Can Europe stay on this roll?

Can Europe stay on this roll?

For years, the U.S. has been the driving force behind global equity markets. So-called U.S. exceptionalism meant there was no great reason to consider investing anywhere else. But the tide may be shifting. International stocks have been taking the lead lately, with Europe being one of the regions at the forefront. In fact, the Eurostoxx 50 Index is up 12.5% since the start of the year as compared to the S&P 500 at -4.5%.

The big question is whether this momentum is sustainable or temporary.

Why is the European market back in the mix?

While Europe has long struggled to gain economic traction (last year’s real GDP growth was only 0.9%), a potential change in fiscal policy may start to turn that around:

Germany recently reached a tentative agreement to expand defense spending (thanks to shifts in similar spending in the U.S.), bypassing its structural deficit cap of 0.35% of GDP. By exempting defense spending, the country now has room to ramp up investments.

Germany also proposed allocating $550 billion to upgrade its aging infrastructure, with plans to modernize roads, railways, and public services. If this spending materializes, it could provide a much needed boost to capex—a previous drag on growth.

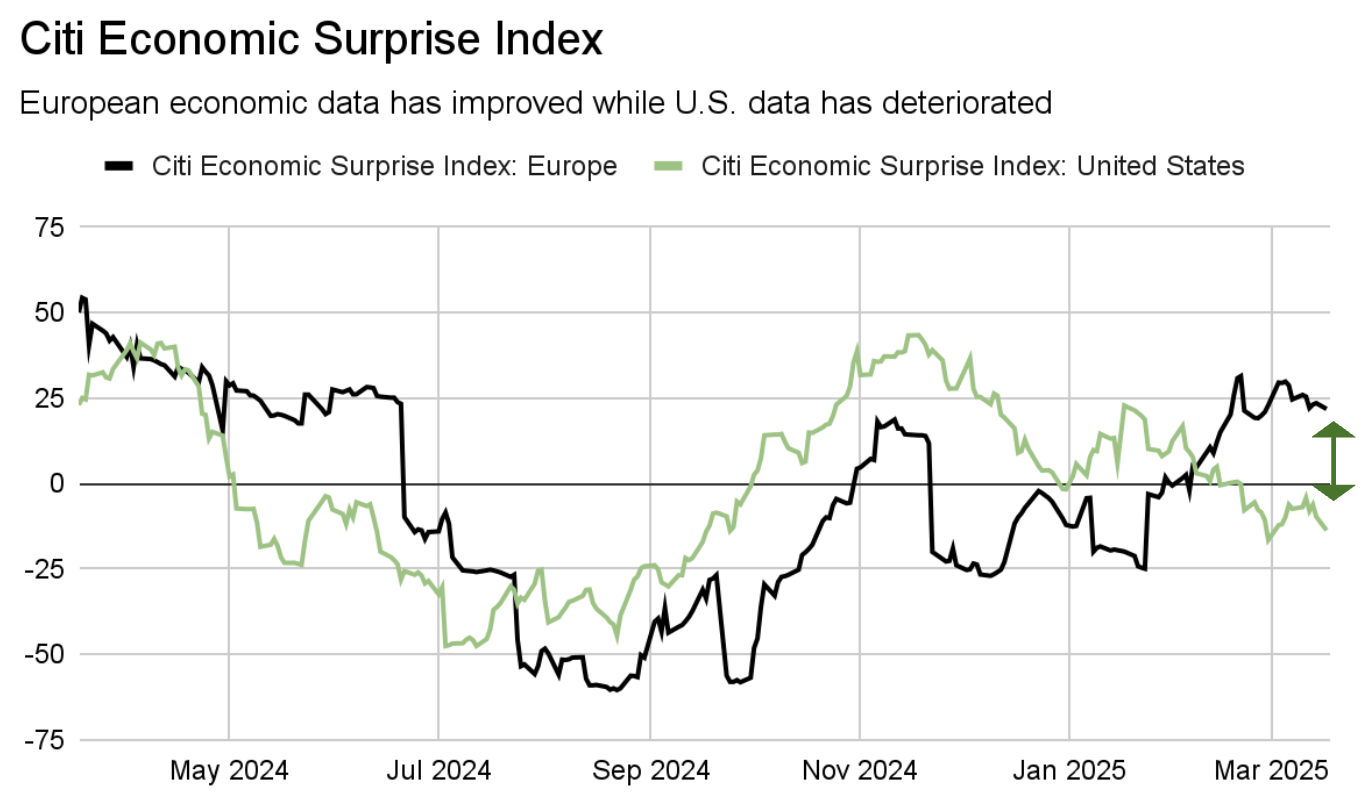

Alongside this, Europe’s economic data has been surprising to the upside. The Citi Economic Surprise Index, which measures how actual economic data compares to market expectations, has shown positive readings in Europe. In contrast, U.S. data has been underwhelming, reflecting signs of economic deterioration—or at least sentiment.

