Halftime: markets wrapped

Halftime: markets wrapped

The first half of the year came with its share of challenges, including global tariffs, a cooling economy, and geopolitical tensions. Despite these headwinds, markets broadly ended H1 on a relatively positive note.

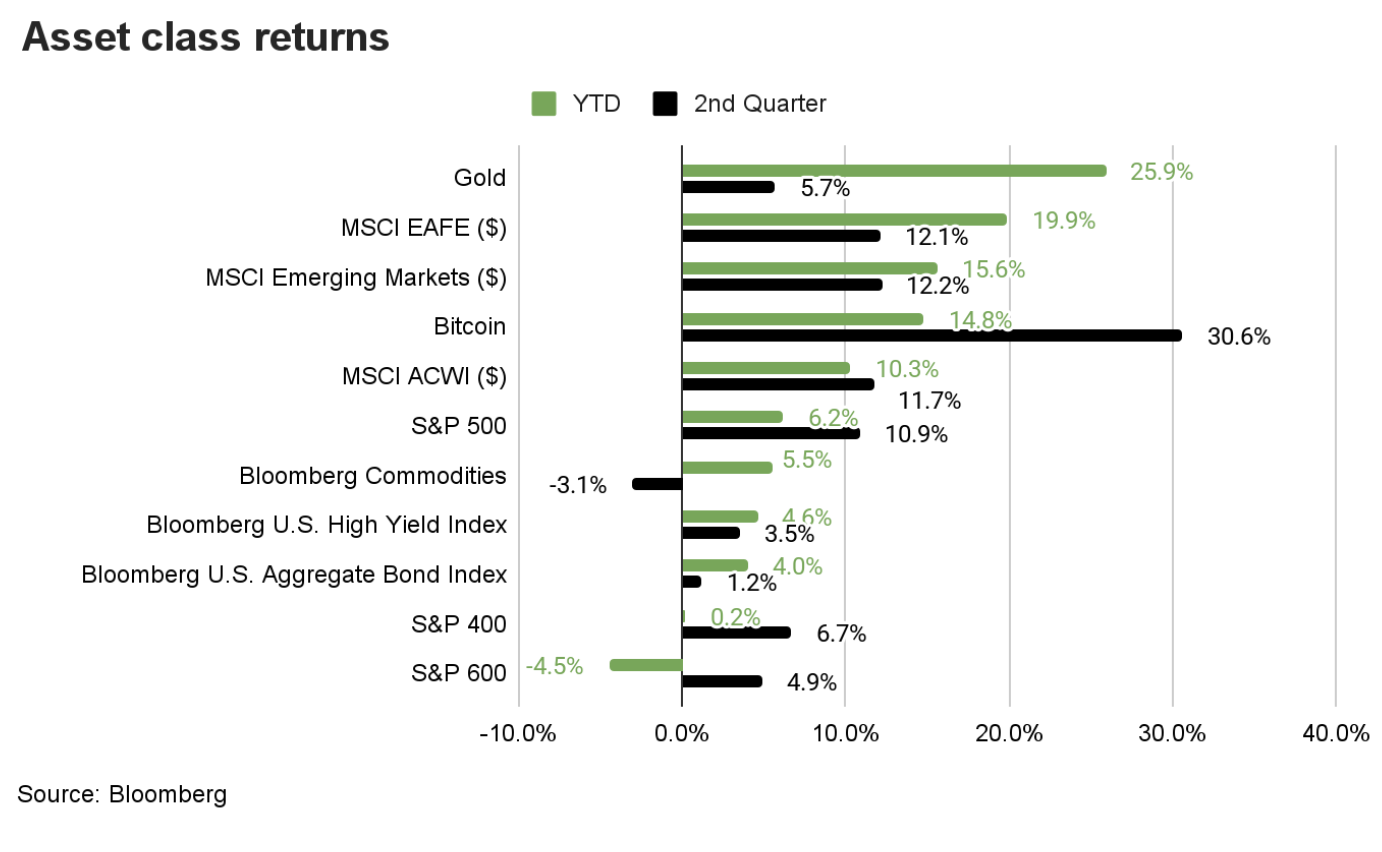

US stocks gained ground towards the end of the second quarter, pushing year-to-date returns into positive territory.

Note: S&P 400 is a mid cap index, S&P 600 is a small cap index.

Technology was especially strong, rising 23.7% and continuing its multi-year run of outperformance. However, the top-performing sector so far this year has been industrials. This has been driven in part by gains in aerospace and defense, supported by changes in foreign policy and geopolitical conflict.

For example, the Trump administration’s proposed $1 trillion defense budget for fiscal year 2026 includes $961 billion earmarked for the Pentagon, which would bring defense spending to approximately 3% of GDP.

