Timing: quarterly or semi-annual earnings

Timing: quarterly or semi-annual earnings

Timing is everything.

Ok actually expectations are everything, but timing is up there. Like Alanis Morisette sings “traffic jam, when you’re already late” and “a free ride, when you already paid.” Some things just don’t line up for us.

And now, for markets, the timing of earnings season itself is back in debate as President Trump posted on social media that companies “should no longer be forced to report on a quarterly basis.”

Quarterly earnings, or earnings season,is part of the rhythm of US markets. Should public companies only have to report every 6 months instead of every 3?

First some historical context—how did quarterly reporting start?

Quarterly reporting in the US traces its roots back to the Great Depression. After the 1929 crash, Congress passed the Securities Acts of 1933 and 1934, creating the SEC and mandating more transparent financial disclosures. Initially, annual and semi-annual reports were more common.

By the 1970s, the SEC began requiring public companies to file Form 10-Q — standardized, unaudited quarterly financial statements—to provide moretransparent information to investors.

This rhythm of reporting has morphed into a market ritual. Analysts, media, and investors comb through details to assess whether companies “beat” or “missed” quarterly estimates from across Wall Street — cementing the earnings season we know today.

So back to the question: Is quarterly too frequent?

On one hand, the focus on quarterly numbers may incentivize short-termism — prioritizing quick wins and potentially scaling back capex projects that would hurt near-term earnings, even if those projects could pay off later.

Less frequent filing could also cut compliance and audit costs (especially for smaller companies), which we believe has contributed to the drop in public companies over time. JPMorgan’s Jamie Dimon has argued this in each of his annual letters the last few years. This is from 2025:

The number of public companies has gone from 7,300 in 1996 to 4,000 today – it should be 15,000 today. This situation is the result, I believe, of a combination of factors: costly regulation and listing requirements; litigation; frivolous shareholder meetings; interference by non-governmental organizations; irresponsible, not-shareholder-friendly and misguided proxy advisors; lack of research for smaller companies; and cookie-cutter compliance requirements for boards, among others.

Similarly, in 2016 Blackrock’s Larry Fink encouraged companies to stop reporting quarterly EPS guidance:

Over time, as companies do a better job laying out their long-term growth frameworks, the need diminishes for quarterly EPS guidance, and we would urge companies to move away from providing it. Today’s culture of quarterly earnings hysteria is totally contrary to the long-term approach we need. To be clear, we do believe companies should still report quarterly results — “long-termism” should not be a substitute for transparency — but CEOs should be more focused in these reports on demonstrating progress against their strategic plans than a one-penny deviation from their EPS targets or analyst consensus estimates.

Supporters say quarterly earnings updates boost transparency, improves confidence for investors, and lowers the cost of capital for the companies, which can ultimately support investment.

With less frequent updates, many investors would experience “information asymmetry”—meaning they have a more limited sense of how a business is performing, vs. say internal employees, managers, and executives do.

