A short update on our outlook and the debt-ceiling’s impact

A short update on our outlook and the debt-ceiling’s impact

Before I jump into this week’s topic, a word on our outlook in light of briefly hitting official correction territory (-10% from peak levels on the S&P 500 through intra-day Tuesday):

At the start of the year, we expected markets and the economy to benefit from several different factors: deregulation, an increase in M&A activity (benefiting mid-cap equities), continued strength in the labor market and slightly lower interest rates. Taken together, we saw this leading to a S&P 500 target of 6500 — or roughly an 8% return from early December. While we acknowledged tariffs could come into play, we didn’t expect them to be enacted to this extent and would be alongside some of the positives mentioned above.

We also didn’t foresee such a sharp negative swing in sentiment. Sentiment—1 of the 3 keys to the market (earnings growth and interest rates being the others)— has quickly turned negative, leading to the most widely held stocks falling vigorously. While the economy generally still seems like it’s in a decent place, market sentiment can become a self-fulfilling prophecy. Given this shift, we believe GDP growth and earnings growth will be less than we originally anticipated. As a result, I’m lowering my year-end S&P 500 target from 6500 to 6200. We’ll keep watching this space.

Back to regularly-scheduled programming:

We’re heading into another federal government budget deadline (3/14), but beyond the budget, the debt ceiling also looms. The deficit debate isn’t just political theater—it has real market consequences. If and/or when the debt ceiling is raised or suspended, the Treasury will flood the market with new debt. This could push short-term interest rates and borrowing costs higher. For investors, businesses, and consumers alike, this is yet another layer of uncertainty to watch in the months ahead. But let’s take a step back.

The debt ceiling functions as the government’s credit limit—currently set at $36.1 trillion. Once this cap is reached, the government can no longer issue new debt to cover expenses, increasing the risk of running out of cash. While extraordinary accounting measures can provide some short-term flexibility, most analysts expect these measures could be exhausted by June.

America’s checking account

Much like personal finances, the US government has its own bank account—the Treasury General Account (TGA)— the balance currently stands at $542 billion. When the Treasury needs to replenish its funds, it does so by auctioning government securities. Investors can choose whether or not to bid on these securities, but if demand is low, primary dealers—large financial institutions—are required to step in and purchase the remaining Treasuries.

This is important for 2 reasons:

