Don’t know what to call it and Fed independence

Don’t know what to call it and Fed independence

The mountain breeze, the starry night sky, and the company I was with made listening to a little cover band outdoors recently a night to remember. They were the “Red Not Chili Peppers” and they might as well have been the real thing. With incredible guitarists and a lead singer who was having the time of his life dancing and doing handstands on stage, it was infectious (and made me love the music).

One song in particular hit me that I had forgotten about, from the band’s later years (2006), was “Snow (Hey Oh)”. When they sing:

The more I see, the less I know

The more I like to let it go

Because even in just these first 8 months of this year, things have happened in the markets and in policy from the executive branch of our government that I didn’t fully, or at all, have on my radar at the start of the year. The more I saw, the less I knew. Ultimately, tactically investing based on what we hear from POTUS and Treasury Secretary Bessent has become a real thing over the last few months for us. I’m still not sure what to name it.

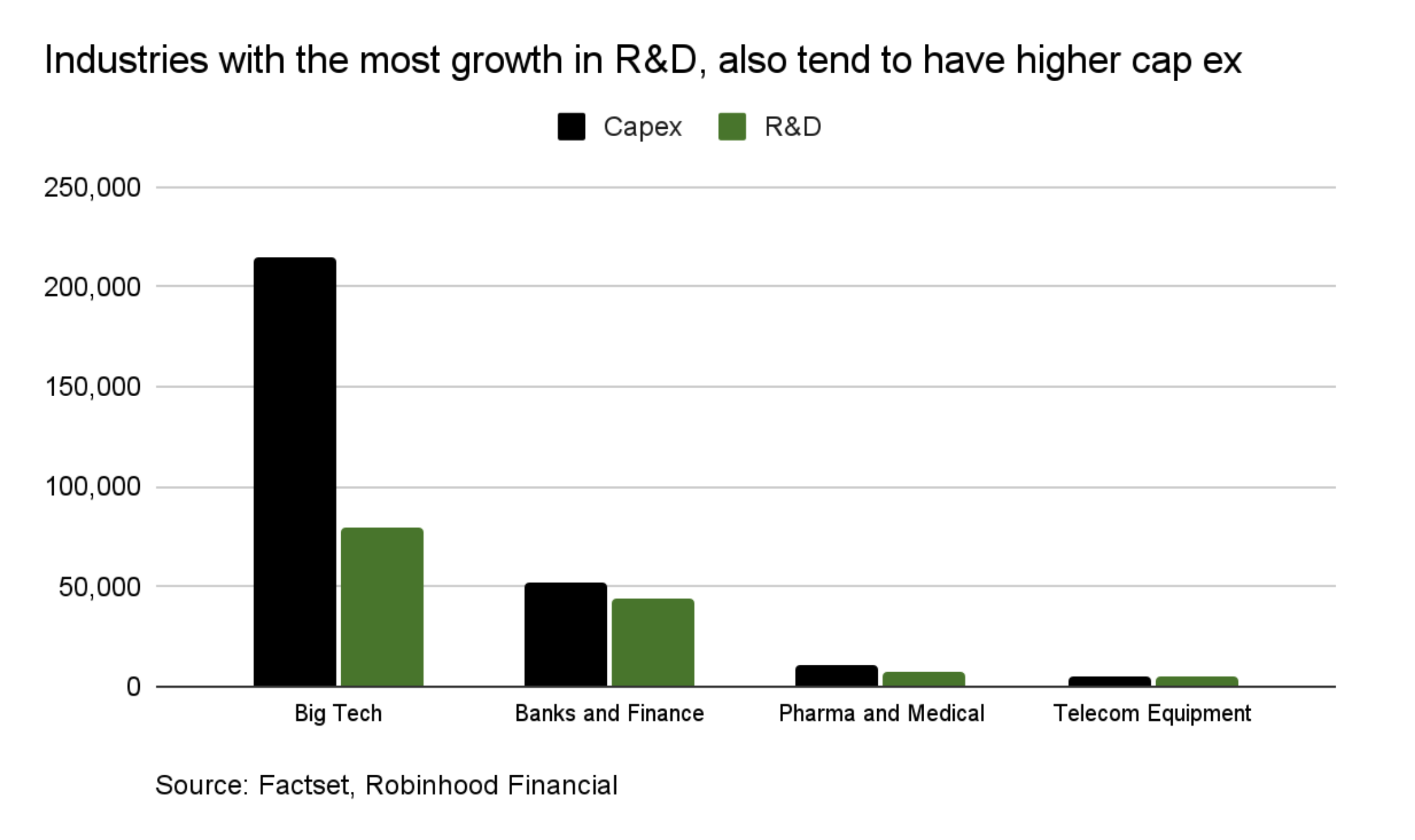

But examples include focusing on companies that will benefit from the One Big Beautiful Bill’s (OBBB) tax incentive—like 100% immediate expensing of domestic capital expenditures (capex) and research and development (R&D)—and its many potential advantages for the aerospace and defense sector, which still seem to have legs.

For capex and R&D expected growth, within the S&P 500:

While the big spenders on data centers and power are apparent here, R&D is also high in pharma and in large and regional banks. Those with the most R&D spending should all benefit from the shift under the OBBB. We’ll just need to watch how future sectoral tariffs impact pharma.

