Investing in AI’s Next Chapter: Why Software Is the Sweet Spot

Investing in AI’s Next Chapter: Why Software Is the Sweet Spot

Every so often, the world experiences a wave of technological change that reshapes entire industries. Think about that evolution—from carriages to trains, horses to autos and airplanes, or the telegraph to smartphones. These innovations didn’t just change how we lived—they made the world more efficient, productive, and connected.

Today, the pace of innovation is again accelerating with one of the most transformative shifts of our time: the AI revolution.

The AI revolution is unfolding in what we see as three distinct phases: infrastructure, software, and productivity.

The infrastructure phase is all about the physical foundation of AI. This includes semiconductor companies whose chips power AI systems, and the massive data centers needed to store and process all that information.

This is a big reason why you’ve seen such explosive growth in stocks like Nvidia and Broadcom.

Not to mention all the energy needed to power it throughout these phases.

Then comes the software phase, where AI becomes usable. At this point software companies and IT providers begin integrating AI into tools that people and businesses can actually use.

Finally, there’s the productivity phase—where AI starts to truly reshape industries, replacing tasks, and in some cases, even jobs.

Transitioning from infrastructure to software phase

In our view, we’re moving out of the infrastructure phase and more fully into the software phase.

Two big drivers of the infrastructure buildout have been chips and energy. You need both to get AI systems off the ground. Over the past year, tech giants have poured billions into acquiring high-performance chips and building up energy capacity to power their models. As a consequence, companies like Nvidia and Constellation Energy saw explosive revenue growth.

So, why the shift?

The recent release of DeepSeek, a powerful open-source AI model from China, raised new questions as to just how much computing power and energy is actually needed. DeepSeek is able to deliver cutting-edge performance on par with those models produced by OpenAI with lower cost.