The banks’ role with Treasury auctions

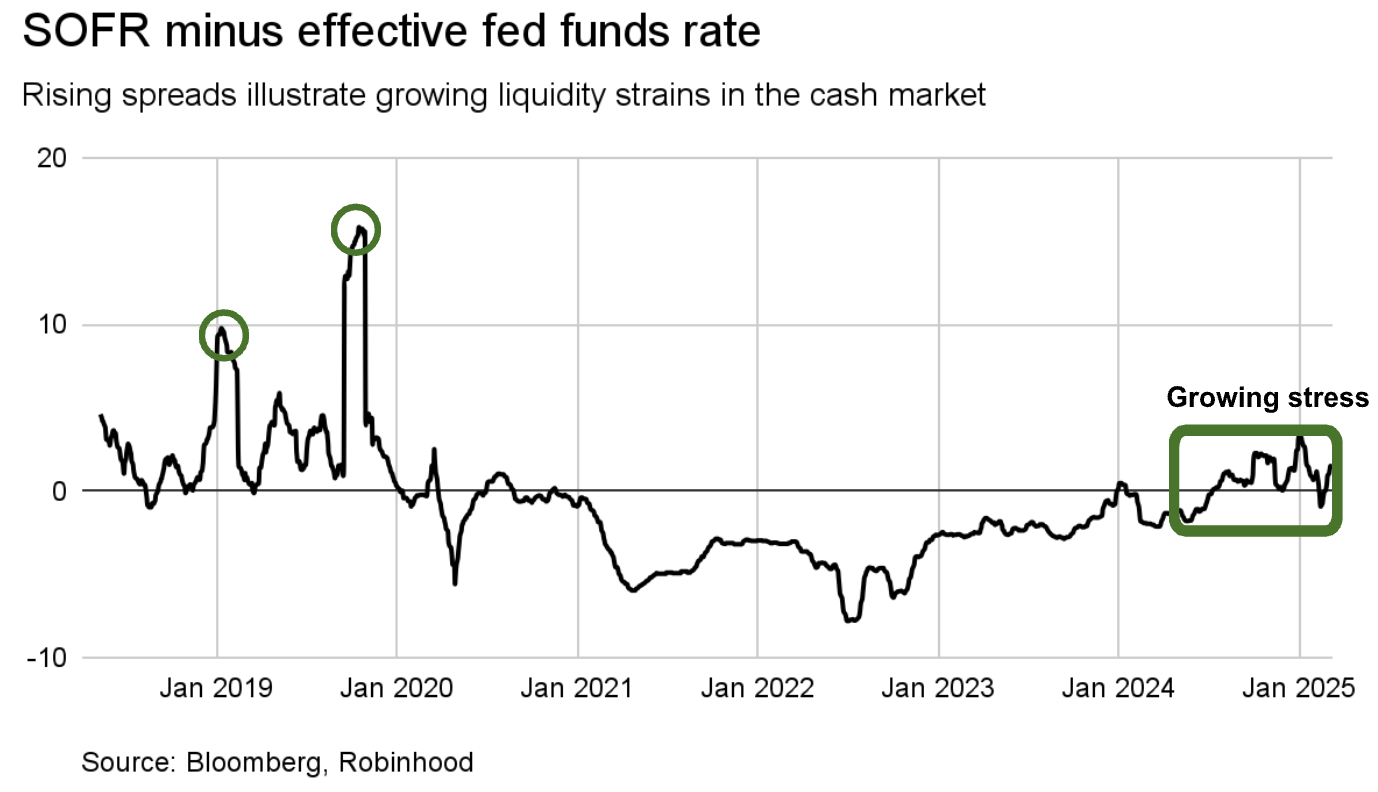

First, these primary dealers include major banks we use every day. To purchase Treasuries, banks often borrow cash in the repo market—a short-term lending market where institutions borrow and lend money overnight. When demand for cash surges, short-term interest rates can rise, pushing them above the Fed’s target range. One way to gauge stress in the repo market is by looking at the spread between the Secured Overnight Financing Rate (SOFR) and the Effective Federal Funds Rate (EFFR).

As shown in the chart below, there have been multiple instances where SOFR spiked well above the effective fed funds rate. The most significant jump in recent history occurred in September 2019 (more details below), where the key takeaway is that stress may be growing. A widening spread suggests demand for cash is exceeding the willingness of dealers to lend. This imbalance adds pressure on short-term rates and overall market liquidity.