Another advantage for Europe recently is their flexibility to cut interest rates. European inflation is around 2.4%—just 0.4% above the European Central Bank’s (ECB) 2.0% target. This level gives the ECB room to cut rates more than the Fed. So far, the ECB has already delivered 1.5% of rate cuts, to 2.5%. Meanwhile, the Fed has eased by 1%, but is still at around 4.5%.

Markets expect the ECB to lower rates further to 2.0%, by August, while the year-end Fed funds rate is expected to be 3.8%—still 1.8% higher than the Eurozone. This policy divergence could continue to support European assets, as lower rates loosen borrowing conditions and make European equities valuations more attractive on a relative basis.

Though, much of the rally this year has been fueled by valuation expansion rather than earnings growth.

Europe’s valuation story

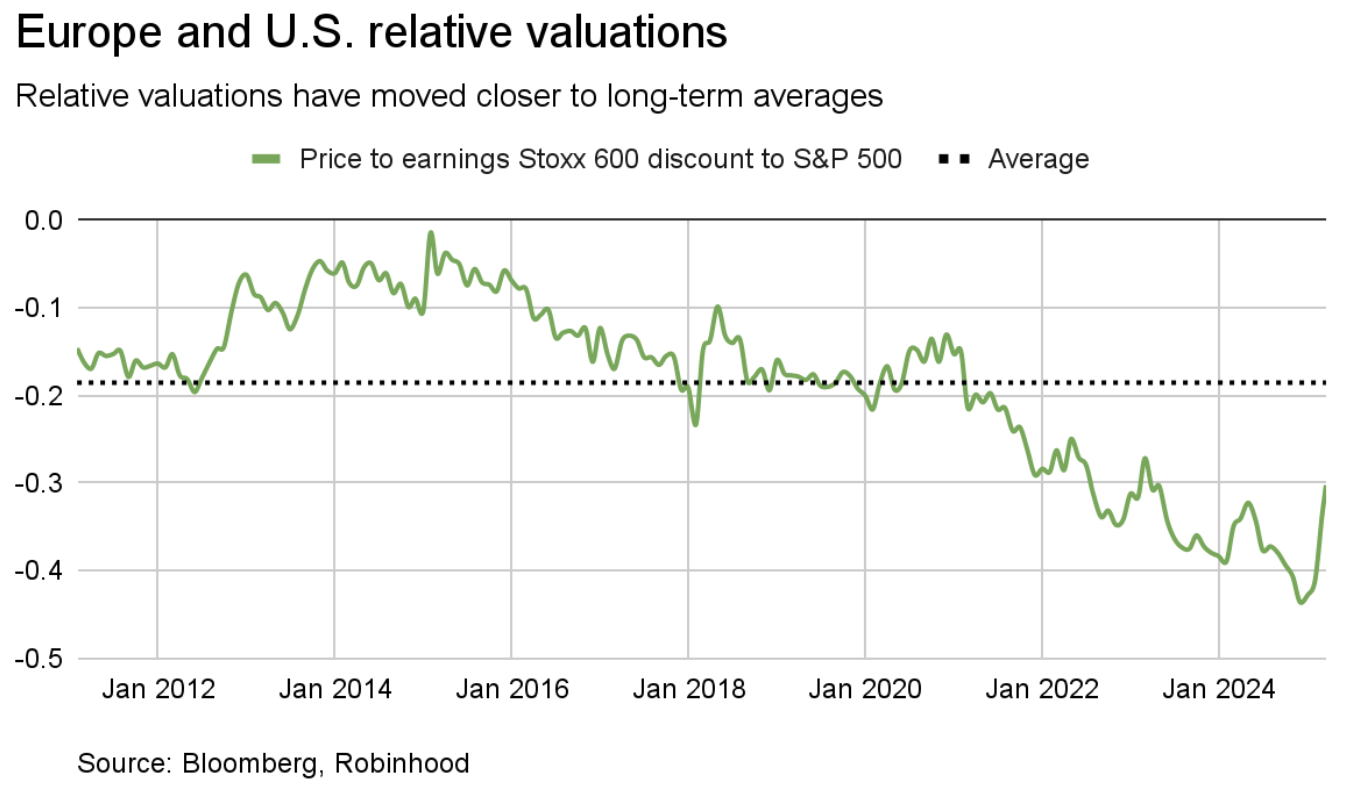

Historically, European stocks trade at a discount to U.S. stocks (as you can see the average is negative), in part due to sector composition. This is because the U.S. market is more tech-heavy, while European indices lean toward banks and industrials, which traditionally command lower valuations.

