Jobs data in a time of no data

Jobs data in a time of no data

There are periods in the market that make you feel as if your partner is away for a weekend with their friends and they’re leaving you on read. Your mind wanders between “are they ok?” to “what are they doing?” While this can happen for the week or two before earnings season starts each quarter(because companies go into their quiet periods)we just finished a prolonged one, thanks to the now longest government shutdown in history ending.

Because with it came a void of economic data. Without the commonly reviewed Bureau of Labor Statistics data, the Challenger, Gray & Christmas Job Cuts Report took on outsized importance — and the details were noteworthy.

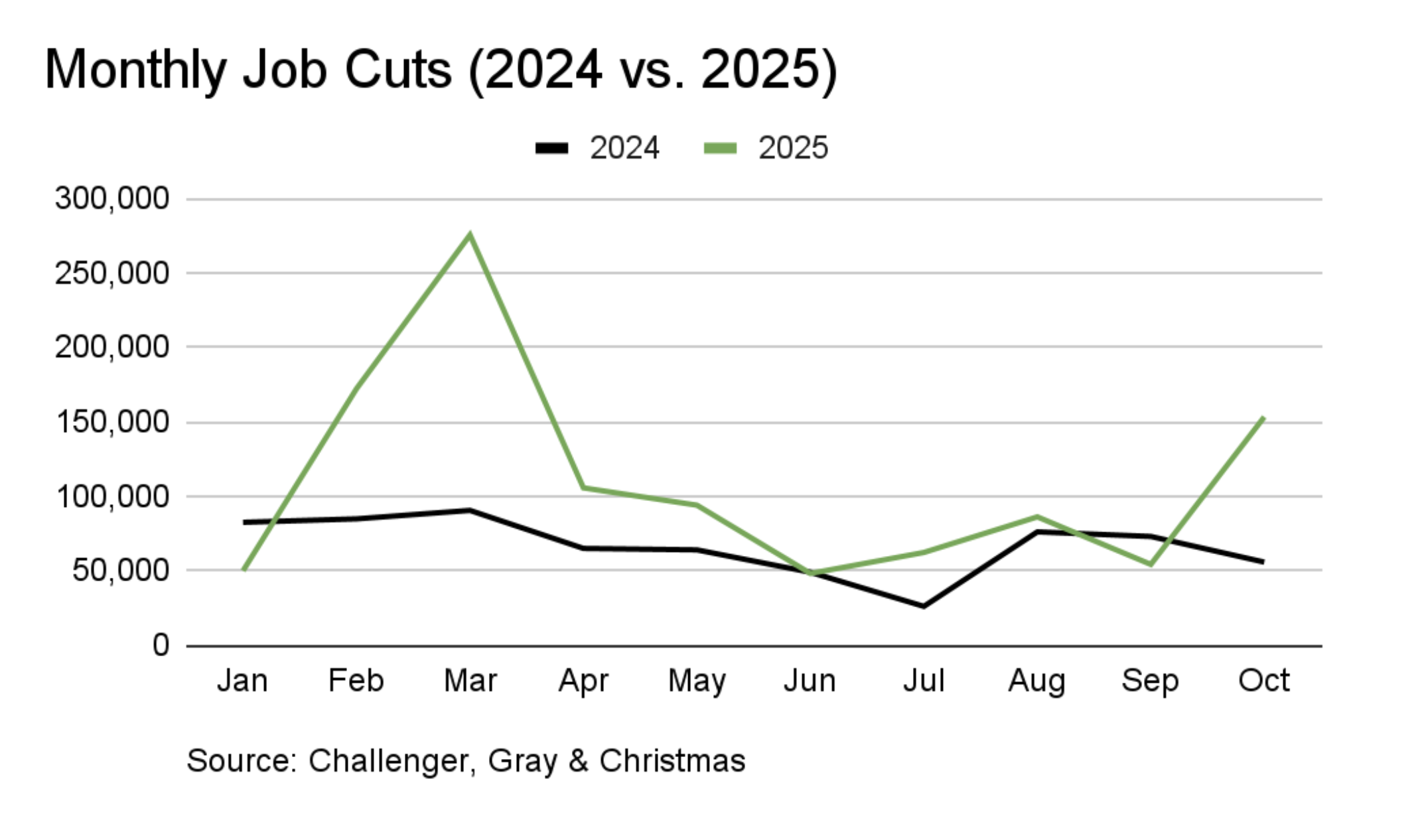

The headline was that employers announced 153,074 job cuts last month, which caught investor attention given that was nearly triple September’s total and the highest October figure since 2003. Through October, total planned cuts for 2025 reached 1,099,500, up 65% from the same period in 2024 — the steepest pace since the pandemic year 2020.

