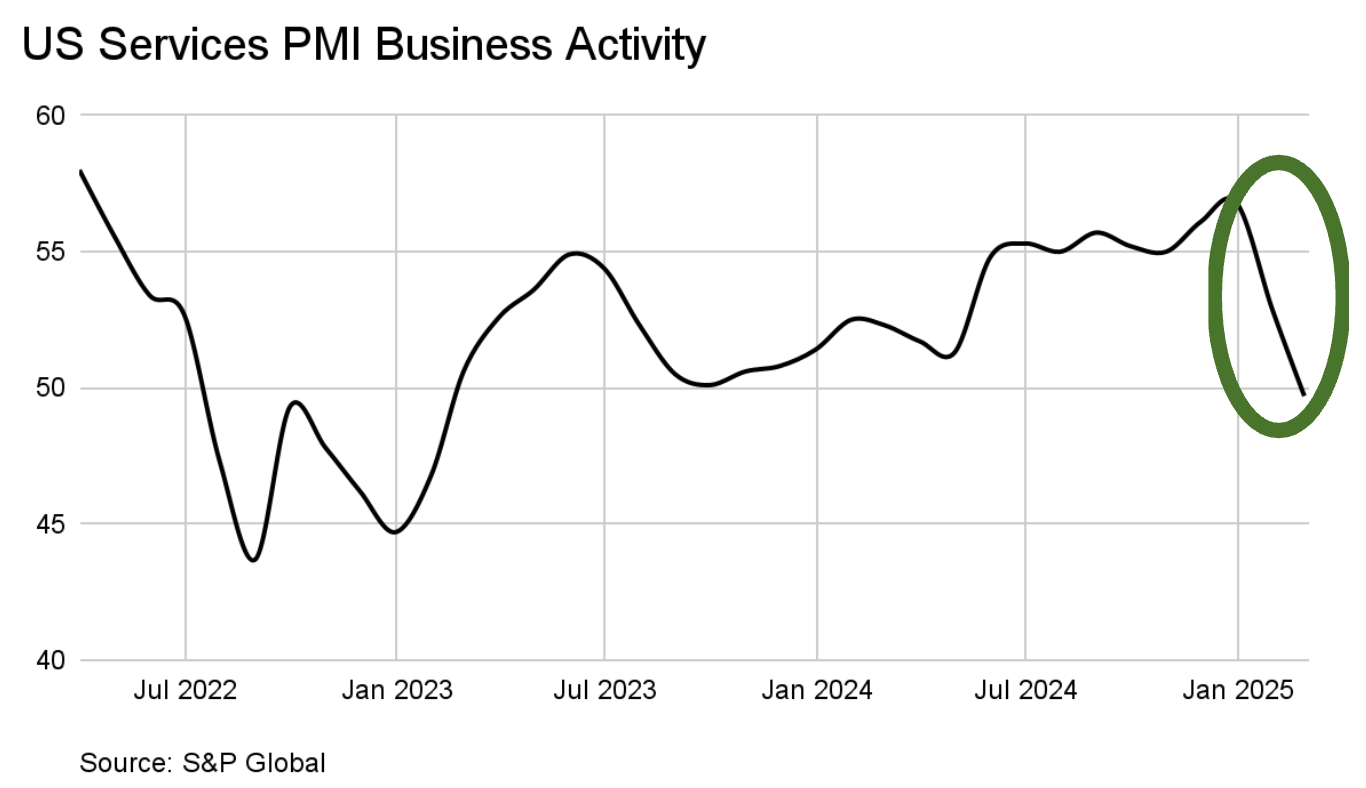

And we’ve seen some of the same in business activity for services—surprising to the downside in February. This is important because services are a much bigger part of our economy (77% of GDP).

Today we got some better services data; ISM Services PMI came in above expectations. So things are not all bad. But these shifts have pushed this quarter's estimates for GDP growth down (actually to negative territory)—and the market has followed.