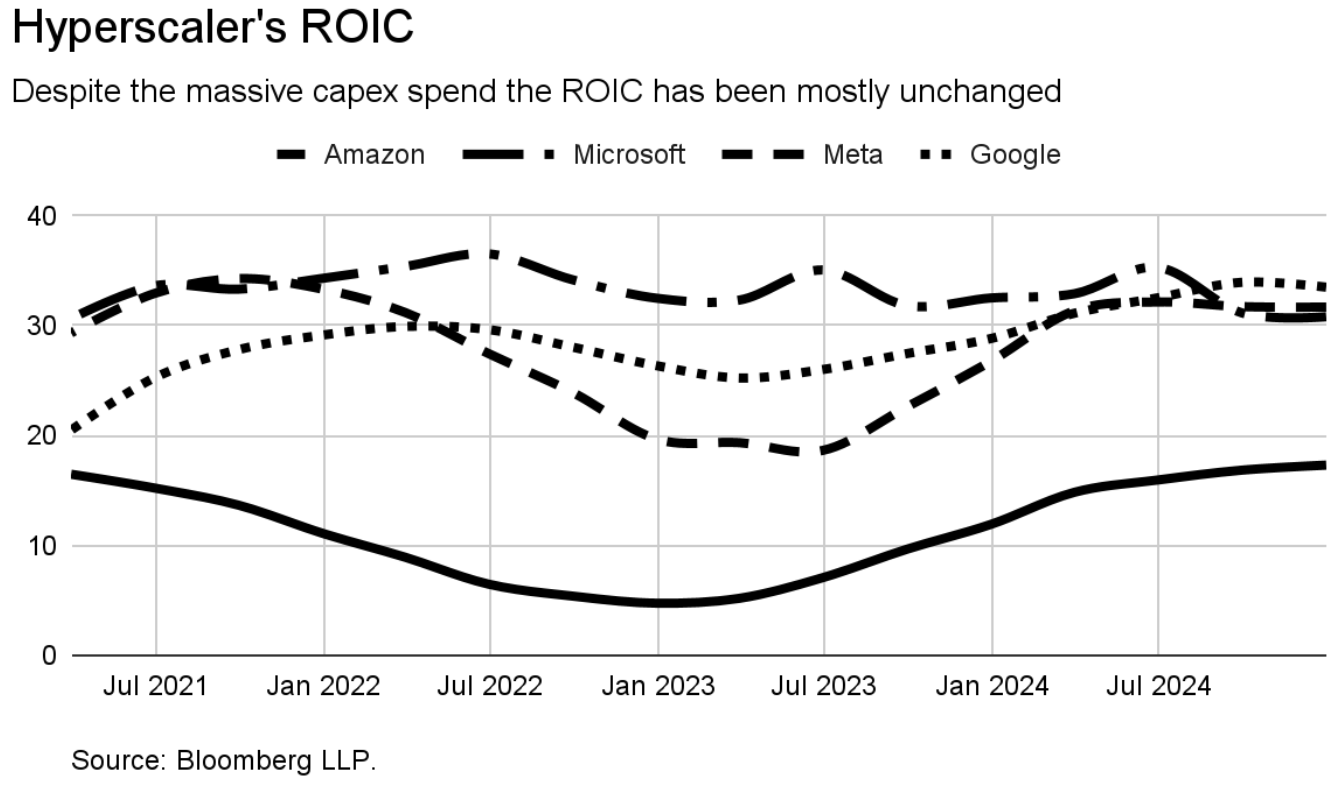

Despite the wave of infrastructure investment that began in 2023, return on invested capital (ROIC) among hyperscalers — i.e. large tech companies that operate massive cloud infrastructure, enabling them to scale computing resources rapidly and efficiently — has merely returned to pre-investment levels. This lack of improvement in capital efficiency has made investors uneasy about the long-term returns on these infrastructure bets.

The software phase may be where the real value emerges

We’re entering a new era where products and services will be fully tailored to individual users, powered by AI. This phase is expected to be defined by the rise of chatbots, copilots, and autonomous AI agents. Tech giants like Amazon, Microsoft, Meta, and Google are leading the charge, but a growing number of startups are jumping in, thanks in part to open-source models.

These models are lowering the barriers to entry, allowing emerging companies to build powerful AI software without significant capex investments. According to PitchBook, nearly 1 in 4 new startups today is AI-focused.

