Do we have inflation or not?

Do we have inflation or not?

Yeah, we do.

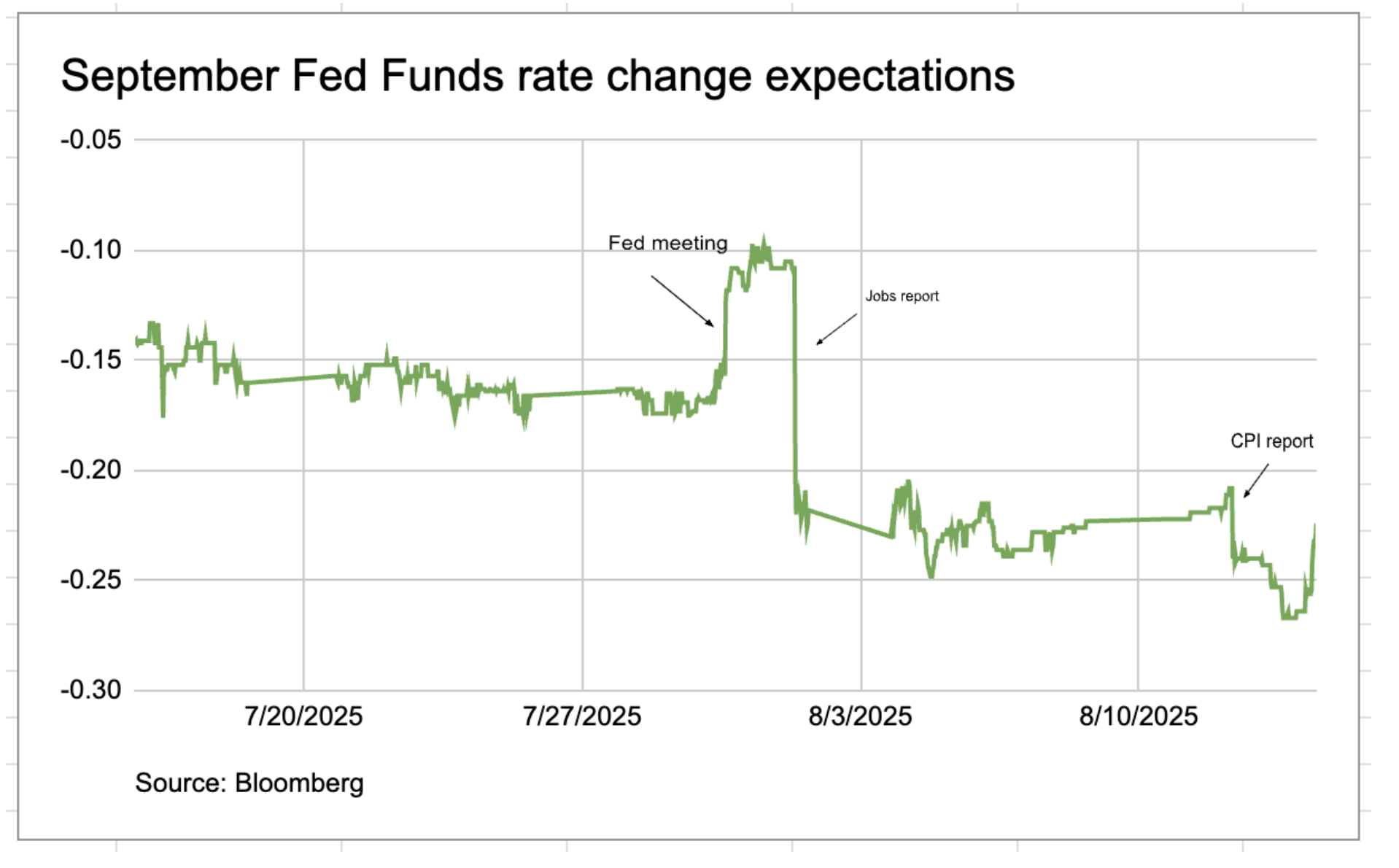

But Tuesday’s Consumer Price Index (CPI) report got the market excited because the vibe was “oh, it could have been worse.” This is because there was an expectation that this week’s inflation report would be the first one that could begin to reflect the impact of tariffs on prices. This led to expectations of a Fed rate cut in September, because inflation is a component of interest rates. In the chart below, the lower number means a bigger cut expectation.

Let’s look at the inflation numbers:

CPI came in at +0.2% M/M and +2.7% Y/Y—the same as June and a tiny bit cooler than the Street’s +2.8% forecast. Core CPI came in at +0.3% M/M (inline) and +3.1% Y/Y—up from +2.9% in June and only a bit warmer than the Street’s +3% forecast.

But there is a case to be made that, given the rush of importing inventories pre-April 2nd and the additional rush between “the pause” and July when deals began to be struck, the current goods being sold in the US do not yet fully reflect the future cost that could come in a higher tariff world.

