The cockroach theory: hidden risks in loans?

The cockroach theory: hidden risks in loans?

I remember moving into a new house with my family as a kid and, not long after, moving out for a weekend. By then, several cockroaches had appeared. After the first one, we tried home remedies, but eventually, we had to resort to a more severe (and less convenient) approach to eradicating our home of Blattaria. That’s Latin for “an insect that shuns the light.” Fittingly, during a discussion regarding a loss from a bad loan, JPMorgan’s CEO, Jamie Dimon called the situation a “cockroach.” Similar to the insect, bad loans tend to flee from the light; at first you might see one or two—but rarely does it stop there (as many NYC apartment dwellers can attest).

It started with Tricolor—a Texas-based auto lender specializing in loans to borrowers with weak to no credit scores—which went bankrupt in September amid suspicions of fraud. The company funded those loans by borrowing from banks and packaging the loans into bonds sold to investors. The thing is, at the time of bankruptcy, the company went straight into liquidation—an unusually abrupt end for a lender of its size—after one of its banking partners, Fifth Third, reported a $200 million loss tied to alleged fraud in Tricolor’s financing lines. Turns out the people running it had a shady past.

Then First Brands, an auto parts supplier, filed for bankruptcy, disclosing more than $10 billion in liabilities in the same month. Auditors uncovered a $2.3 billion shortfall in what were supposed to be customer payments—money that had, in their words, “simply vanished.” Investigators are examining whether the company borrowed multiple times against the same invoices, effectively reusing the same collateral to get more cash. A criminal probe is now underway.

A few more have happened since, also auto related,though not all fraud related. CarMax, for instance, had to significantly increase its provision for loan losses to $142 million this quarter, a jump of nearly 40% from the previous quarter.

Banks large and small have been reporting earnings over the last few days with many of them increasing their provisions for losses as well. For example, Zion’s Bank is charging off $50 million of loans in the construction space where it found "apparent misrepresentations and contractual defaults". Western Alliance Bank is also suing a borrower due to allegations of fraud on a loan they provided.

So, is the timing coincidental or is there more to it? Well, easy money likely lightened due diligence.

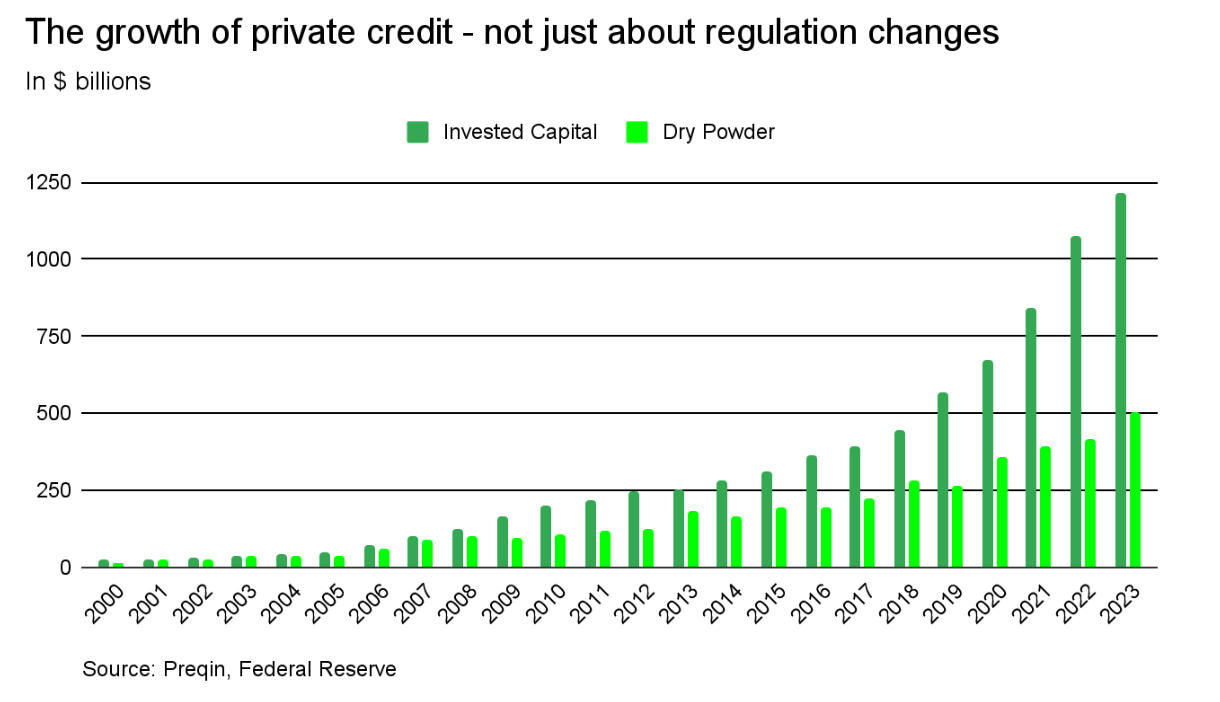

Private credit has quietly become one of the most powerful forces in global finance.