2. The Fed’s role in the Treasury account

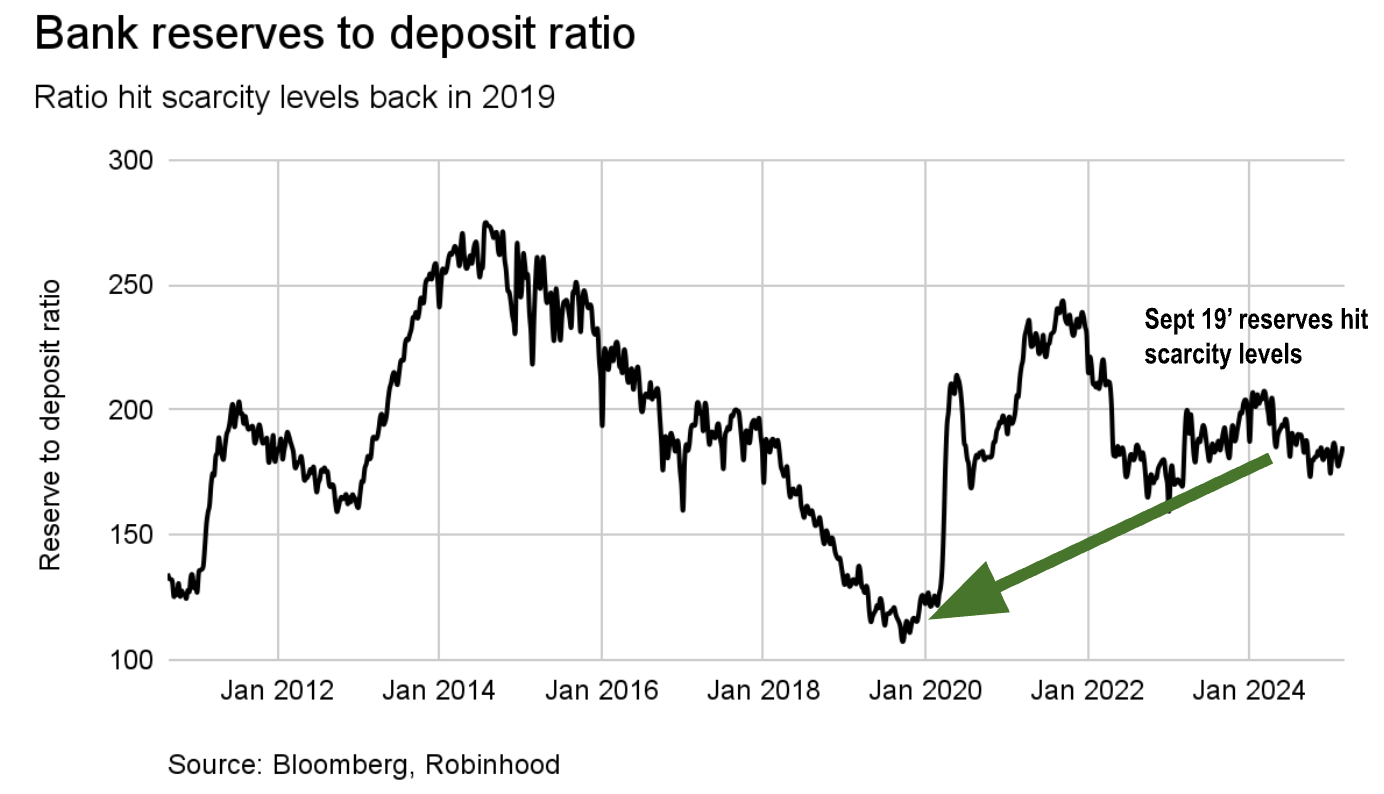

The Federal Reserve is still engaged in quantitative tightening (QT). This allows Treasuries previously bought during QE to roll off its balance sheet rather than buying more of them. When the Fed buys Treasuries, banks receive excess reserves which they can use to increase their lending capacity while staying compliant with regulatory requirements. However, QT does the opposite by gradually bringing down reserves to the minimum needed to remain compliant and maintain lending activity.

Once reserves approach this threshold, banks become more cautious about lending in the repo market, limiting short-term cash availability and potentially putting upward pressure on short-term interest rates.

This happened in September 2019 after a storm of liquidity constraints played out:

QT was already draining reserves, reducing available liquidity.

Firstquarter corporate tax payments were due, leading to over $100 billion in withdrawals as businesses pulled deposits from banks.

$54 billion in newly-issued Treasury securities settled, forcing investors to draw down bank balances even further.

The combination of QT, tax payments, and Treasury settlements strained market liquidity, causing a sharp spike in short-term rates and highlighting the risks of shrinking bank reserves.

So with these pieces, is a repeat of 2019 on the horizon?

It’s a possibility—if and/or when the debt ceiling is raised and the Treasury floods the market with new debt issuance.

This concern is contributing to elevated short-term rates, as investors brace for potential liquidity strains. However, the Fed has tools to prevent another episode, including:

Slowing or pausing QT to help stabilize reserves.

Injecting liquidity into the system through its repo facility, ensuring banks have access to short-term funding.

Still, elevated short-term rates could have real consequences for businesses and households, by increasing borrowing costs and potentially slowing economic activity.

Short-term borrowing rates influenced by the repo market are directly tied to the Secured Overnight Financing Rate (SOFR), which serves as a benchmark for adjustable-rate loans, including adjustable-rate mortgages (ARMs). Lenders typically use a 30-day average SOFR rate as the base for setting interest rates. This means that if short-term rates remain elevated for an extended period, borrowing costs will rise—not just for consumers, but for businesses as well. Smaller companies are particularly vulnerable. Unlike large corporations, which can access bond markets for funding, small businesses rely more heavily on bank loans. Roughly 30% of the debt held by companies in the Russell 2000 is floating-rate debt, compared to just 3% in the S&P 500. As a result, higher short-term interest rates put greater pressure on small firms' profitability, potentially leading to spending cuts, layoffs, or slower expansion.