A couple charts before Jackson Hole

A couple charts before Jackson Hole

We have Jackson Hole this week. This annual Fed conference has, in the past, marked important speeches by the Fed Chair, setting the course for our monetary policy. DJ Powell is expected to speak on Friday morning.

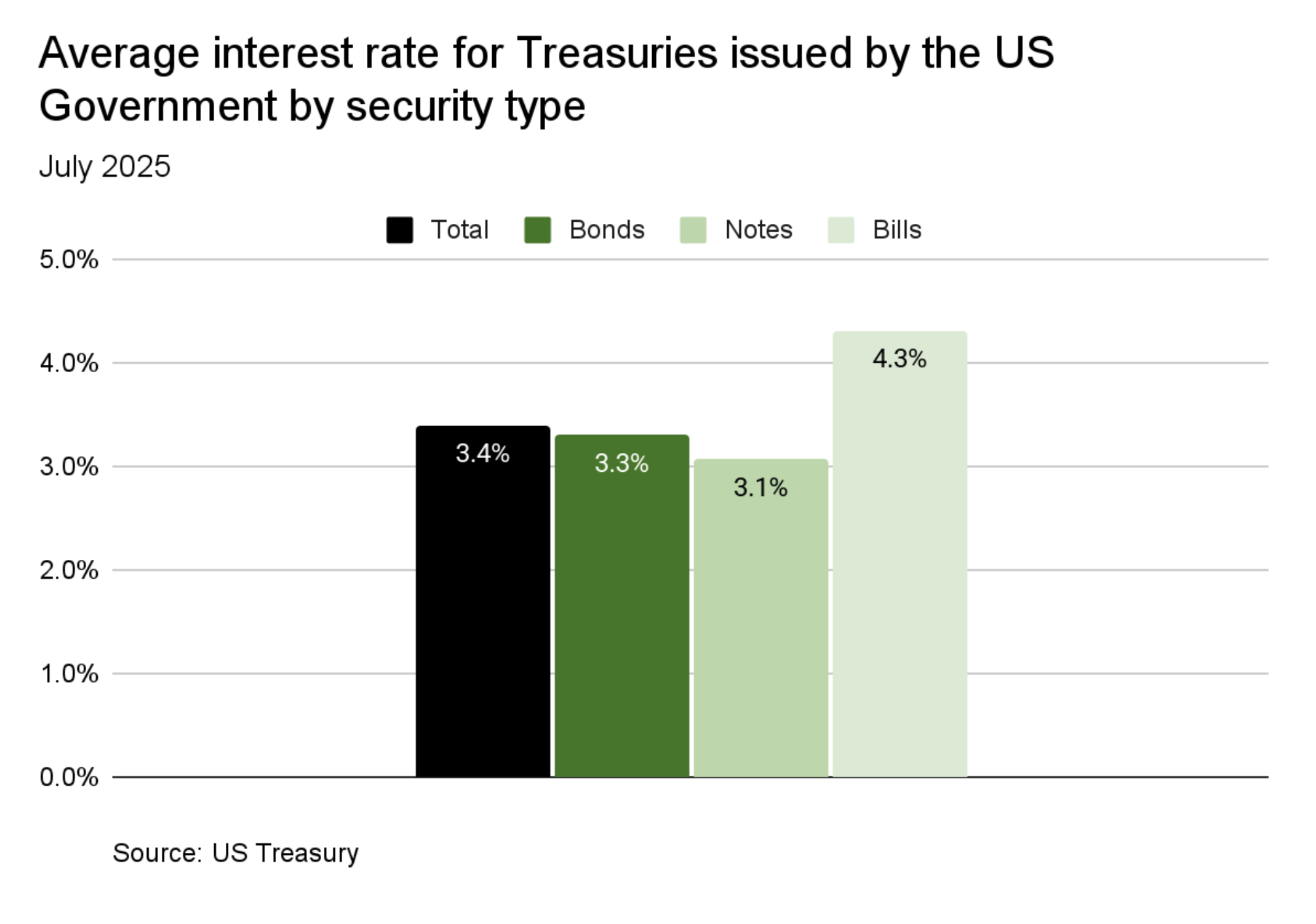

Going into it, the Fed is under pressure to cut interest rates, specifically the rate on Federal Funds. This pressure is generally stemming from the US Treasury’s goal to pay less in interest on government debt. When Fed Funds go down, short-term treasury rates also tend to follow and the US government has a good portion of their debt in short-term maturities, called Treasury Bills, that have higher interest rates than they are paying in other debt.

Note: U.S. public debt in the form of Treasury securities is primarily made up of bills (4-52 weeks), notes (2-10 years), and bonds (20-30 years).

You really can’t blame them. If I had $39.6 trillion in gross national debt, I’d look for ways to cut costs too.

By design, the Fed was meant to be independent from the US Treasury in its decision making. It is supposed to care solely about keeping inflation reasonable and the labor market healthy. I appreciate the value of that, so cutting rates to help government costs feels at odds with that.

Currently, Powell is worried about inflation in light of tariffs, more than he is worried about a weak labor market.

