And mostly just dance for me: Nvidia, jobs and the Fed

And mostly just dance for me: Nvidia, jobs and the Fed

At a recent concert, the legendary singer-songwriter Stevie Nicks, a woman in her late 70’s with a sultry voice, sent us off at the evening’s end with a message: “Dance on your way to the kitchen, dance on your way to the TV because you can’t sleep and mostly just dance for me.”

This hit me as I thought about how much this woman has gone through in her life, how I may never get to see her sing live again, and that, in that moment, I realized “dancing” through the ups and downs of life is one of its own inherent meanings.

Markets move in a rhythm too. There are ups and downs. Staying measured to the beat—without becoming too greedy or too fearful—becomes a practice in self-awareness. How do you stay grounded through volatility?

For me it comes back to my core investment belief: expectations are everything.

Let’s talk about that in the context of Nvidia. Looking back over the last years, few companies have set expectations (or defied them as much over time) like Nvidia. For 2023, earnings estimate revisions (adjustments to expectations) were tripled during the year, from $0.42 per share to $1.21 per share. And for 2024, they were doubled, from about $1.62 to $2.84. But inevitably, earnings expectations catch up. By the end of 2024, earnings estimate revisions for 2025 have leveled off, hovering around $4.40 per share. While it’s true 2026 and 2027 earnings estimates have been revised higher this year, with 50% growth rates expected, it goes without saying that there is a limit to all of it. Add in that investors have started to ask for economic validation of the AI spending boom, and you’ve got a symphony primed for disappointment.

Nvidia did beat expectations on both revenue and earnings this week. And the market liked it at first.

But this confused me, to be honest. Mostly because they didn’t beat expectations to the same level in the past.

And when you get into the details of their report, there’s a data point that raised eyebrows: the “net operating cycle” increased from 85 days to 101 days, the highest levels since January 2024. This fueled concerns around the time to monetization.

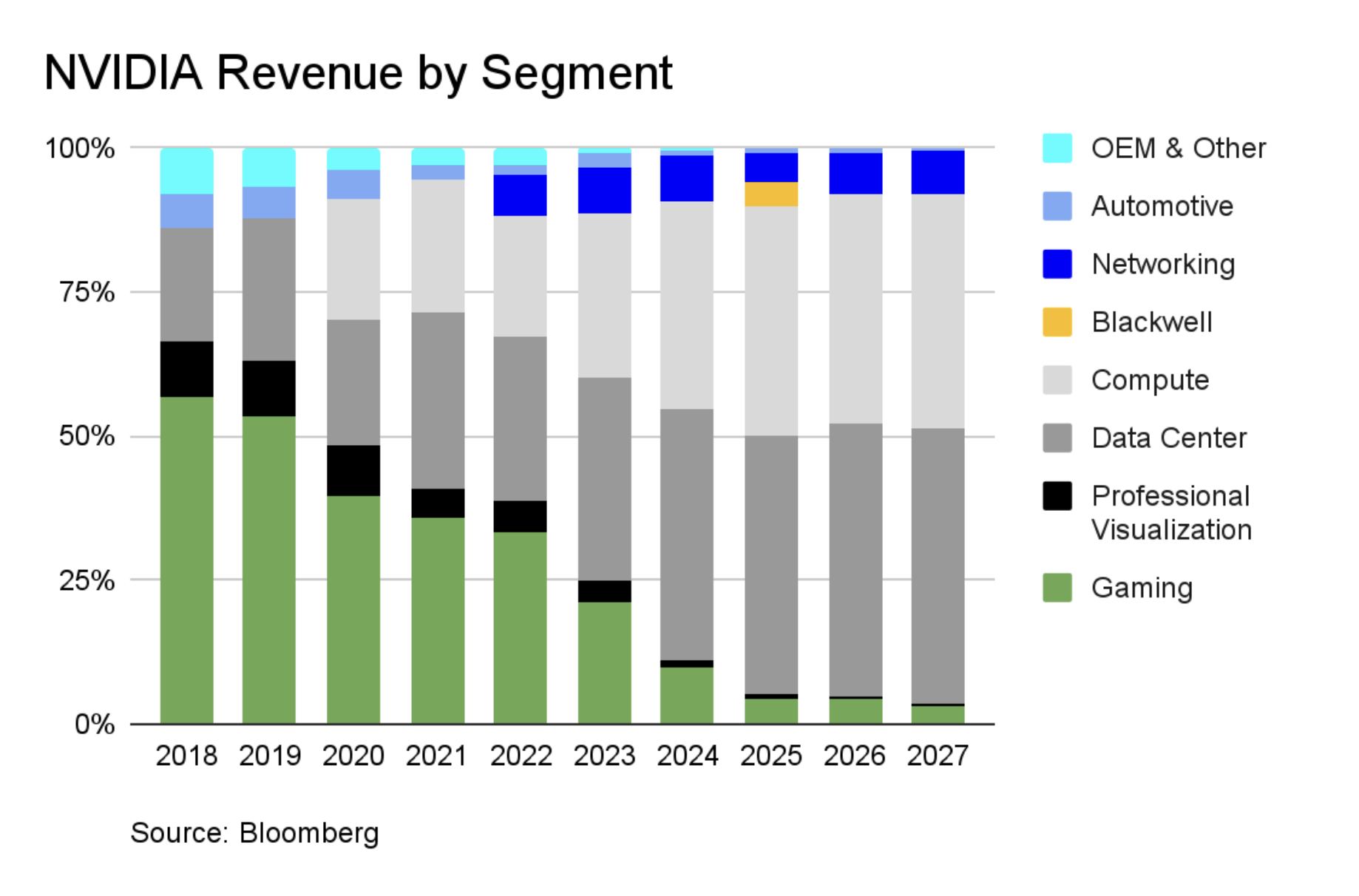

Because the story around Nvidia isn’t just about demand—it’s about capacity. As the following chart illustrates, AI-infrastructure segments now make up the vast majority of Nvidia’s business, underscoring how deeply tied its growth is to the pace of global data-center expansion (as mentioned back in January).

