Why tariffs at all?

Why tariffs at all?

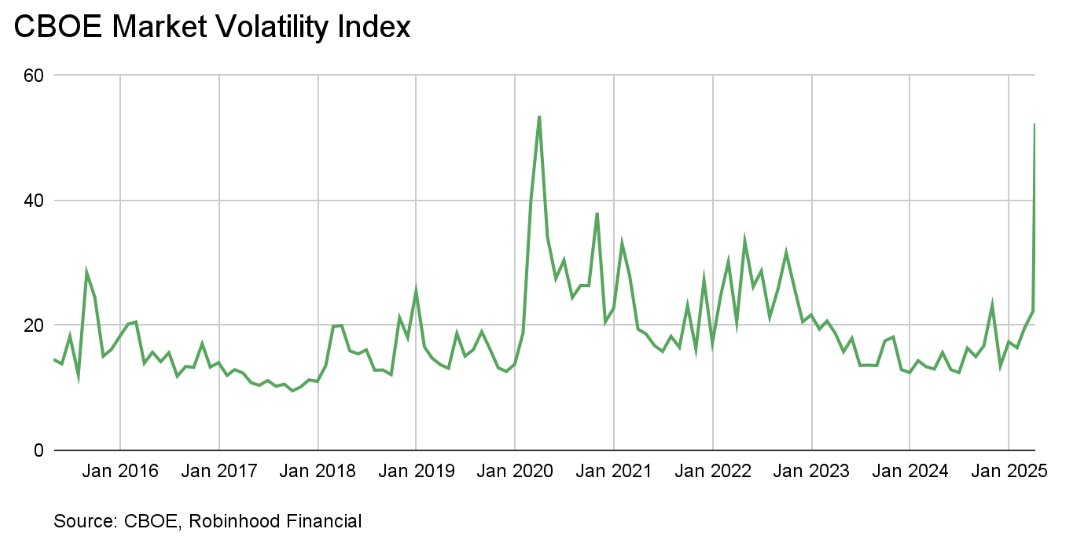

It’s been a fun week for investors navigating heightened volatility levels (check out the CBOE Market Volatility Index below), as a result of announcements of tariffs the US has and could place against many countries.

The economic impact is bad for all of us when you consider the potential higher prices and slower growth.

But one of the stated motivations behind the tariffs isn’t unfounded: "The only reason we’re in this mess is because past leaders sold us out. They let other countries take advantage of us with terrible trade deals and no tariffs. I’m just trying to fix it."

Despite the downside, let’s consider that statement.

Over the last 40 years, revenue and margin expansion contributed equally to strong corporate earnings growth. This was because US companies could do the following:

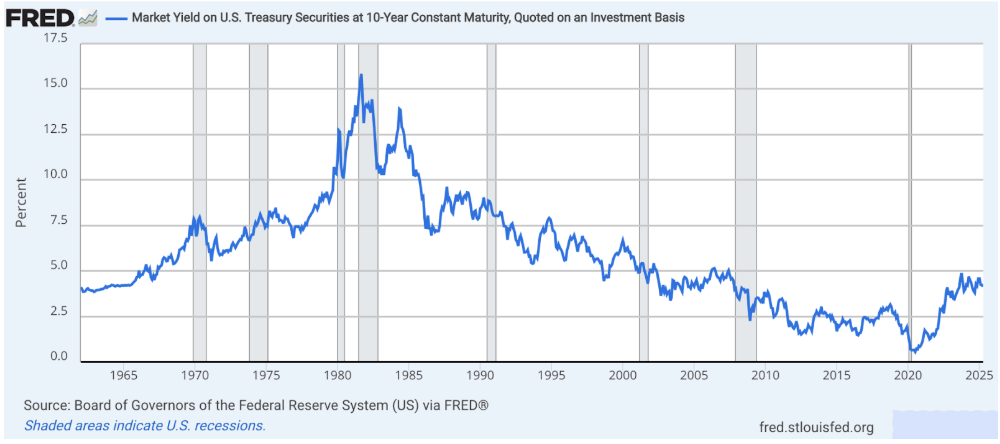

Access capital (aka borrow) more cheaply over time. Inflation came down from historical heights starting in 1981and borrowing costs went with it. This was especially exacerbated by quantitative easing taken on by the Federal Reserve after 2008, which took rates down to unprecedented levels. Check out the direction of interest rates since the 1980s below.