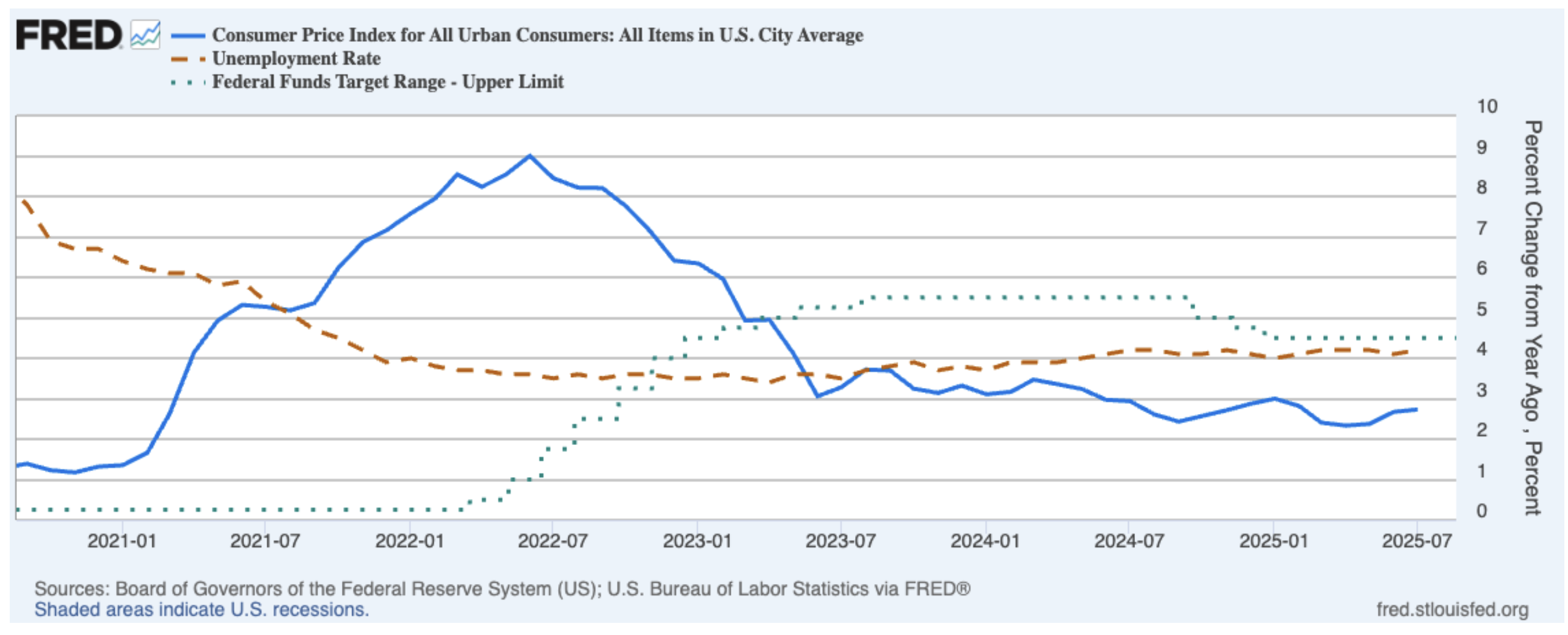

Let’s look at some data in the following chart.

This shows the Fed raised rates to curtail inflation starting in 2022 and stopped in 2023. The time they stopped was right after inflation had fallen below Fed Funds (after the blue and green crossed). It’s historically typical for the Fed to stop around that point. Rates were then cut starting in 2024 soon after the Jackson Hole conference when Powell’s speech included a reference to cuts coming. Since they stopped cutting rates at the end of 2024, unemployment hasn’t really budged while inflation has fallen a very tiny amount.

If I could, I’d ask Jay Powell and his committee about their fears. Outside of when they stopped raising rates, the chart also shows they may have been late in raising rates when inflation was rising, in the hopes that it would wind down on its own (they used the word “transitory” a lot in 2021).

And now that inflation is lower, they may fear that they’ll miss it again in light of the new tariffs. I get that. The last time we had them was 100 years ago, so they are unprecedented in this modern global economy. They want to protect the economy from that awful period of inflation shock we all experienced. As humans, we tend to plan for the last disaster, and the true impact of a tax on imports on the prices we pay is unknown.

I’d also ask them if they should be worried about a potential future where the impact of a tax on imports is actually in the labor market? Where companies cut costs (and employees) to keep their margins the same in the face of higher input costs.

Per the recent Conference Board Measure of CEO Confidence, the share of CEOs expecting some reduction in the size of their workforce over the next 12 months increased for the 5th consecutive quarter to 34% (highest since 2020). In addition, only 19% said they would absorb higher costs and instead planned to increase productivity (93%), negotiate with suppliers (89%), and upskill their workforce (83%).

I believe the Fed should make some cuts this year for insurance against missing a problem with the other side of their mandate on the labor market health.

It’s important to note that markets already do expect some of this. The futures market for Fed Funds is currently showing an 82% probability of a rate cut in September (up from 56% a month ago) and a 45% chance of another cut in October. So if DJ Powell indicates several cuts this Friday, we could get a positive response in the markets. If he continues to focus on inflation in his speech, I would expect a day in the red. His comments on the economy will also drive moves.

Either way, as in past years, it will likely be an important speech.