Oh, and another shift:

The Fed’s independence has been in question for a bit but even more so now. It’s clear there is a desire to change the way the Fed works today. Perhaps it's because the many years of quantitative easing entwined the Fed and the Treasury more than it should have (when the Fed bloated up its balance sheet with treasuries to support the economy post the Global Financial Crisis in 2008 and again during Covid).

Or it’s another move to change our economy’s structure.

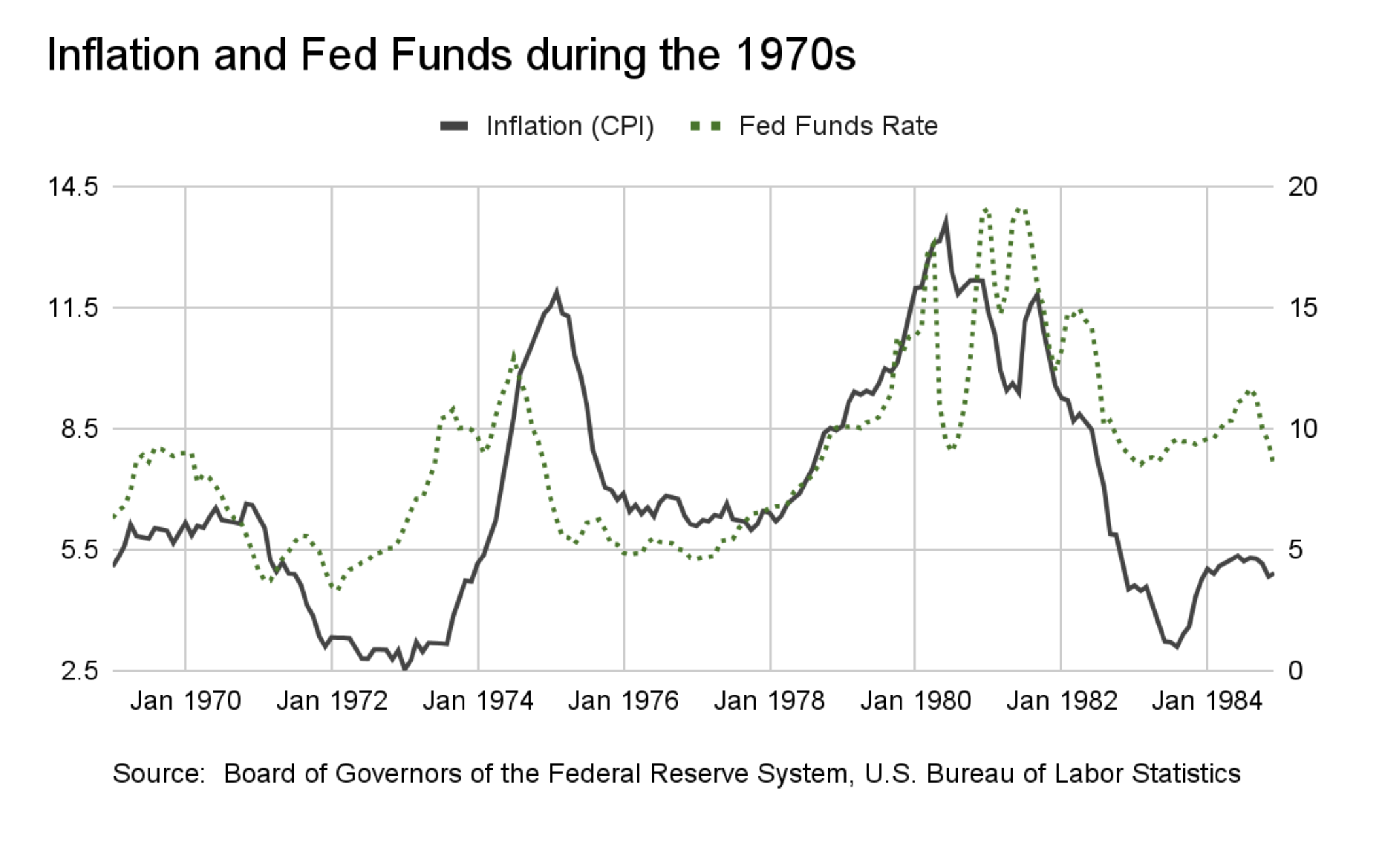

Personally, I like the idea of an independent Fed. In the early 1970s, when inflation was high but temporarily pushed down by wage and price controls (1971-1973), Fed Chairman Burns decided, under well-evidenced pressure from President Nixon at the time, that raising rates couldn’t help the problem. In 1971, Burns said “we should regard continuing cost increases as a structural problem not amenable to macro-economic measures.” And he actually lowered rates during this time. So while this monetary stimulus helped to boost the economy in time for the 1972 election, and Nixon’s presidential election victory, the excessive aggregate demand stimulation created a problem. Inflation spiked again in 1974 and it took nearly a decade to resolve. The economic situation isn’t exactly the same today—but there is a lesson here.

So I prefer the Fed be able to do its job on its own, even if some things about the way the Fed works needs to be updated.

But, you know what, like the song says, the more I see, the less I know, and for now, I’m going to let it go. There are bigger things to consider—for now.

Source: Journal of Economic Perspectives—Volume 20, Number 4—Fall 2006; How Richard Nixon Pressured Arthur Burns: Evidence from the Nixon Tapes.