A decade ago, if a midsize company wanted to borrow money, it went to a bank or issued bonds. But thanks to changes in regulations post the Global Financial Crisis of 2008, a good portion of that business was taken away from banks. Today, that same company might turn instead to a private credit fund—a pool of money run by investment firms, not banks, that lends directly to companies. For borrowers, private credit is fast and flexible. For investors, it offers higher yields than traditional bonds. And for regulators, it sits largely outside their reach.

And that mix has fueled extraordinary growth. Since 2010, the private credit market has exploded from a niche financing tool into a $1 trillion+ industry. The money comes from pension funds, insurers, and wealthy individuals seeking steady higher income.

This created more competition for loan investments and seemingly unlimited capital waiting to invest. Historically, the more money flows into something, the looser standards can get. In both Tricolor and First Brands, key checks broke down:

Auditors and bankers didn’t fully trace the collateral behind the loans.

Investors took financial statements at face value, assuming internal controls were solid.

Competitive pressure favored speed—close the deal first, verify later.

These aren’t signs of systemic fraud everywhere—but they’re reminders that when everyone chases yield, due diligence can become an afterthought.

So where else could this go?

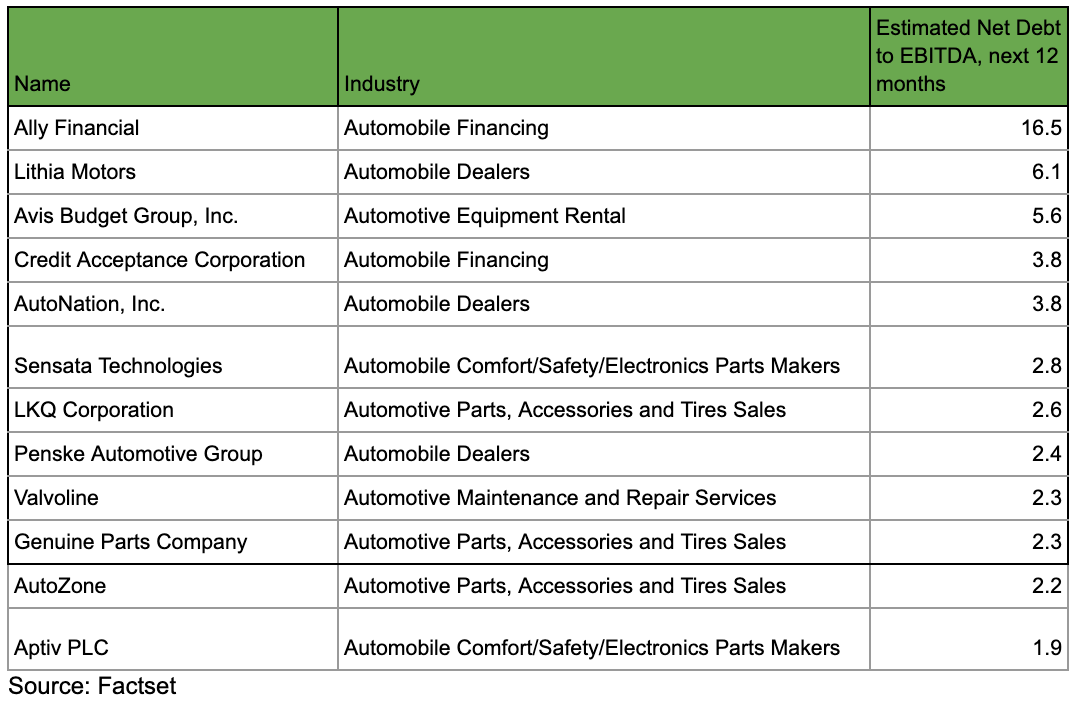

The combination of high vehicle prices during COVID (driven by supply constraints), higher post-pandemic interest rates, and general economic pressures on consumers, has led to rising delinquencies in the auto sector. Out of the largest 1,000 US companies, those in the auto and auto-related sectors show the following data in terms of debt to operational earnings (EBITDA or earnings before interest, taxes, depreciation and amortization):

So far, the fallout looks containable. According to the Federal Reserve Bank of New York, there’s over $13Tr in housing debt and $5Tr in non-housing debt. Auto loans now stand at $1.66Tr, where delinquencies greater than 90 days are only about 5%. Student loan and credit card delinquencies are actually rising at a faster clip.

Still, it raises a bigger question: How much risk is hiding in corners we can’t yet see? It’s why I prefer keeping a little dry powder on hand right now.

Because the lights are on now—and investors are watching for movement.