As illustrated above, February and March 2025 saw massive layoffs — over 447,000 cuts combined — largely from federal and contractor reductions under the so-called DOGE Impact. After a calmer summer, October delivered a second wave of 153,000 cuts, driven by cost-cutting across private industries, more cuts during the government shutdown, and AI.

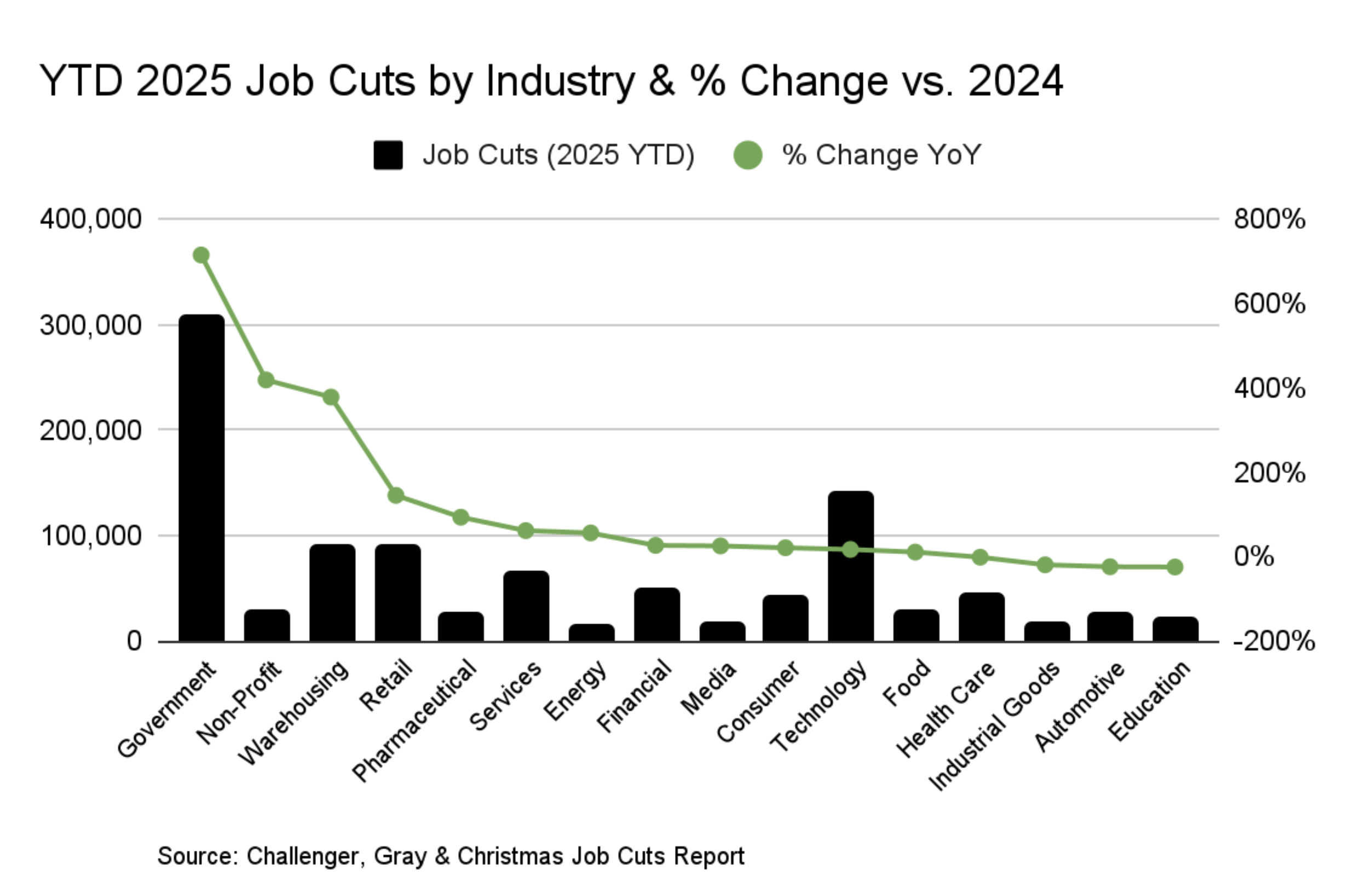

Cost-cutting was the top reason for October layoffs, responsible for 50,437 job reductions. Companies across sectors are paring headcount to preserve margins as input costs rise and demand cools.

