The dichotomy

The dichotomy

To me it feels like there is a growing dichotomy in life. One minute you’re reading about conflicts abroad, the details of the recent Big Beautiful Bill impacting the economy, and the regulations on crypto in the Genius Act. And the next you’re deciding what to eat for dinner and which road to take while out on an errand. These things, both the globally significant and the locally mundane, living together in your brain is just downright wild.

And yet, it’s a metaphor for the history of the US economy and investments—and the “Two Americas” we have today.

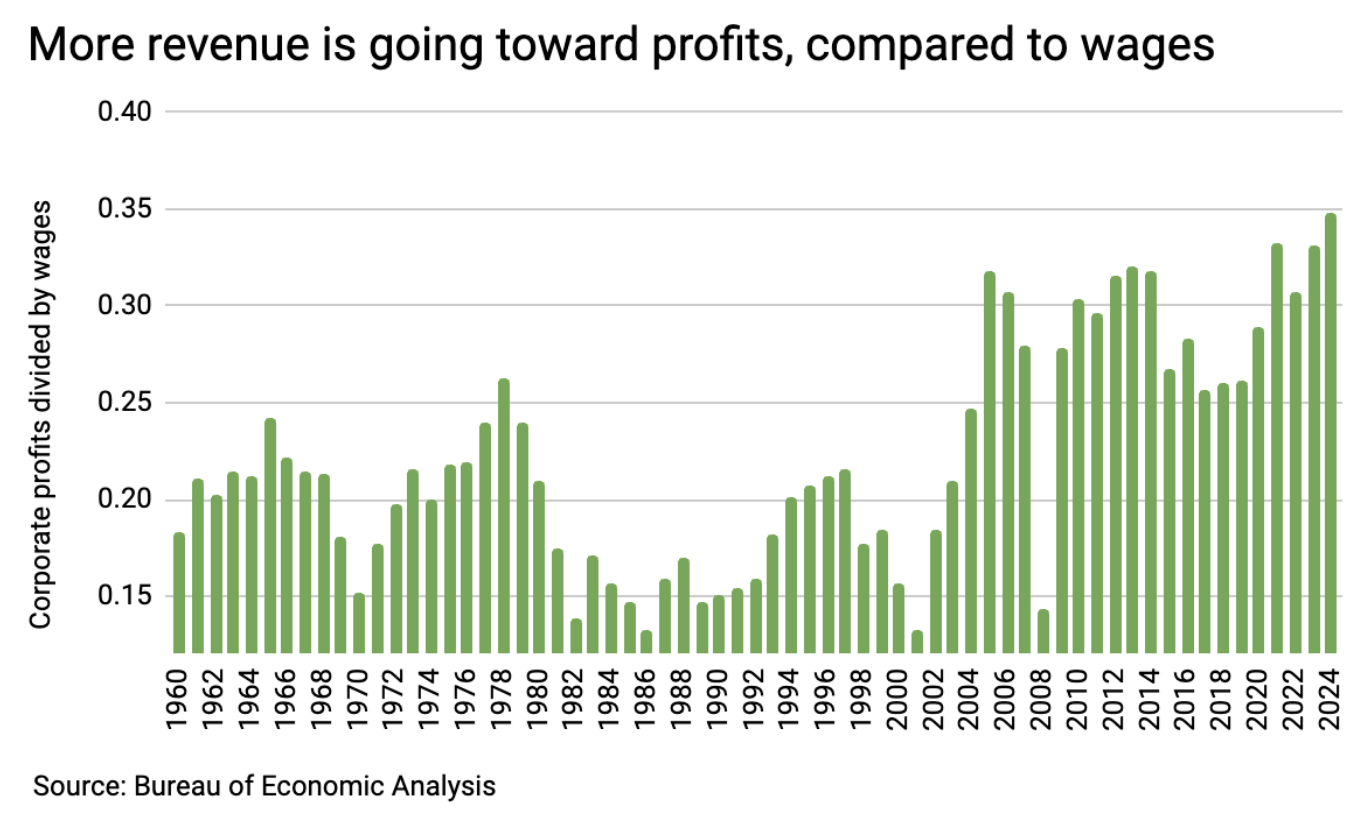

As I wrote about several times (most recently in April) post World War II, the large middle class was the backbone of the US economy. But that foundation eroded over time, particularly since the early 2000s as corporate priorities shifted focus almost exclusively towards corporate profits and boosting shareholder returns.

Today, the top 10% of earners—those making $250,000 or more—account for nearly half of all US consumer spending. These households tend to hold financial assets and benefit from market gains.