In fact, the Producer Price Index from today showed a much higher than expected set of numbers:

Headline increased 0.9% m/m vs consensus for 0.2% rise, which is 3.3% YoY, hotter than 2.4% consensus.

Core PPI (ex-Food & Energy) also rose 0.9% m/m vs consensus for 0.2% increase, bringing the YoY number to 3.7%, well ahead of 2.9% consensus.

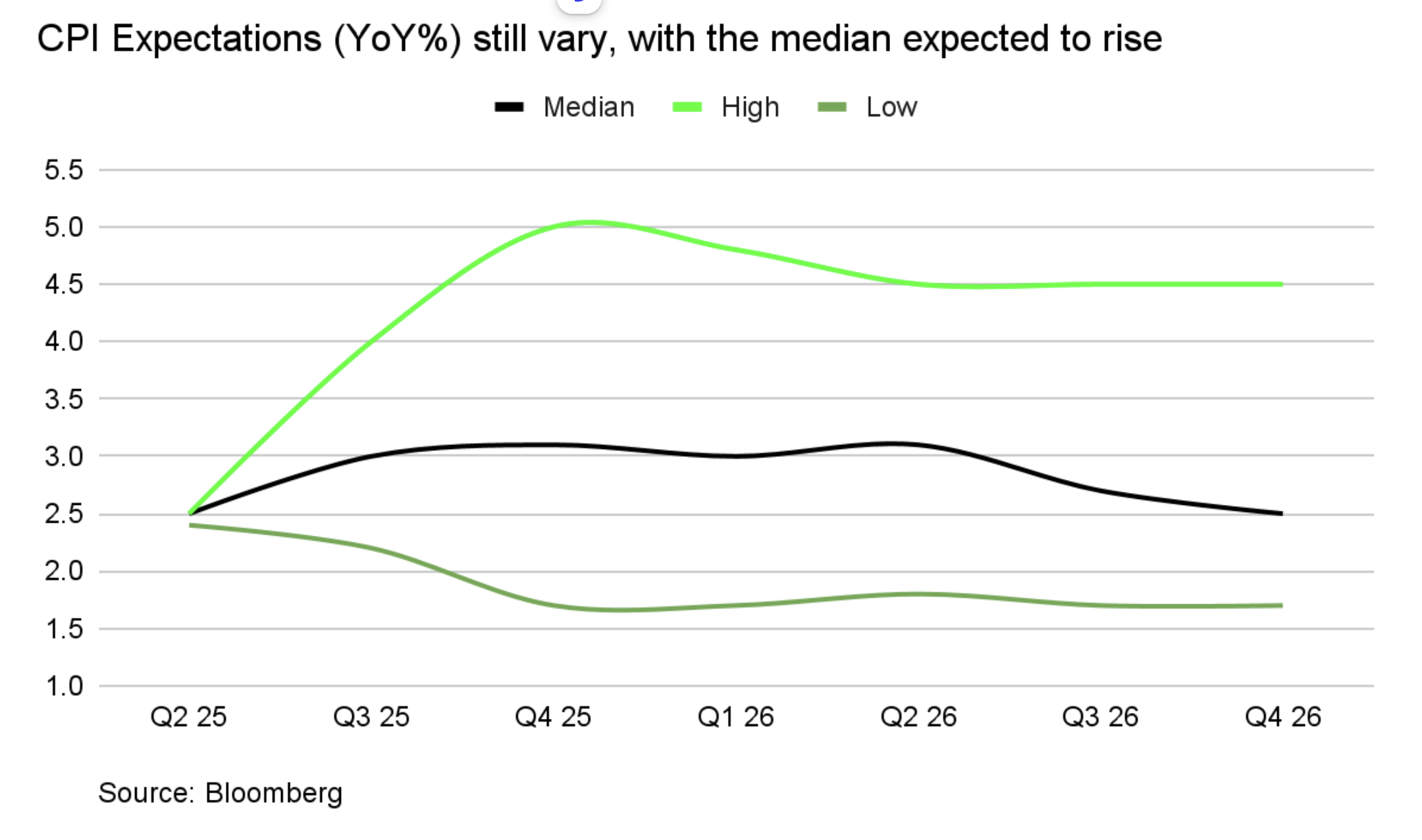

In investing, expectations are everything—from earnings to interest rates to inflation. The actual numbers are less relevant for market moves than the relative numbers. So let’s look at what expectations of inflation for the rest of the year are, based on a survey of market participants:

You can see, even with the recent CPI report that looked ok, there is still a mild expectation for inflation to rise. The question for interest rates—and thus market valuations—is whether inflation will be worse than this or better. If worse, then interest rate expectations will rise again, and markets will likely correct. The next set of inflation data is in September (9/10 for PPI and 9/11 for CPI). But also pay attention to Powell’s speech at the Jackson Hole Symposium, expected August 22nd.