Better than nothing: Cap ex tells a story

Better than nothing: Cap ex tells a story

Every now and then you hear an old song that brings you to a place and time you forgot. As a kid, we drove places. To Florida for the beaches, to DC to see history, or to Maine to feel a brisk summer. And what played on the radio on those trips are now core memories, easily reignited by a tune playing at the supermarket or, as I experienced recently, a cover band: “But what a fool believes, he sees. No wise man has the power to reason away. What seems to be. Is always better than nothing. Than nothing at all”.

This song, “What a fool believes”, by The Doobie Brothers, brought me back—to the back seat of our station wagon—listening to my mom sing along (with her admittedly pretty soprano), while the breeze from the open windows softly flowed through the car.

Markets lately could learn something from these lyrics: what seems to be is always better than nothing.

I thought of this as I was diving into consensus earnings expectations (because they are everything) across market caps and then into S&P 500 companies, looking for something to believe in. Here’s what I found:

Since the start of the year, earnings expectations for 2025 have come down: Large Caps: -$10 per share or -4% to 9.6% growth

Mid caps: -$0.4 per share or -8% to 5.2% growth

Small caps: -$1.4 per share or -15% to 29.9% growth

While expectations for 2026 have moved down in an absolute sense, the earnings growth rates are the same for large caps and actually higher for mid and small caps. It doesn’t seem rational with this level of uncertainty–particularly because small caps are impacted by higher rates, which seem more certain now.

The other thing I noticed in the data is that capital expenditure (cap ex) expectations swung from negative (-2.5%) to positive (+3.3%). This piqued my interest so I dove into the details of what companies are increasing their cap ex. Cap ex tends to involve purchases of assets that could benefit the company longer term—an investment in the long term growth of their business. While growing cap ex is in line with the trend of the last few years, in this environment with potentially greater costs from tariffs and lower growth, I expected cap ex to drop. Here’s what I found:

Out of the 500 companies, 310 companies were expected to increase their cap ex, with 14 of them expected to grow it by more than 100%. 194 will have flat, none or negative growth in cap ex.

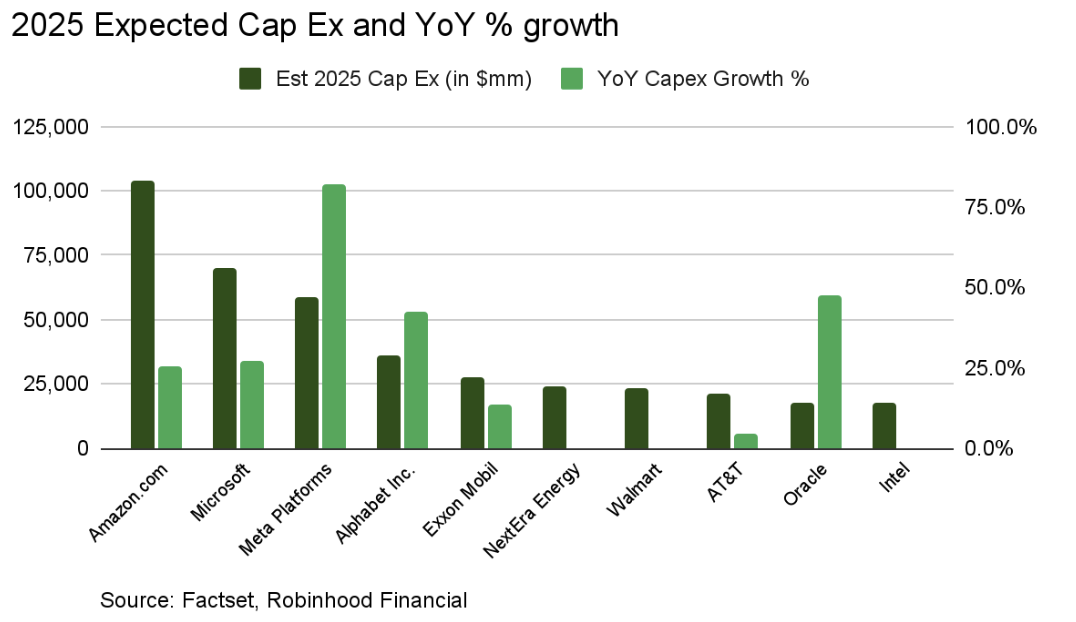

From an absolute perspective, 4 of the top 10 are Mag 7 companies—and they are spending a lot.

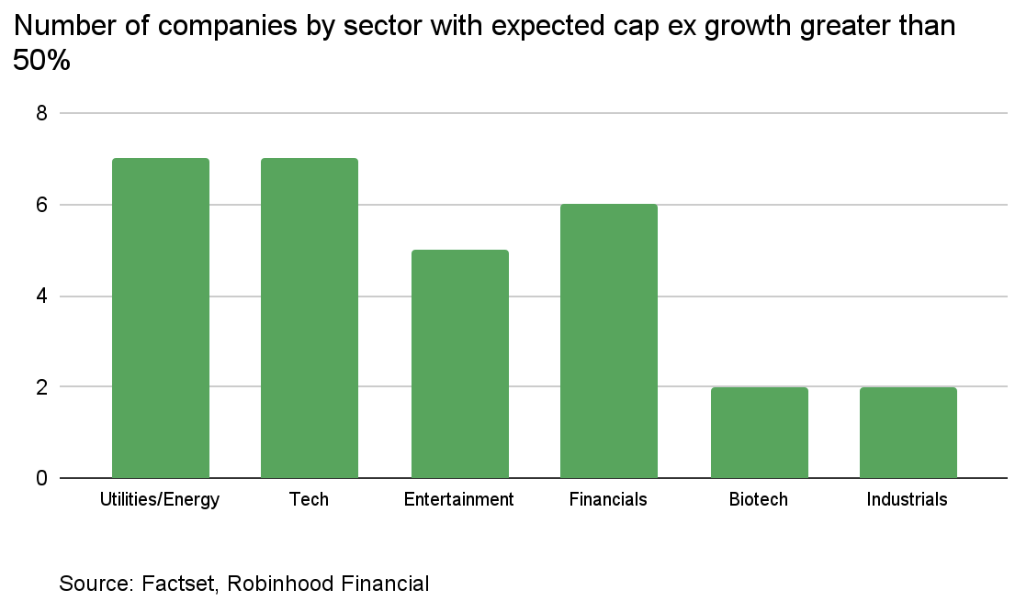

For companies with greater than 50% cap ex growth (29 of them), the secular themes of energy needs for AI and the growing demand for experiences—in cruise lines and entertainment (the boomers are retired too), came through. This tells you the expectations for growth were strong enough to really boost investments in long term projects in these areas.

Notably, there were many REITs with a large reduction in cap ex for 2025. Many of these companies said they would scale back acquisitions given lower return expectations. My conclusion from all this: despite the thundering noise from tariffs and deficits and higher rates, there is always something brewing. The data and energy needs will still be vast for technology. Earnings for these cap-ex growing utilities are expected to grow at a median rate of 10% over the next two years, reflecting stronger investment. But expectations aren’t so high that they couldn’t be exceeded. And that is something.