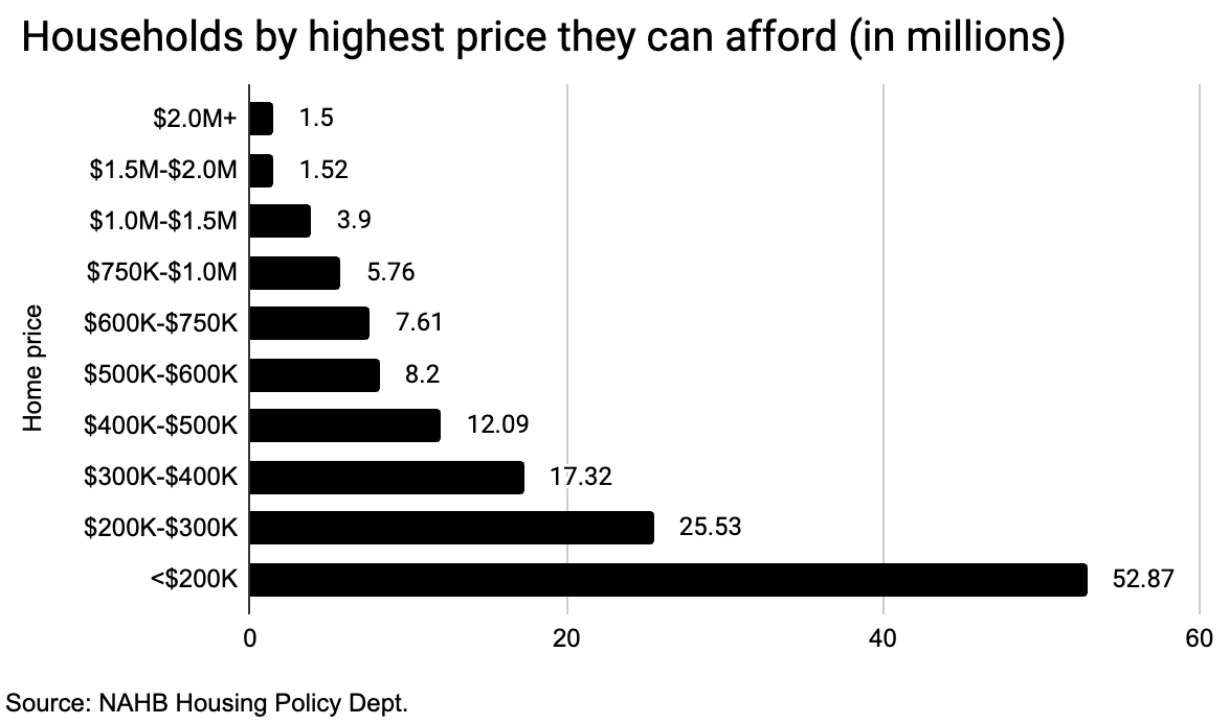

Middle- and lower-income households rely heavily on wages. With the trend in the chart above, that means they were hit hardest by rising costs and shrinking affordability, especially in housing. In fact, over 57% of US households can’t afford a $300,000 home, even though the median home price in 2025 is $459,000, according to the National Association of Homebuilders.

At the same time, the traditional safety nets have been steadily dismantled. 40 years ago, about 60% of private-sector workers had access to a defined-benefit pension. Today, that number is closer to 14–15%. In their place, was a shift to 401(k)-style plans, pushing the responsibility of retirement savings squarely onto workers’ shoulders.

The double-edged sword of AI

Looking ahead, artificial intelligence has potential to either further divide the haves and the have-nots, or start to bring them together.

On one hand, AI may boost productivity and profits for the companies that use it well, across all industries. It could also spawn new industries and careers we can’t think of today.

On the other hand, it could displace jobs faster than workers can retrain, straining household budgets and creating social and political tension. If AI adoption continues without clear policies to support affected workers, we could see slower consumer spending, greater political backlash, and a growing risk of regulation.

Navigating an unequal economy The narrowing of the middle class and rise in inequality isn’t just a sociopolitical issue – it also shapes the investment landscape, creating both opportunities and pitfalls. Here are some key considerations:

Own a slice of the system: As I shared in a World Economic Forum piece a few years ago, wages alone haven’t been enough. Stocks, property, and businesses are where wealth has been built. Regular investing, even in small amounts, lets you tap into corporate growth and align yourself with the economic engine that’s historically been rewarding owners vs. workers.

Follow the money: As inequality deepens, consumer spending is splitting. Luxury brands and deep-discount retailers thrive. These shifts may create opportunities in places adapting quickly to consumer polarization between high-end spenders and budget-conscious shoppers.

Invest in AI: Automation is driving profits, but also raising the risk of political and regulatory blowback. Stick with companies using AI effectively, to grow revenues or reduce costs, but be mindful of social consequences.

The fate of the middle class and the future of the market are linked. A strong middle class supports steady demand and innovation. But if that base continues to erode, even the most profitable companies will feel it eventually.

That’s why investors must stay informed. Not just of financial trends, but of the social and political shifts taking shape around them. Smart investing today means also understanding the structure of the economy itself and how it continues to change.