Artificial Intelligence ranked second, cited in 31,039 layoffs during the month — roughly one in five October job cuts. Firms are reorganizing teams and automating functions to boost efficiency, bringing AI-related layoffs to 48,414 for the year. This is small compared to the total but something to watch.

Outside of the government, the technology sector continues to lead private-industry reductions. Companies announced 33,281 tech job cuts in October alone, up sixfold from September, for a year-to-date total of 141,159.

Warehousing followed with a dramatic 47,878 layoffs in October, compared with just 984 in September, signaling overcapacity and automation-driven restructuring.

Retail and services also remain under pressure, while non-profits have seen layoffs surge 419% year-over-year (27,651 vs. 5,329), largely from reduced federal support.

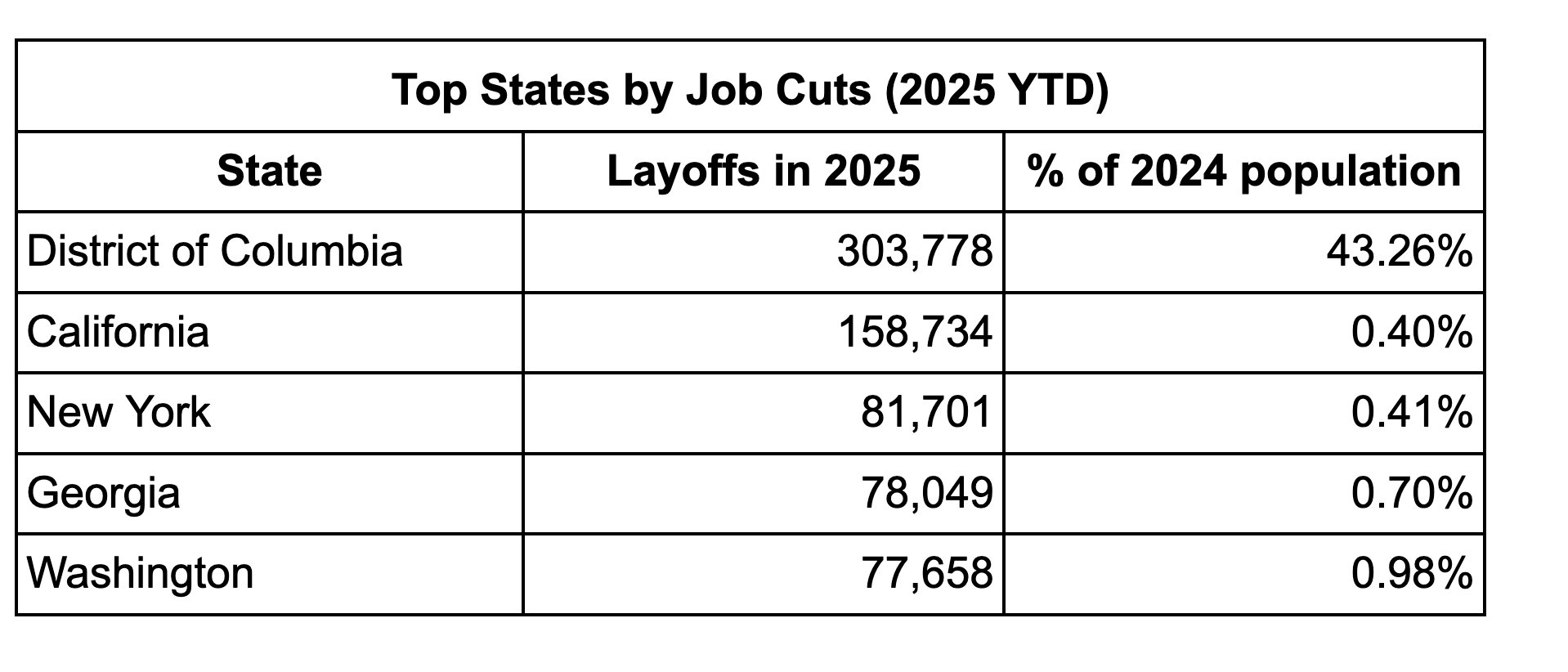

All in, layoffs this year are higher relative to 2024, mostly because of the government’s new administration and cost cutting in tech hubs like Washington state, where Amazon is located.

The thing is, layoff announcements are only half the story. Planned hiring is historically weak so we think we are in a transition. Cost controls are becoming dominant levers while AI recalibration may be starting, as well.

For investors, this phase favors companies that can translate restructuring into productivity gains while preserving growth capacity. To be clear, we don’t believe the US job engine has stalled — but it’s running leaner, and with more automation. This will bring earnings gains, but not without some softness,and wondering, in between.