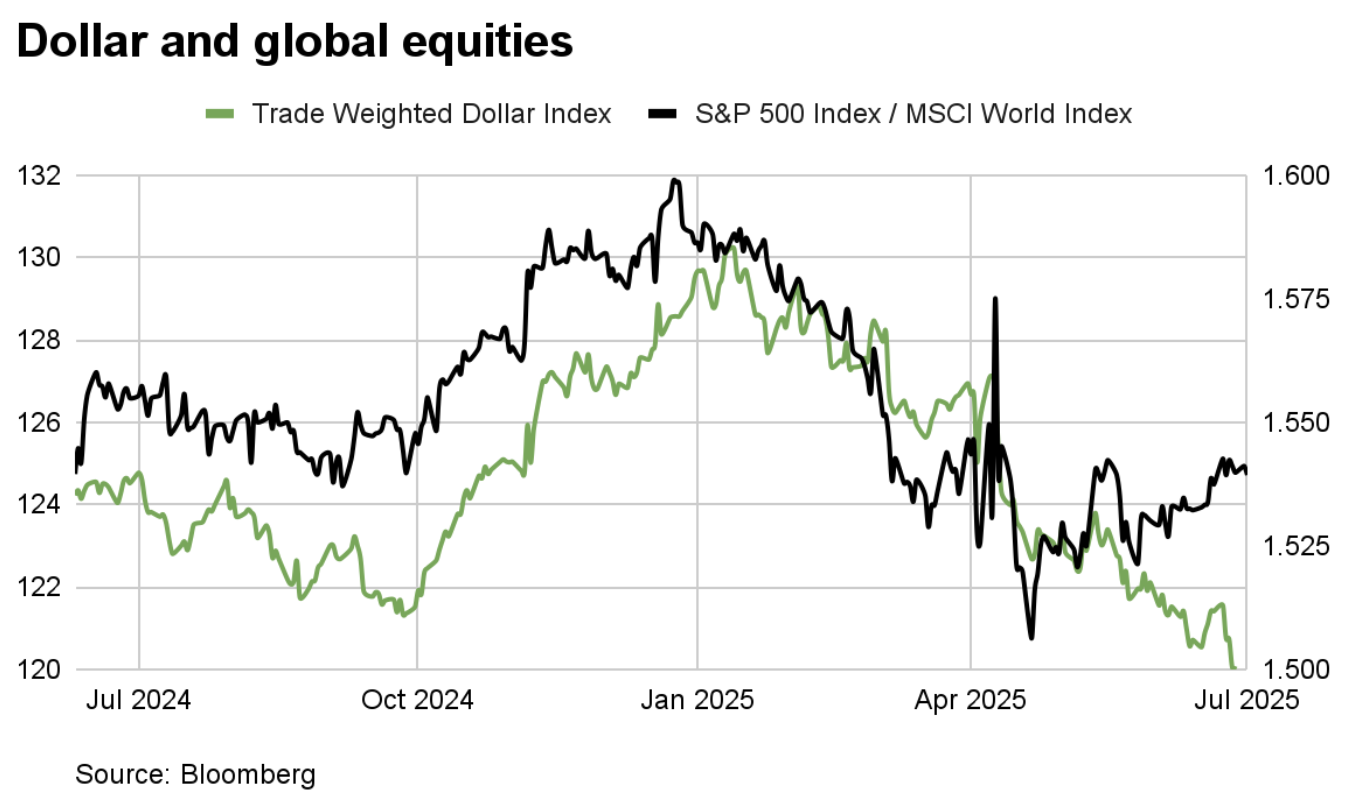

Even with a solid 2nd quarter, US equities lagged international markets. A weaker US dollar helped boost returns for foreign equities when translated back into dollars. The dollar has been under pressure due to several factors, including monetary policy, growing trade tensions, and rising concerns about the federal deficit. This makes international exposure an increasingly important part of a well-diversified portfolio.

