Optimism is high (again) and that’s a risk

Optimism is high (again) and that’s a risk

The S&P 500 is once again nearing record highs (and our target of 6200). While macro headlines have been a bit quieter the last few days, the recent rally raises some important questions around valuations, earnings expectations, and the direction of Federal Reserve policy.

On the surface, valuations appear more reasonable than they were back in February when the market last peaked. BUT the recent dip in forward price-to-earnings ratios is being driven by rising earnings estimates vs. falling stock prices. In other words, equities are looking cheaper because analysts are now projecting stronger profits across sectors than a few months ago, which pulls down valuation multiples—on paper. To be fair, this form of “valuation compression” is usually a good sign.

But economic signals are less rosy

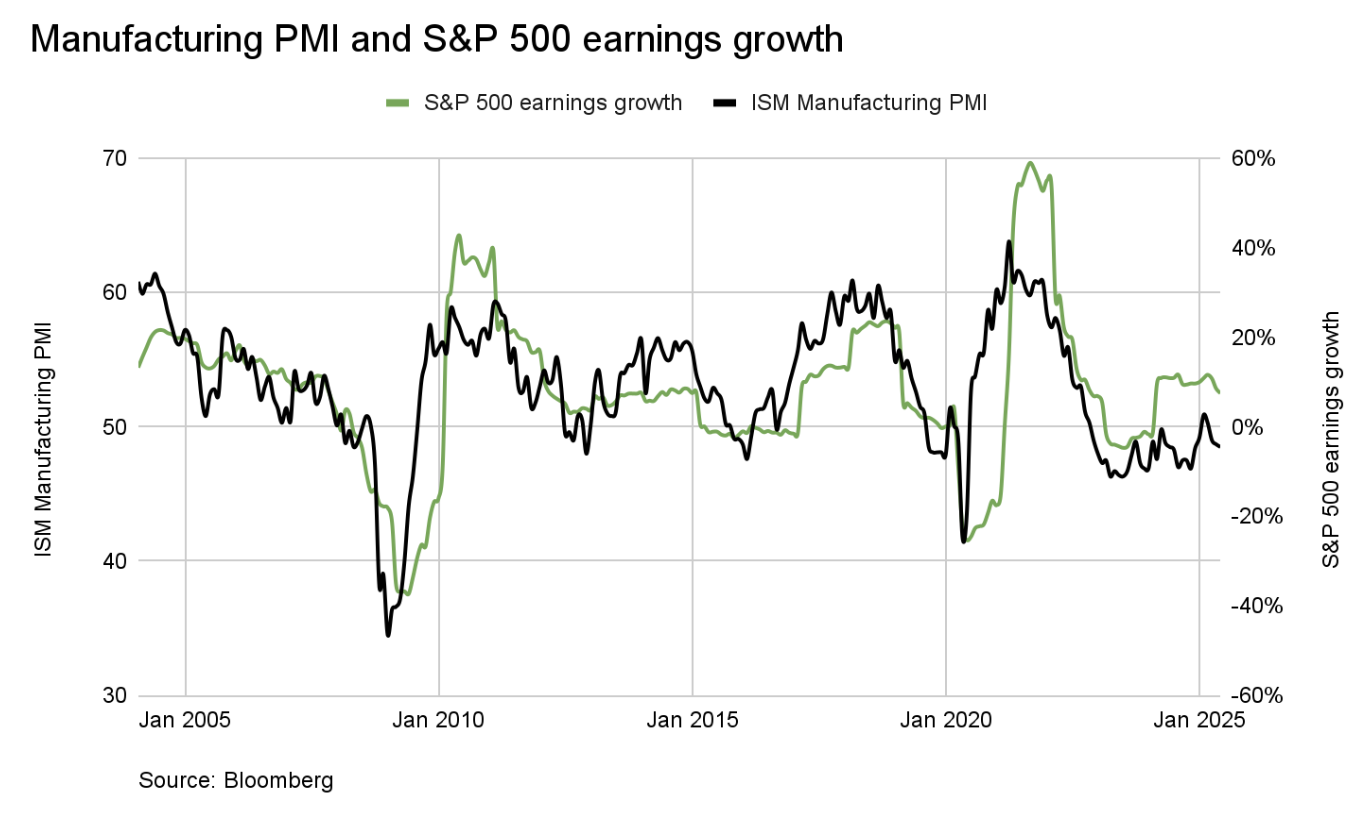

Take the Institute for Supply Management (ISM) Manufacturing Purchasing Manager Index (PMI), which tends to lead corporate earnings by about four months, has continued to weaken and remains in contraction territory, suggesting potential softness ahead.

If earnings fall short of these increasingly aggressive forecasts, markets could be in for a negative surprise.

This time could be different. PMI could rise to meet earnings growth expectations. And this is possible because the uncertainty from tariffs is a temporary drag on production. But it’s something we are watching closely. It’s also important to keep the broader valuation picture in mind. Even with the recent improvement, the S&P 500 is still trading roughly 33% above its 20-year average of 16.5x. That means stocks remain expensive by longer-term historical standards.

Part of what’s keeping valuations elevated is growing optimism around rate cuts. Traders are still pricing in two rate cuts this year but have crept the timing of them to be sooner — July instead of September. Federal Reserve Chair Powell repeated himself this week, after last week’s Fed meeting, that the committee is not in a rush to ease and the economy is in a place that makes that possible. We think it’s possible that we only get one cut this year. The Fed’s next move will hinge on two factors:

inflation data in light of tariff policy and

the labor market in light of automation and immigration

Looking ahead, the next key date to watch is July 8, when President Trump's 90-day pause on reciprocal tariffs expires. Markets are hoping for/expect a clear resolution and lower tariff rates. But with earnings optimism high and valuations elevated by historical standards, any breakdown in negotiations could put equity prices under pressure.