Mid-Year Outlook: many lives already lived

Mid-Year Outlook: many lives already lived

Investors have already lived several lives this year. As I reviewed my original outlook for 2025 (It’s always and never different), and my update to return expectations in March, it had one flaw: an underestimation of the level of impact the Federal government would have on the markets this year.

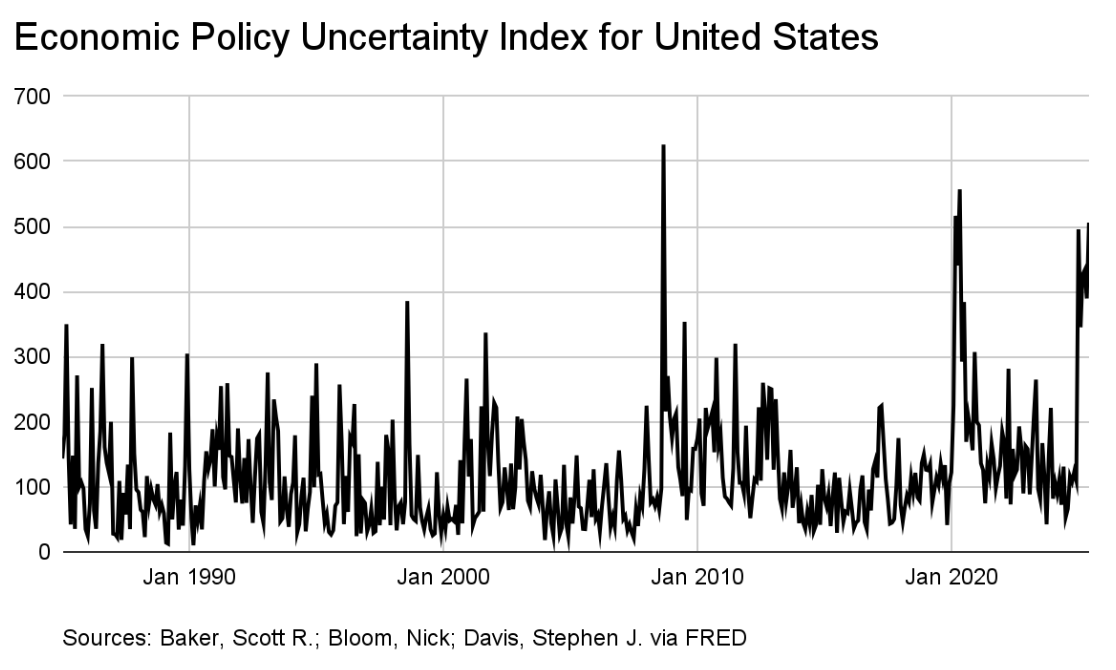

Despite acceptance of this, or as a result of this (?), economic uncertainty continues.

Essentially, we believe if we are still in uncertainty by September, the market could see a pullback and the economy could be more at risk than we previously thought. So this midpoint outlook comes with more risks. But there are still pockets of opportunities.

Starting with the economy:

Tariffs. Just last week, President Trump announced another round, pushing the effective tariff rate to 20.8%, according to Yale’s Budget Lab—much higher than the market-discounted average of ~12-14%.

While tariffs could generate around $3 trillion over the next decade ($100b+ have been collected and Treasury Secretary Bessent cited $300b per year), this is still shy of the $3.5 trillion expected cost of the Big Beautiful Bill over the same period.

Potential inflation. Historically, producer prices take one to two quarters to show up in consumer prices and another few quarters to hit margins. Based on our estimates, core CPI could begin to hit around 3% by year-end (from 2.7% today). So tariffs start to become essential in net spending cuts.

The truth is, lower-income households where necessities are a larger share of spending, will feel rising costs more acutely. Meanwhile, higher earners, who account for nearly half of all US spending, can still absorb those costs. For this reason, we don’t expect inflation to significantly dampen consumption in the second half of this year.

Which brings us to interest rates. Tariffs, and tighter immigration, are feeding cost pressures. This makes it hard for the Fed to cut aggressively and even if they do, long-term rates may not follow—given the deficit is still expected to expand. With this in mind:

One cut, and done: We see a single cut this year, with a continued slower pace of quantitative tightening keeping financial conditions stable.

10-year rates should stay rangebound, hovering around 4.5%.

The labor market. Tariffs may have a small impact on inflation this year. But, my bigger concern, that stretches into 2026, is that tariffs lead to labor force reductions. Instead of more material passthroughs (there were some higher prices in goods inflation in June’s CPI report), other costs are cut. Since labor is about ⅔ of a company's cost (at least for now), this is often a place to go. We also can’t forget AI. As more of it is used in all industries, efficiencies will happen. Less people will be needed to do more (but I am a big believer in other industries, we can’t even conjure, eventually being formed out of this revolution).