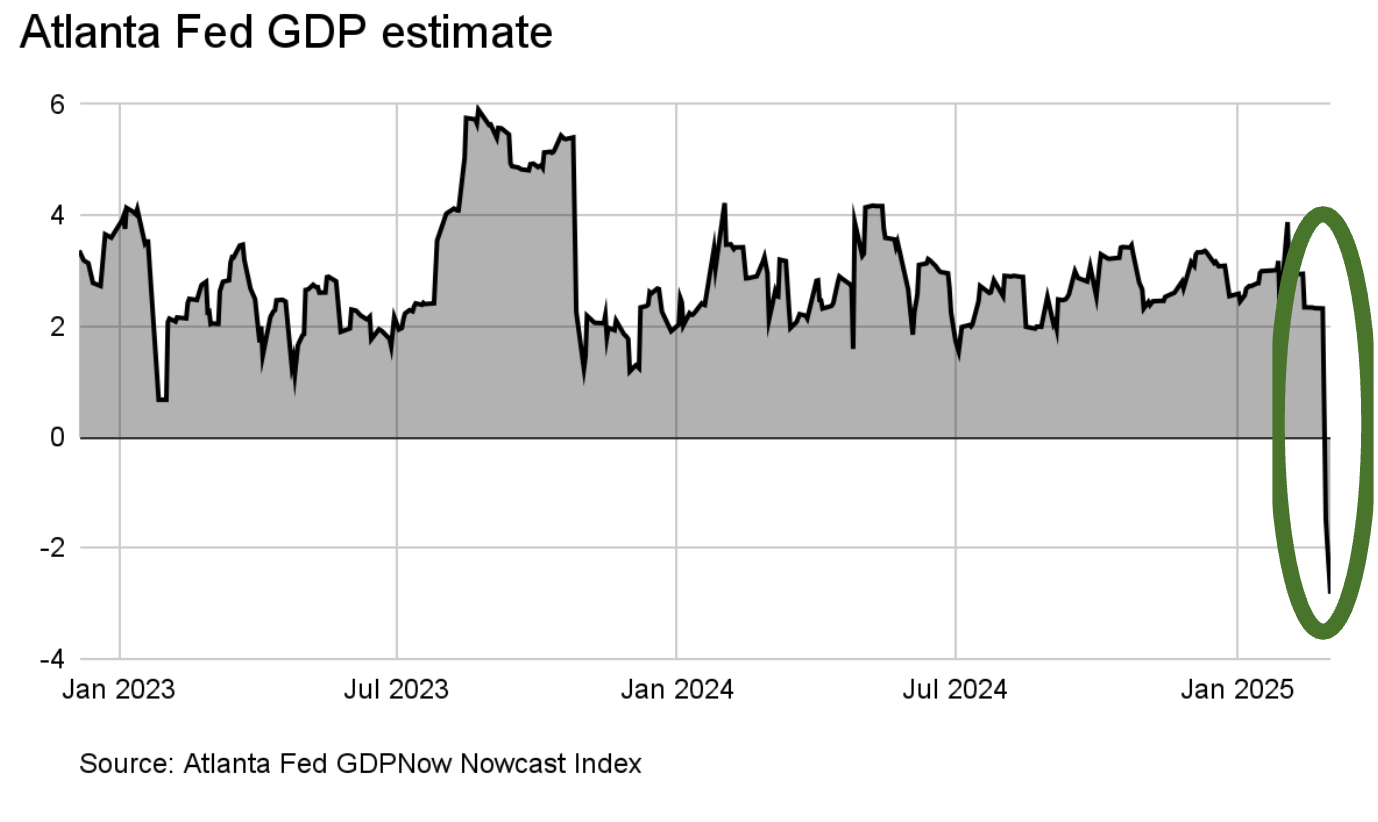

The Atlanta Fed’s GDPNow tracker is flashing a warning sign: 1Q25 GDP is now projected to contract by -2.8%.

This sharp drop is largely being driven by real personal consumption expenditures growth falling from 1.3% to 0.0% and real private fixed investment growth sliding from 3.5% to 0.1%.

Why it matters GDP and corporate earnings generally move together, so this drop raises red flags for markets. Over the last 35 years, every 1% increase (decrease) in YoY GDP growth has translated into a roughly 5% increase (decrease) in S&P 500 earnings per share (EPS).

Since it’s likely GDP is lower for Q1, earnings will be as well. Consensus earnings estimates have already come down for Q1. The longer the uncertainty continues, the more likely GDP will slow in Q2 and beyond. So we’ve made some tweaks to the 2025 outlook set in December:

We are lowering our GDP estimate to 2.5%, from 3%.

So, earnings growth for the year could fall from its current consensus of 11.8% to 11%.

As mentioned, the negative sentiment we’ve seen has been tied to tariff uncertainty, which may continue to weigh on markets. The direction from here largely depends on how long the increased tariffs and uncertainty persist, as well as how high/deep they go. If we see a resolution in the next few weeks, it could spark a rebound in sentiment and a reversal of some S&P 500 losses, keeping us on track for our current target of 6,500. However, if uncertainty drags on, market pressure could intensify, further pressuring GDP and S&P earnings growth closer to 8.5%. Assuming a generous 21-22x P/E multiple, prolonged uncertainty could push our S&P 500 target closer to 6,300.

Markets are at a crossroads, and the next few weeks could determine whether this is just a temporary mood or the start of something deeper.