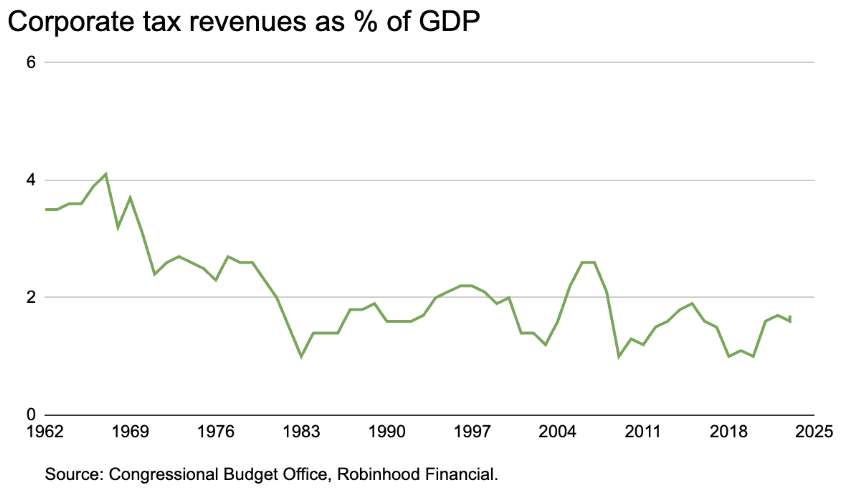

Pay less in taxes. Corporate tax rates also dropped over time, contributing less and less as a percentage or total revenue collected by the government. Below is the corporate tax collection over time—which is less than 2% of GDP. To put this in context, individual tax revenue is at 14%.

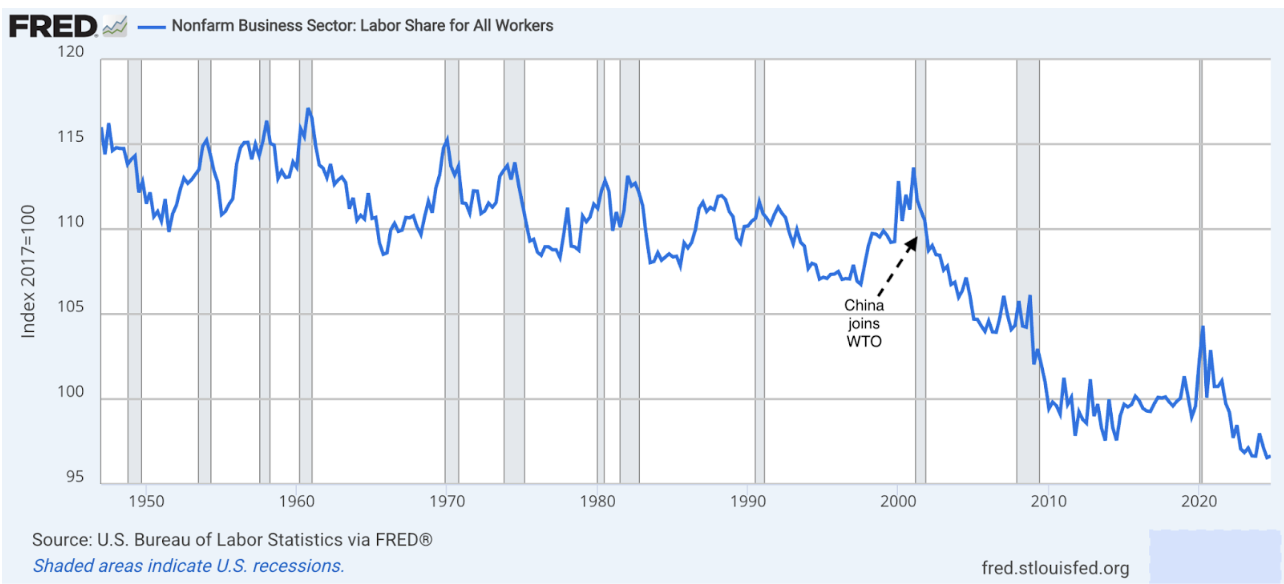

Pay less in employee wages. The labor share of output was steady for decades until a decline began around 2001.