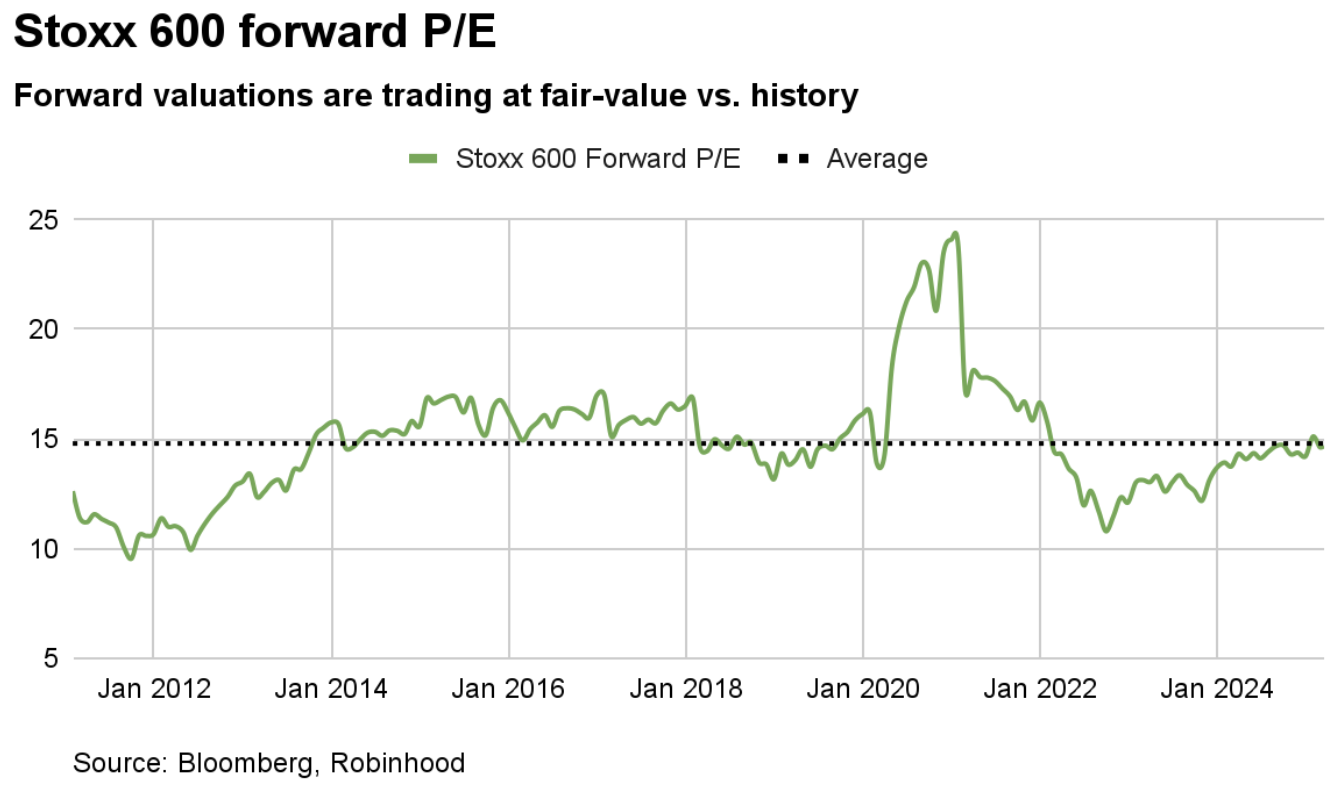

Since COVID, this valuation gap widened significantly, largely driven by the outperformance of U.S. tech stocks, especially the "Magnificent 7." More recently, as shown in the chart above, this valuation discount has narrowed. The key question now is: Can this continue? It certainly looks like there is more room for them to narrow further. But relative to its own 15-year history, European equities are fairly valued, suggesting that the next wave of gains may not be as strong as what we’ve already experienced.

Earnings expectations are modest with the weighted average of STOXX 600 companies projected to grow earnings by 8% this year— lower than the 11% expected for the S&P 500. The question is whether Europe can beat their lower expectations and whether U.S. companies can beat their high ones.

Nonetheless, risks remain that could weigh on earnings:

One of the biggest concerns is weak household consumption. Concerns over geopolitical tension and trade disputes may be keeping them cautious. A subdued consumer limits the potential for a strong, sustained recovery in domestic demand.

European corporate revenue is heavily reliant on foreign consumers. In 2023, roughly 60% of the revenue* for European companies came from outside the region, making their growth increasingly tied to external demand.

In the short term, we think European equities still have room to outperform. However, given its market strength has largely depended on fiscal policy and interest rate differentials, for the rally to last, consumer spending, business investment, and earnings growth need to pick up. We’ll be watching for that.