Next up - bank earnings

Next up - bank earnings

While there has been no lack of market-impacting news the last few weeks, we have technically been in a quiet period. For public companies, that is. And the quiet usually gives the markets anxiety. Similar to human reactions, not hearing about your investments can lead to wondering and negative sentiment.

But that hasn’t happened in the last couple of weeks because the market is aligning to the following:

First, with tariffs starting to be settled and the Big Beautiful Bill being passed, focus can shift more to deregulation.

On another note, markets have shown a preference for softer economic data so that rates can come down—the data has continued to be relatively strong.

Despite this, there are shifts in policies to support demand for bonds (more bond demand potentially equals lower interest rates).

We believe banks, one of the most heavily regulated sectors, could benefit from this, particularly regulation.

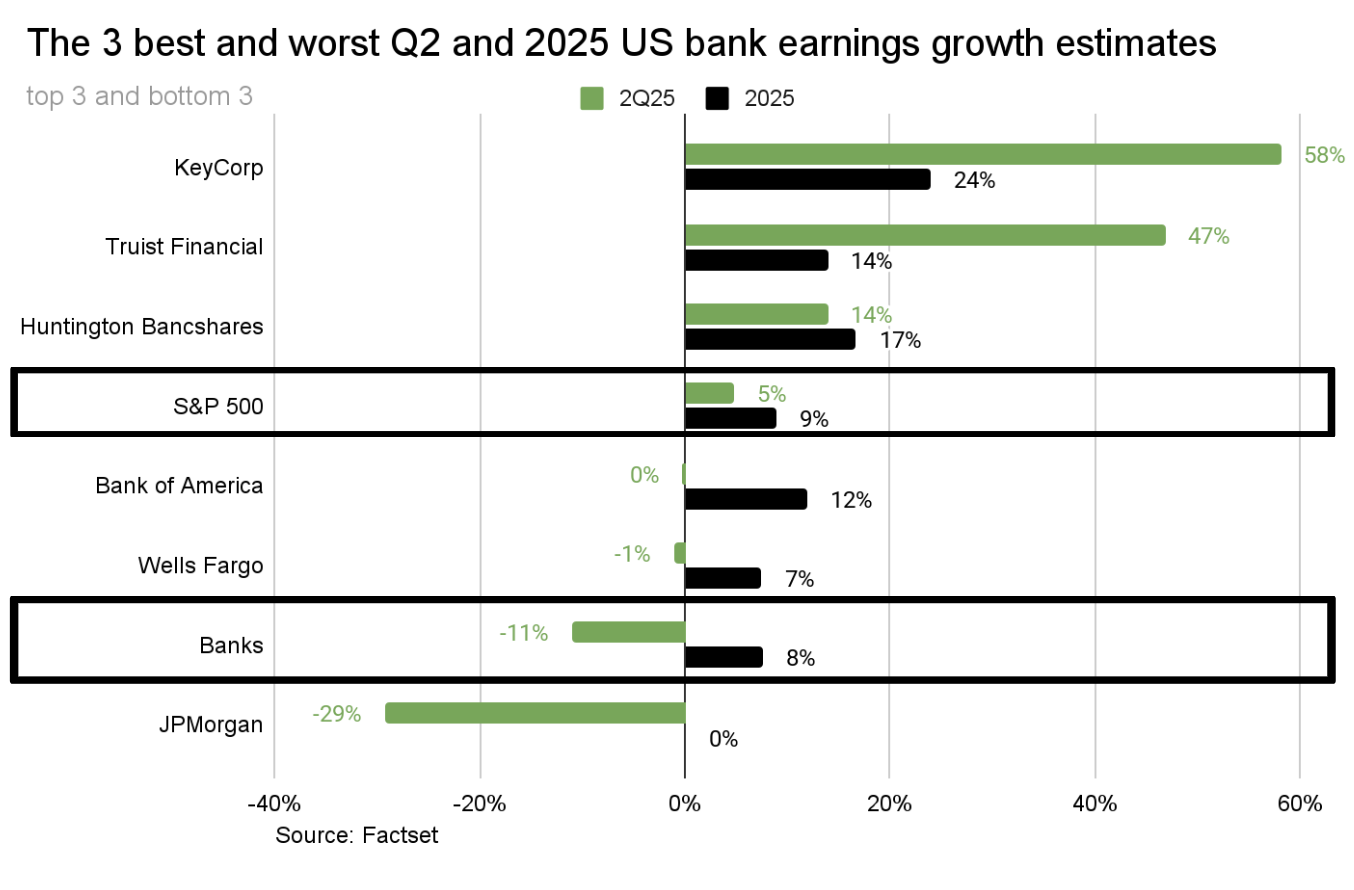

And earnings season kicks off next week with the big banks first out of the gate. Here’s data on expectations:

The banking sector is expected to post a -11% earnings decline for Q2, despite still being on track for 7.5% growth in 2025.

Much of the Q2 weakness is tied to tough year-over-year comparisons. For example, a 29% earnings drop is expected for JPM because it includes a one-off $7.9 billion gain from a sale of long-held Visa shares last year. Excluding that one-time windfall, the sector’s 2Q25 earnings decline estimate would shrink to just under 2%.

For banks, the focus is on their interest rate expectations. Last we checked banks were modeling anywhere from 0 to 4 Fed cuts by year end. A more dovish path could pressure margins, but may also unlock more loan demand, especially if credit conditions stay stable. And if the yield curve steepens, it would actually be positive for margins. We’ll be watching closely for updated rate forecasts and whether loan pipelines are translating into funded balances.

Regulatory policy is also in the spotlight. For example, the recent stress test results and changes to capital requirements like the Supplementary Leverage Ratio (SLR) may give banks more room to maneuver. This could mean more capital is returned via dividends and buybacks. Also, tax relief and some regulatory rollbacks in the Big Beautiful Bill may stimulate broader economic activity and banks’ earnings.

Finally, credit quality will remain under scrutiny, especially in commercial real estate, unsecured consumer lending, and on the consumer side. Deterioration there could quickly shift the tone for the second half of this year.

Heading into bank earnings, the setup looks relatively constructive. However, with tariff policy and rate uncertainty, execution from bank management teams is going to matter more than ever.