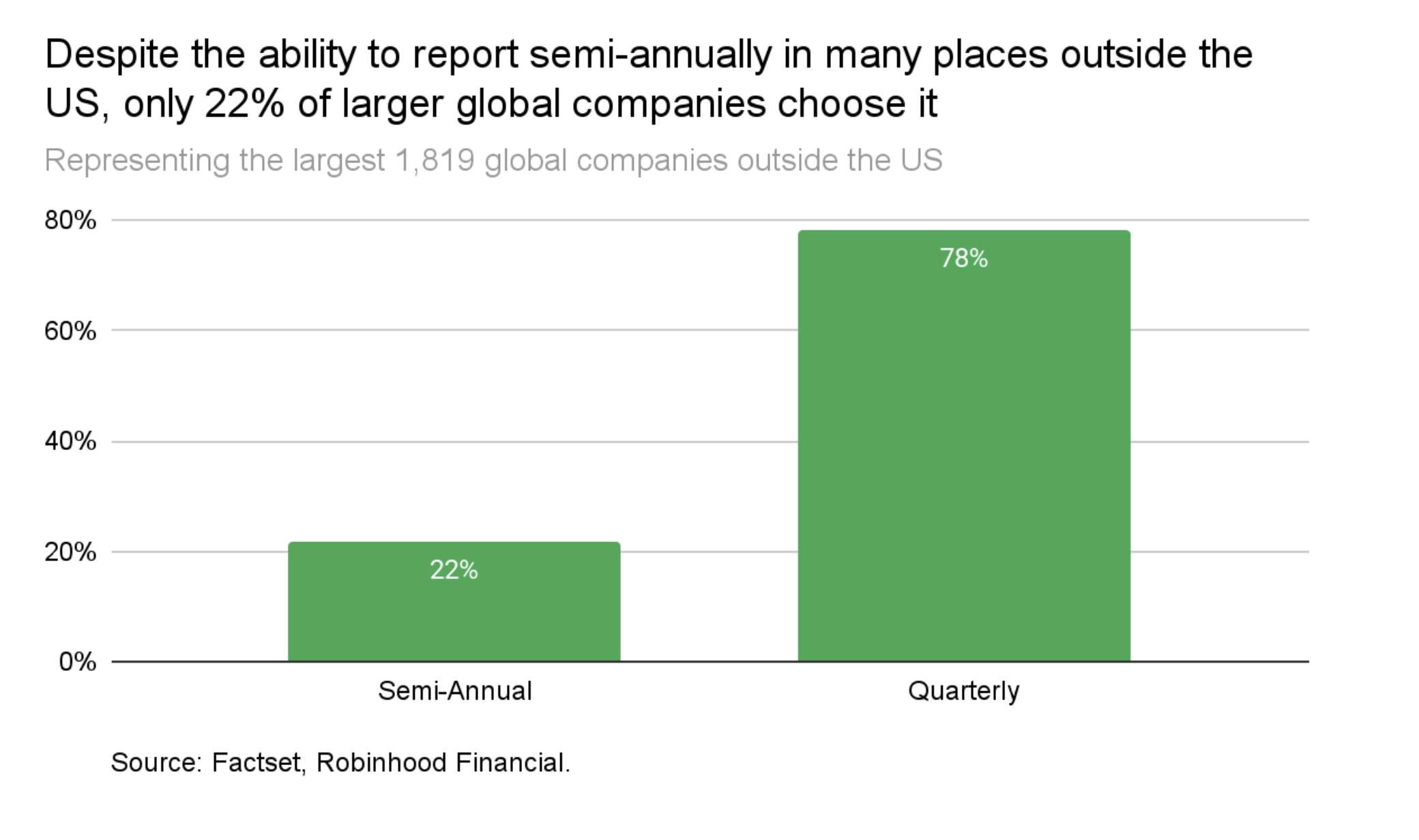

Outside the US: less-than-quarterly reporting has already been put in place. In Europe, companies have the ability to report on a semi-annual basis.

In the UK, companies moved to quarterly reporting in 2007, then in 2014 returned to semiannual, offering a quasi-natural experiment. According to a 2017 CFA Institute research piece, Impact of Reporting Frequency on UK Public Companies:

Evidence shows that when quarterly reporting was mandated (2007–2014), analyst coverage increased and forecast accuracy improved.

When quarterly reporting became optional again, many companies maintained quarterly disclosures voluntarily—but smaller firms were more likely to drop back to semiannual (due to the higher cost of reporting). Those that did tended to see reduced analyst coverage.

Yet during that time, the shift to quarterly reporting vs. semi-annual had no material impact on corporate investment levels (capex, R&D, property) for public firms.

Our take: There’s no one-size-fits-all answer. But, we think a hybrid approach—sem-iannual formal reporting paired with lighter quarterly updates of key metrics—could balance the best of both worlds.

The thing about timing is, it’s not always clear in the moment whether it was right or wrong. Sometimes later you realize it was actually the right timing—you just didn’t have all the information. Or as Alanis sings: “life has a funny, funny way of helping you out.”