Is something wrong? Fed liquidity watch

Is something wrong? Fed liquidity watch

With last week’s Fed meeting and earnings reports dominating, I’ve seen only a few references to something unfolding in the background — short-term funding in the banking system.

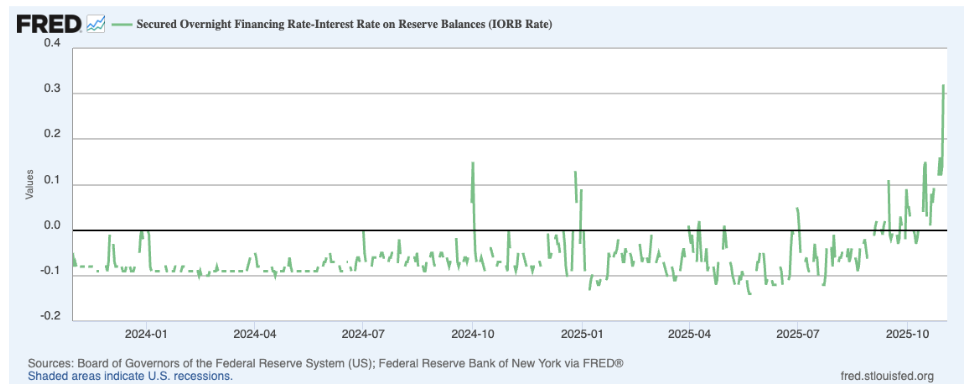

First this chart:

What it is: The difference, or spread between the Secured Overnight Financing Rate (SOFR) and the interest rate on reserve balances (IORB). SOFR — the key benchmark for overnight borrowing backed by Treasuries — increased by 0.18% on October 31 to 4.22%. It may seem like a small move but it was the largest one-day increase since 2023. That made the spread between SOFR and IORB more than 0.30%, the widest spread since SOFR started in 2021.

Why it matters: SOFR measures the cost of secured overnight borrowing — where cash is lent to banks in exchange for Treasuries held by banks as collateral. IORB is the rate of interest on balances maintained by or on behalf of eligible institutions (banks) in master accounts at Federal Reserve Banks – simply parking funds at the Fed.

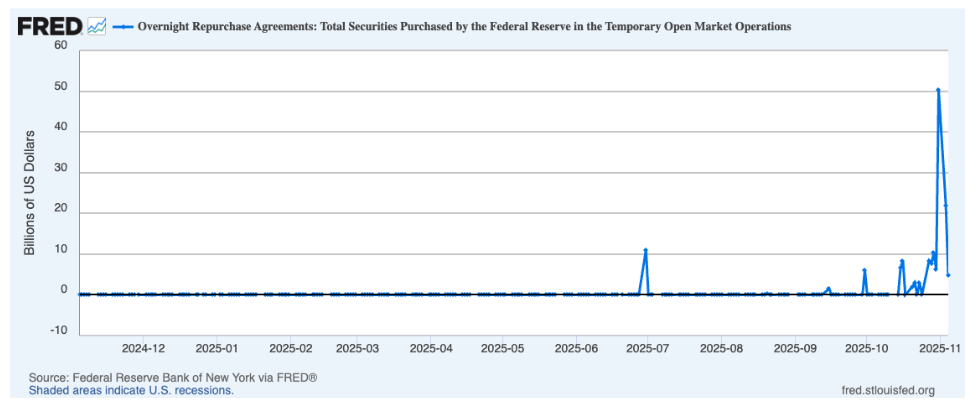

That “spread” can signal shifts in the liquidity in the banking system: When SOFR trades above IORB, it indicates that collateralized cash is in short supply, a sign that liquidity is tightening. And this chart:

What it is: The total purchases of treasuries by the Fed in Repurchase transactions or “repos,” spiked on October 31 to the highest levels since 2020. These operations are designed to temporarily add or drain reserves available to the banking system and influence day-to-day trading in the federal funds market.

Why is this happening? Is it ominous or a function of timing? Our view is it’s less ominous and more a function of timing, changes at the Fed and the impact the government shutdown is having on liquidity. And we believe people like to more readily assume that’s where any issues will start because the last big recession was there.

Banks buy treasuries, which takes cash from banks at the time of purchase. Banks also hold our cash and when we get paid, they get more. When we use it on something (spending, taxes) it drains the system.

These rates tend to spike at the end of the month, quarter, or year, as primary dealers—mostly large banks—withdraw from acting as middlemen in repo transactions on these reporting dates.

October 31 was the end of the year for Canadian banks. Canadian banks are lenders in the US repo market, so similar to the above, they don’t get involved to have a cleaner snapshot of balance sheets.

The Treasury has been aggressively issuing bills to build its cash balance after the US debt ceiling was lifted over the summer. The increased bill issuance increased the need for repo financing (done by banks) to absorb all those Treasuries in the market.

The government shutdown means there are less paychecks coming into bank accounts.

And quantitative easing (QT) is ending, but hasn’t yet, which also matters.

The Fed’s decision to end QT is a response to these pressures. With the Fed no longer reducing its balance sheet, and instead reinvesting proceeds from maturing bonds into short-term Treasury bills, it is trying to prevent further strain in funding markets. Those reinvestments — estimated around $15 billion per month — should help reduce the net supply of T-bills to private investors, easing some of the upward pressure on repo rates. But this doesn’t start until December 1.

Back in our March 2025 Investor’s Guild post, we explained how balance sheet reduction and Treasury issuance can drain liquidity and drive up short-term borrowing costs. Those same dynamics are back in focus now, even as the Fed steps away from QT.

Even with QT winding down and the shutdown likely to end at some point, the Fed’s reverse repo facility — a key measure of excess cash in the system — is low. For investors, this means short-term rates may remain elevated and volatile because the SOFR benchmark underpins a wide range of borrowing costs — from floating-rate corporate loans to adjustable-rate mortgages — so fluctuations can impact broader credit conditions.

We don’t think it’s a screaming issue right now — and one that the Fed is very aware of (September 2019 conditions were way more exacerbated). The Fed’s end to QT should help steady things but it’s always worth watching.