Value—Or Rather, Low Volatility: A new trend?

Value—Or Rather, Low Volatility: A new trend?

Markets have been swinging lately. Headlines about the trade tariffs, the Fed, and inflation are fueling the volatility. 1%+ moves in a single day, in both stocks and bonds, have become the norm. Tell you something you don’t know.

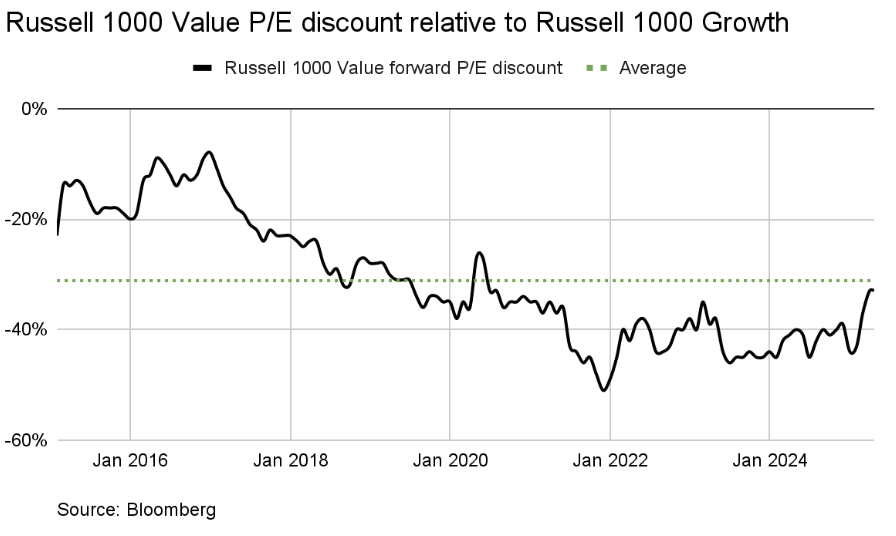

Through it all, what can be called “value stocks” have been outperforming. Value stocks are most commonly defined as companies that trade at lower valuations than the broad market, relative to their earnings, book value, or cash flow.

But that’s just a surface-level view. If you look deeper, it’s actually low volatility and dividend stocks leading the way. They are outperforming growth stocks—and not just by a little. According to Bloomberg, low-volatility stocks are up 3% year-to-date, compared to -10.5% for the Russell 1000 Growth index. This is a reversal from the post-pandemic market, when high-growth names led the charge.

So what exactly are low-volaility stocks?

These are companies whose share prices tend to fluctuate less than the broader market. They often operate in stable, non-cyclical industries, have predictable cash flows, and maintain strong balance sheets.

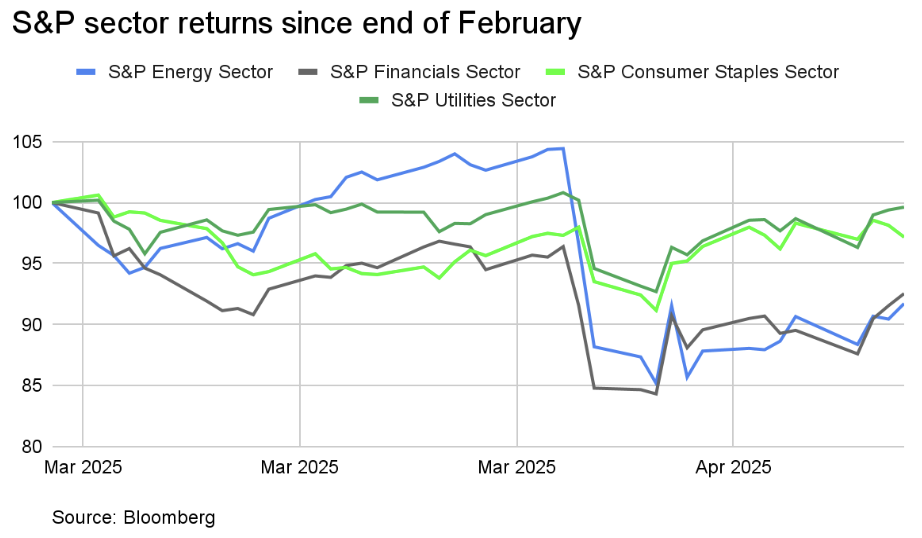

While many dividend-paying stocks fall into this low-volatility category, it's important to note that not all dividend stocks are created equal. The recent outperformance has been concentrated in defensive dividend names—companies that offer reliability regardless of the macro backdrop. Sectors like Utilities, Consumer Staples, and certain parts of Communication Services (particularly traditional telecoms) have benefited from this environment, offering both yield and downside protection.

On the other hand, more cyclical dividend sectors—such as Financials and Energy—haven’t kept up. Recession warnings and global demand uncertainty have weighed on banks and energy companies, even though they often pay attractive dividends. Investors seem to be prioritizing stability and capital preservation over higher—but more volatile—income streams.

The broader takeaway? The market has been rewarding quality over hype, durability over momentum, and stability over speculation.

What about growth stocks?

With talk of a potential Fed pivot—and mounting political pressure to cut rates—it’s fair to ask: is now the time to jump back into growth?

Well, history would say yes—a focus on growth when the world could be slowing down has worked. And typically this is because rate cuts come with it. But this cycle may not follow that script.

For starters, while valuations have come down and are no longer at extremes, they still aren’t very attractive. Many high-growth names like Palantir and Tesla continue to trade at 80–160x forward earnings. That’s a tough multiple to justify with inflation sticky, yields still elevated, and earnings revisions heading lower.

Second, some growth companies face a new headwind: tariffs. Proposed tariffs increase input costs, eat into margins if the costs can’t be passed along, and potentially hit international sales—especially for consumer discretionary names heavily reliant on global supply chains. And tariffs can also contribute to inflation, keeping the Fed at bay from being able to cut rates into slowing growth. Keep in mind, unlike consumer staples, many of these firms could find themselves more limited in their ability to push costs to consumers.

So, is value (aka low volatility) back for good?

Not necessarily forever. But in this kind of environment—high rates, sticky inflation, geopolitical friction, a weaker dollar and earnings risk—low volatility stocks offer a margin of safety that growth just doesn’t.

Importantly, this doesn’t mean piling into every “cheap” stock. Instead seek a more disciplined approach. You want companies with:

Clean balance sheets (low debt, strong cash, and positive working capital)

Consistent free cash flow

Reasonable valuations relative to sector and growth

And be sure to avoid the value traps—those low P/E names with declining fundamentals or structural decline. A cheap stock isn’t a bargain if the business is broken.