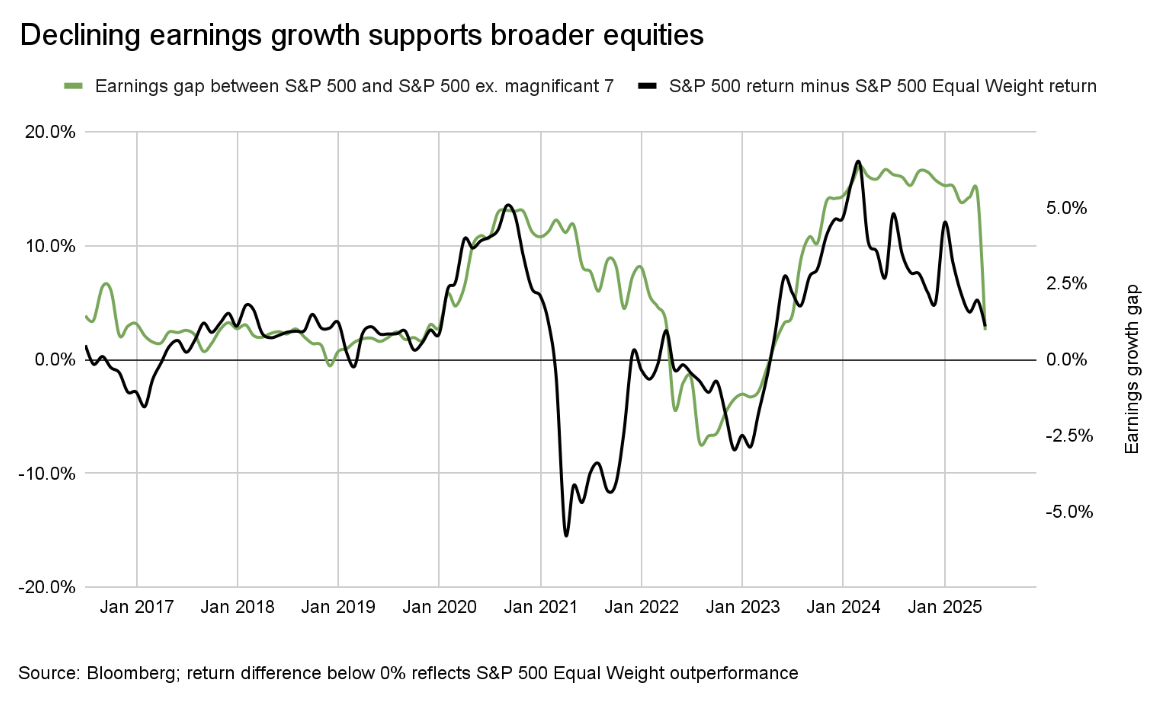

Markets. As for equities. Back in March, we lowered our year-end S&P 500 target down from 6,500 to 6,200. As of today, the index continues to flirt with record highs around 6,300. This strength has come on the back of a rising expectation of falling interest rates, and valuation expansion. Earnings expectations have come down for 2025, but growth rates have stayed in the double digits for 2026. With the full impact of tariffs still unknown and potential for weakness in the labor market, we are keeping our base case target at 6,200 with potential for upside to 6,500 (if our concerns don’t materialize or the Fed cuts more than we expect).

But in all of this, we see the Mag 7 as another set of stocks, to be judged on their own, without the help of a group name.

Within equities, we continue to favor the following:

A tactical bias to:

Cheaper growth names such as in software. This is where you can find more reasonable valuations in tech—and they may be part of the next leg of AI.

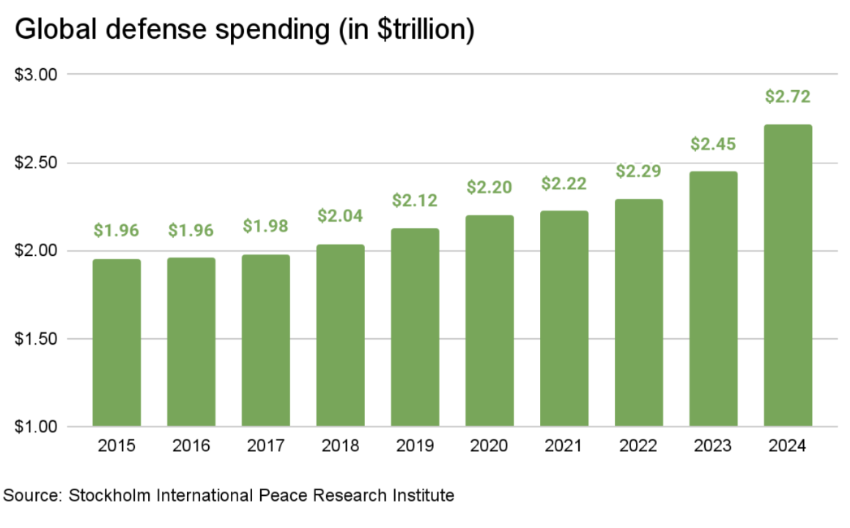

The aerospace and defense diversified names, given higher spending both home and abroad.

Regional banks: Lower valuation within the banking sector and could benefit from deregulation.

Mid caps over small caps: Small-cap firms are vulnerable to rising borrowing and labor cost due to thinner margins and tighter refinancing windows. We remain focused on the US large- and mid-cap names.

Capex growth is a tailwind: Companies investing in AI, reshoring, and infrastructure signal long-term resilience. These firms tend to be large, best positioned to benefit from productivity gains, and therefore less exposed to wage pressures.

Global convergence offers opportunity, keep some international equities. Growth expectations across Europe and Japan could catch up to the US. This shift offers a compelling case to maintain a broad international allocation. Valuations remain compelling, especially in Europe and China tech. A weaker dollar should also further support international returns for US investors.

The second half of 2025 will be shaped by divergence between countries, sectors, and households. US policy decisions, especially around tariffs and deficits, will have influence. Investors should focus on global diversification, and staying aligned with structural tailwinds set forth by policy agenda.