As AI infrastructure spending soars, bottlenecks have shifted from financing and chip supply to the physical realities of building and powering data centers. Even as Nvidia and its ecosystem partners tout backlogs, the challenge is increasingly one of logistics, power, and time.

That’s why many investors took note when CoreWeave, a Nvidia-backed AI infrastructure partner, recently highlighted the growing strain in scaling data center capacity. Despite describing “insatiable” demand, CoreWeave had to trim near-term spending because its construction and power partners couldn’t scale fast enough.

This context matters for Nvidia, not because demand is fading, but because the company’s long-term growth depends on how quickly its customers can deploy the hardware they’ve already ordered.

Jobs and the Fed

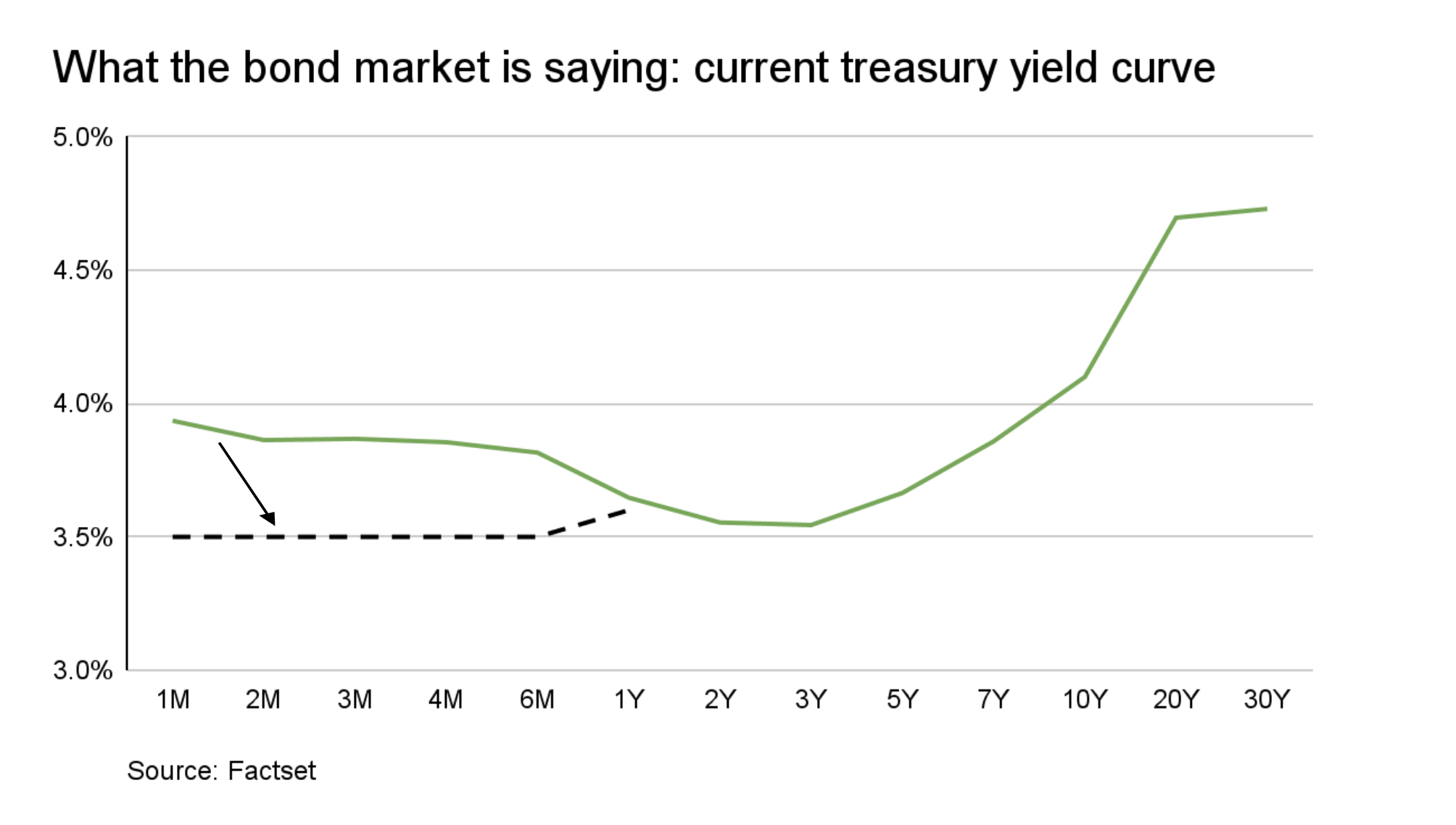

Now in addition to all that, we got a stronger than expected September jobs report pushing the expectation of additional Fed cuts further out in time. The market’s probability of a Fed rate cut in December fell from 40% 2 days ago to 20% today. That’s typically not welcome by markets.

I still think we’ll get two cuts, based on what the current bond market is saying. Fed funds would have to come down by 0.5% to normalize the interest rate curve, but it could take longer.

So what do we think now? We think we’re in a somewhat typical correction, until sentiment and expectations have fallen enough to look like there’s some value. This is at the broad market level though. At the stock level, there are still opportunities. Notably, parts of the consumer sector have already started to show signs of strength from low expectations.

In the meantime, keep dancing. At least it’s Friday, after all.

Looking ahead, Investor’s Guild will take a break next week in light of the holiday and shorter market week. We wish you a wonderful Thanksgiving—we are thankful for you, our customers.