Why?

There are a range of theories to explain this shift, including the impact of globalization, technological change, and the rise of market concentration from superstar firms (EG Mag 7).

But you could also look at another factor: diminished worker bargaining power when China joined the World Trade Organization in December 2001.

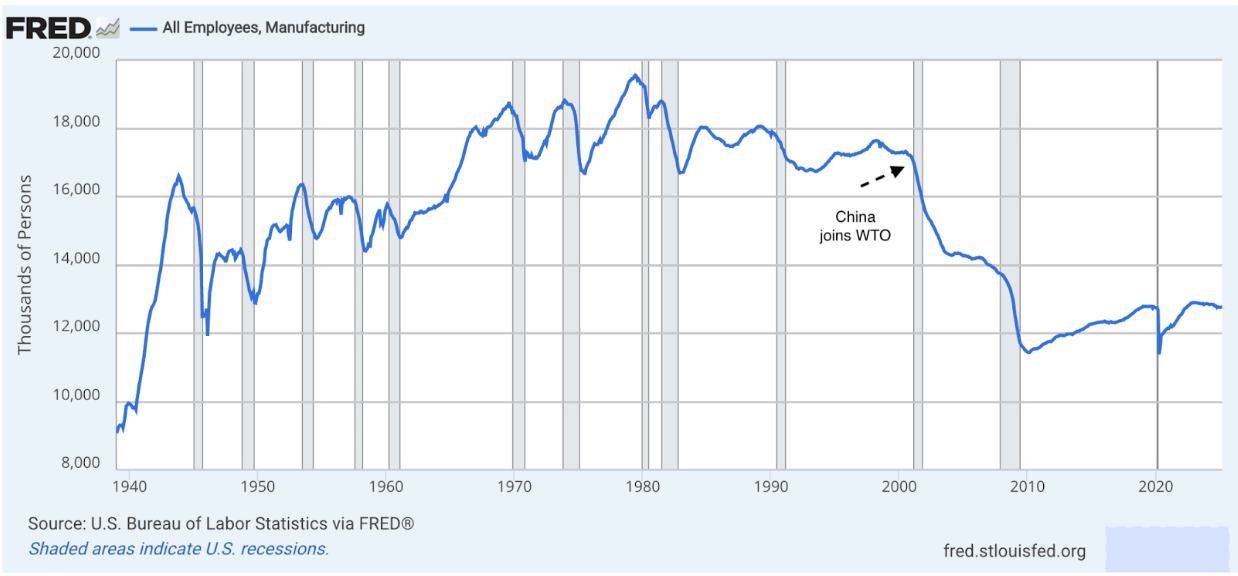

Since the 1960s, the world has seen globalization spurred by peace and profit seekers. Labor is on average 2/3rds of a company’s costs. So looking for less expensive labor to improve margins became very attractive. With a move of manufacturing out of our country and mostly into China - the world became the US corporate sector’s oyster. See the chart below of US manufacturing jobs between 1940-2021.

So while corporations took a W in this, it negatively impacted millions of families through both economic hardship and emotional strain from job displacement and insecurity.

As I stated at the start of this post, the oft-stated motivation behind the tariffs is right. But it’s hard to tell if that’s just something to say. The real motivation is just as likely to be to raise revenues to fund tax cuts in certain places (tip income, social security). Either way, the execution—whether to raise revenues or revert the economy—is so far misguided. I don’t believe it’s possible to unwind decades of the global economy and revert jobs sent offshore 24 years ago back to the US. It seems reasonable to believe that at the very least it would take longer than the 4 years that remain for the current administration. If the US and its trade partners can’t reach a lasting agreement to reduce or eliminate tariffs, the likely result would be higher consumer costs and lower growth without anything else to show for it. A better approach would be fixing social security spending, diverting more towards education, technical training, and incentivizing investment for the future industries. By establishing a new, more affordable savings system for future generations, teaching robotics and mechanical systems, investing in adaptive farming, establishing factories for things we don’t yet make or use, we could continue to grow without leaving American workers behind.

While it looks like now there is room for negotiation from the President, tariffs will cause inflation to rise and growth to fall. This will impact everyone—not just the stock market.