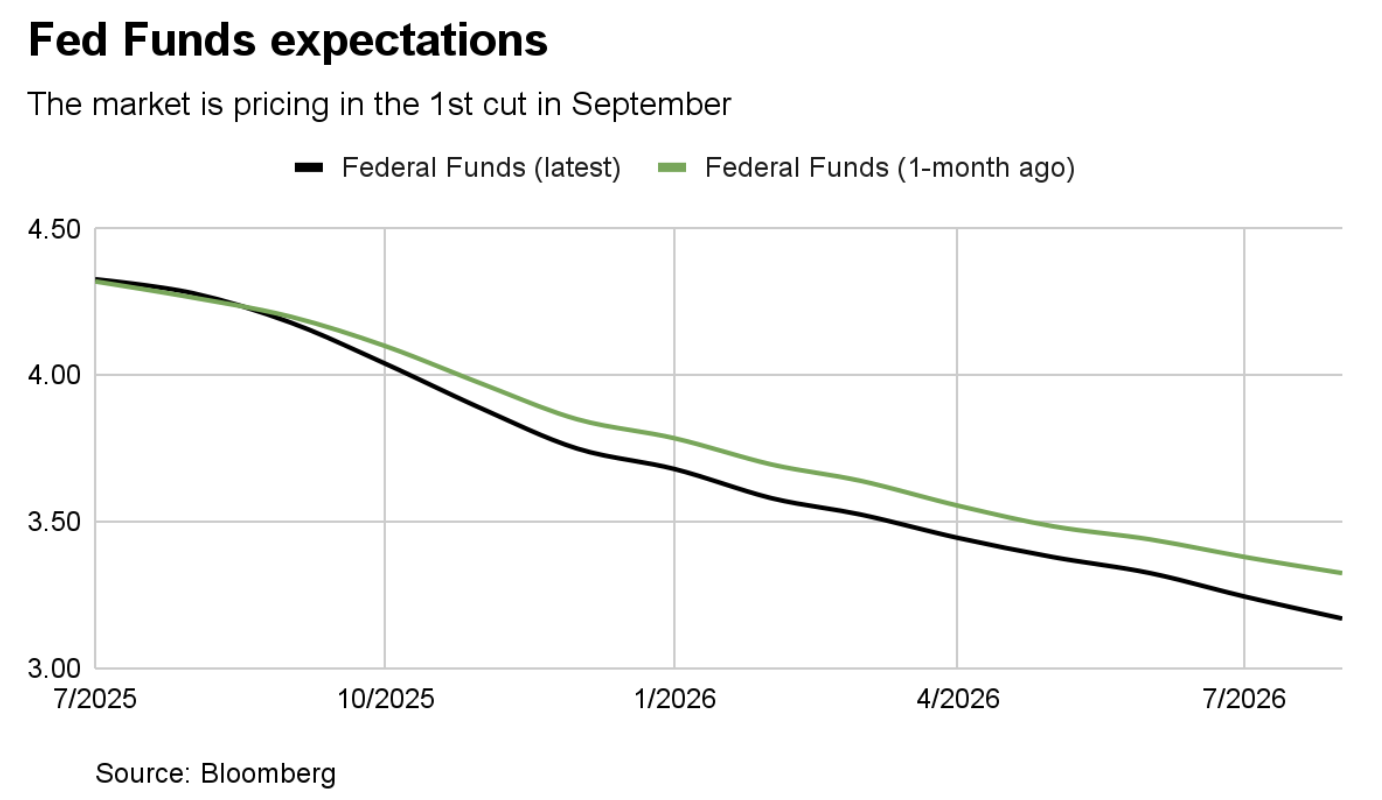

For bonds, yields fell steadily after peaking in January. There are two forces at play here: slowing economic growth expectations pushing down inflation expectations and longer-term yields, while hopes of a rate cut lower shorter-term yields. This resulted in bonds getting a bit of a lift, up 4% year-to-date.

We expect rate cut expectations to remain a key focus for markets. So far, the Fed has held off on easing, in part to see whether inflation pressures stemming from tariffs actually pass through. However, a recent report suggested that President Trump may appoint Fed Chair Jerome Powell’s replacement as early as this fall as a “shadow role.” While a shadow Fed chair can’t action anything, they can talk about their plans for next year. Even without a formal replacement, the mere perception of weakened independence could shift expectations toward a more dovish policy stance.

In other markets, Bitcoin passed $111,000 for the first time, supported by regulations, rising institutional interest, and renewed optimism about crypto adoption. Oil prices were more volatile. Crude fell during the year, spiked in June due to geopolitical headlines, and retreated as the ceasefire came into focus. By quarter-end, Brent crude had settled at $68 per barrel. Commodities were positive for the first year, mostly down to the expansive return of Gold.

Looking ahead: US policy in focus

As we enter the second half of the year, US policy is likely to play a central role in shaping market performance and driving volatility. One area to watch closely is the progress of the Big Beautiful Bill (BBB), which is currently making its way through Congress. The bill recently passed the Senate with amendments and is now under review by the House of Representatives.

According to the Congressional Budget Office, the Senate version of the bill would add approximately $3.3 trillion to the federal deficit over the next 10 years. The final cost will depend on the outcome of House negotiations, but we expect the price tag to remain substantial. With policy risk at the forefront, investors should stay agile. We’ll be back with a full mid-year outlook soon.

In the meantime, happy 4th of July!