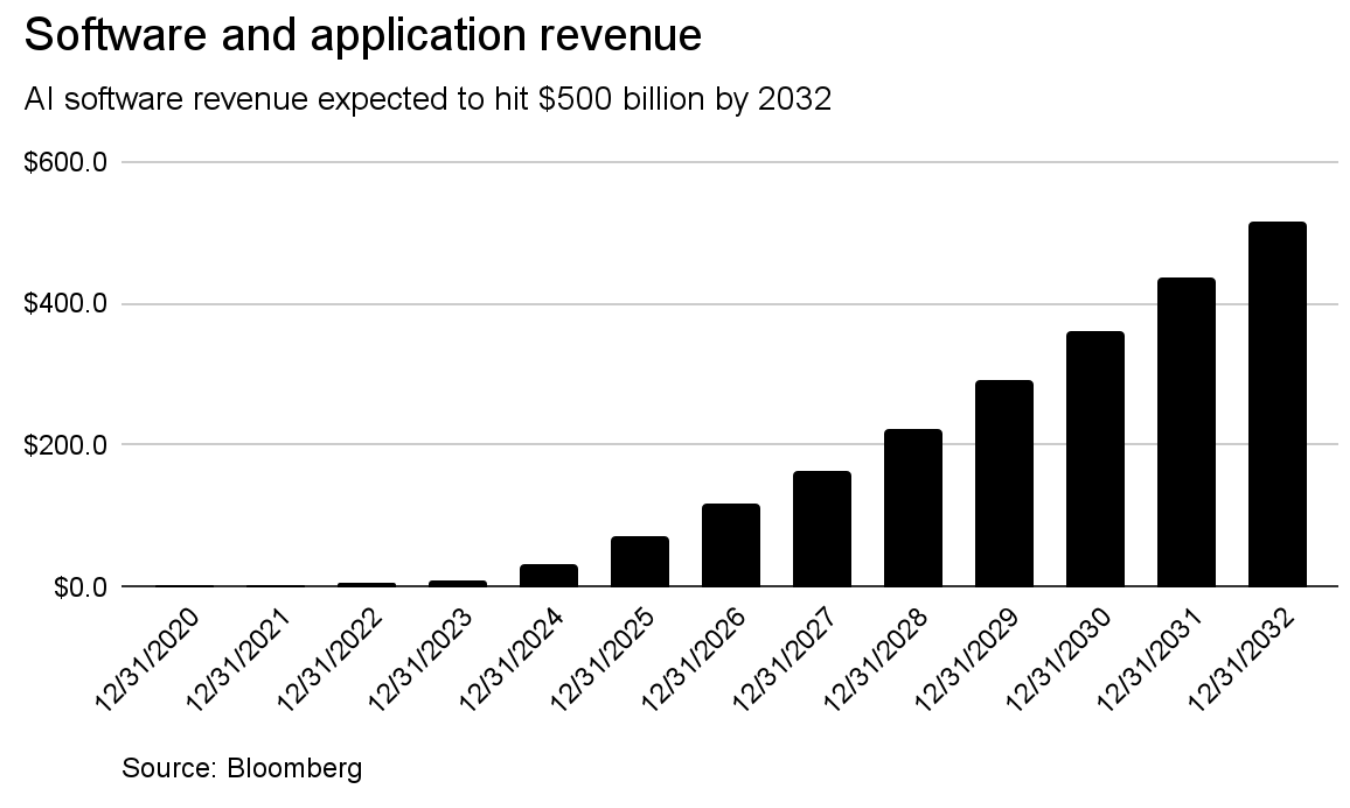

The race isn’t random—it’s driven by high expectations. The AI software industry is projected to exceed $500 billion by 2037, with revenue forecasts growing at a significantly faster pace than the infrastructure segment. Over the next seven years, software is expected to grow at a 48.4% compound annual growth rate (CAGR), compared to 15.9% for infrastructure.

Historically, the software/application phase is where the majority of value creation occurs. A clear example of this dynamic is the telecom sector versus streaming services. During the 90s and 00’s telecom giants like Verizon and AT&T invested heavily in fiber optic and broadband networks—critical infrastructure that made streaming possible. But it was Netflix, built on top of that infrastructure, that ultimately captured more value. Today, the combined market cap of Verizon and AT&T still trails that of Netflix.

All of this sets the stage for the final phase: productivity

If history tells us anything, it’s that big productivity gains tend to follow big technological breakthroughs. Back in the late 1990s, the IT boom—driven by the spread of computers and the internet—pushed U.S. productivity growth up to around 2.5–3% a year. Even after the dot-com bubble burst, the 2001 recession hit, and the shock of 9/11, productivity actually accelerated. By the early 2000s, productivity was hitting 3–4% annually as companies started to reap the benefits of their earlier tech investments and focused on doing more with less.

But the stock market told a different story. The market is a forward discounting mechanism. This means it looks ahead to these possibilities before they arrive in the data–and can get ahead of itself. In 2001, the NASDAQ crashed 78% from its 2000 peak, and the S&P 500 lost nearly half its value. It wasn’t until 2007 that the market fully recovered—thanks in large part to aggressive rate cuts and loose monetary policy. In other words, productivity soared while overvaluation and investor burnout tanked the markets.

Fast forward to today, and we’re seeing early signs that AI could follow a similar path—though we’re still in the early innings. Right now, U.S. productivity growth is hovering around 1–1.5%, but if AI adoption accelerates, it could rise meaningfully in the years ahead. So far, for the stock market, the comparisons are mixed. As of April 2025, the S&P 500 is down 8.3% from its February high, and the NASDAQ has dropped 13.5%. That’s a notable pullback, but nothing like the wipeout we saw in the early 2000s. Valuations today are also more grounded—P/E ratios are sitting around 25–30, compared to the dot-com days when many stocks were trading at 60 to 100 times earnings, often with no profits to show.

Here’s the key difference: back then, the productivity gains were already happening, giving the economy some momentum even as the markets fell apart. Today, with AI, we’re still waiting. The infrastructure is in place, and expectations are sky-high—but the real payoff will depend on how well companies adopt, scale, and integrate AI into their day-to-day operations. Investors takeaway As AI enters its most lucrative phase, investors should position themselves not just for who builds the future—but who makes it usable. For investors, this means broadening your attention beyond the suppliers of chips, servers and energy to include the builders of intelligent, usable software.