Japan’s rebound faces its next test: trade and the Yen

Japan’s rebound faces its next test: trade and the Yen

We became bullish on Japan’s stock market back in the Spring of 2023 (see post here). TLDR: after years of sluggish growth, deflation and negative interest rates, Japan looked like it was starting to turn a corner. Growth and inflation finally picked up and, with it, wage gains—allowing the Bank of Japan to end its long-running negative rate policy. And for the first time in a long time (like 1990), Japanese markets began entering a new paradigm. Fast forward to today, the Japanese stock market is up +34% in the last 2 years. So, now that the first leg of the recovery is behind us, things are getting more complicated.

Obviously, tariffs

Japan depends on exports. Using the MSCI Japan Index as a proxy, over 54% of revenue from Japanese companies is derived outside Japan. On a sector basis, the industrials and consumer discretionary sectors make up 40%—Toyota, Sony, Mitsubishi, etc. Both aspects make them sensitive to swings in global demand—and the cost to send goods abroad.

Despite making temporary deals with a couple of other nations, Japan has not yet made progress with the US. To recap, here is where things stand today:

The baseline tariff of 10% applies to most imports

25% sector-specific tariffs, targeting autos, auto parts, steel, and aluminum

24% "reciprocal" tariff aimed at addressing trade imbalances

These get stacked. One of the biggest losers with tariffs are Japanese auto manufacturers—facing up to a 59% tax.

Japan has pushed for a full elimination of tariffs. It’s an election year for them, so showing progress has become even more important. Right now it feels unlikely that a full removal of tariffs could happen, though more possible on a temporary basis, similar to the ones with China. Any relief—especially on autos—could provide meaningful market support.

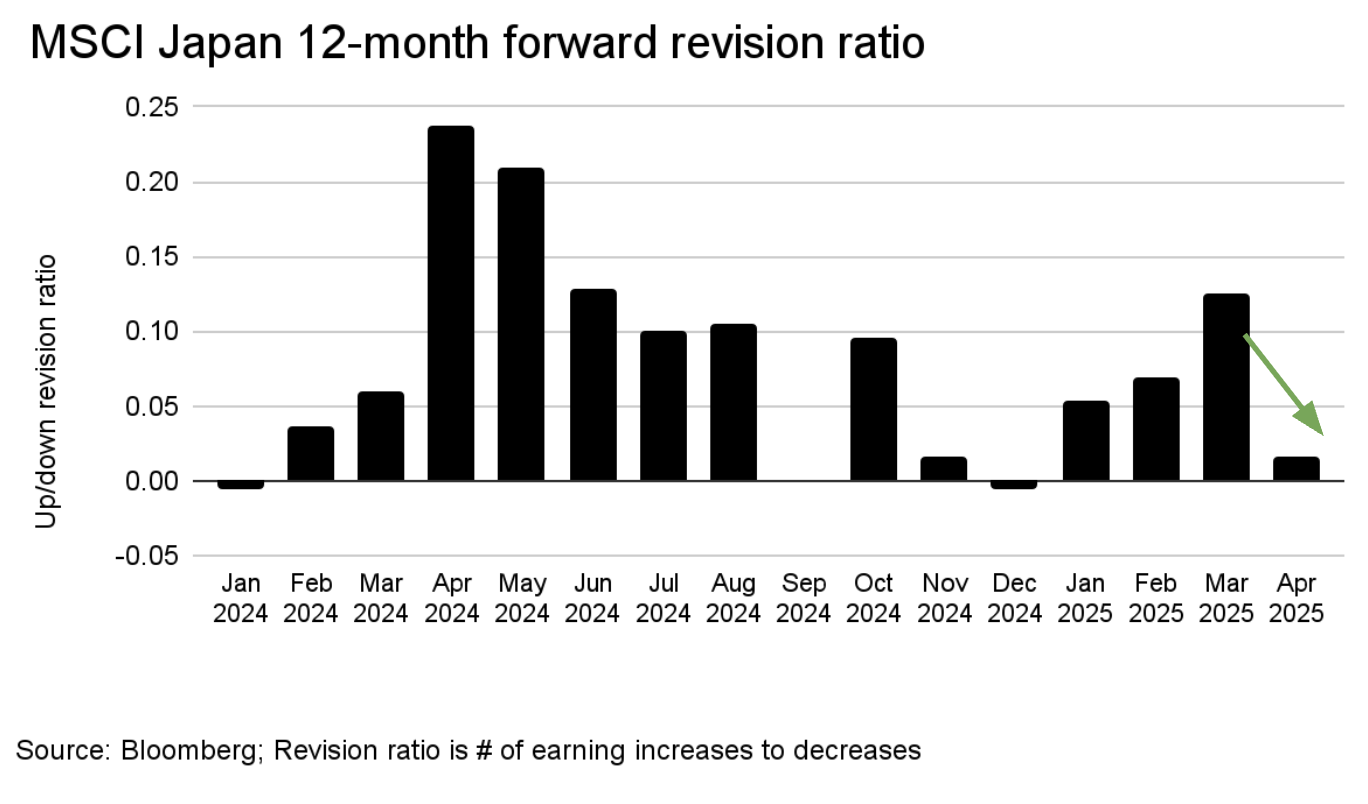

Expectations have been adjusted

The impact of tariffs is showing up in forward guidance. In recent earnings transcripts, Japanese firms cited tariffs and a stronger yen as key reasons for reduced visibility into future performance. As a result, the number of earnings estimate increases vs. decreases has dropped more than 83% from March to April—reflecting lower earnings expectations.

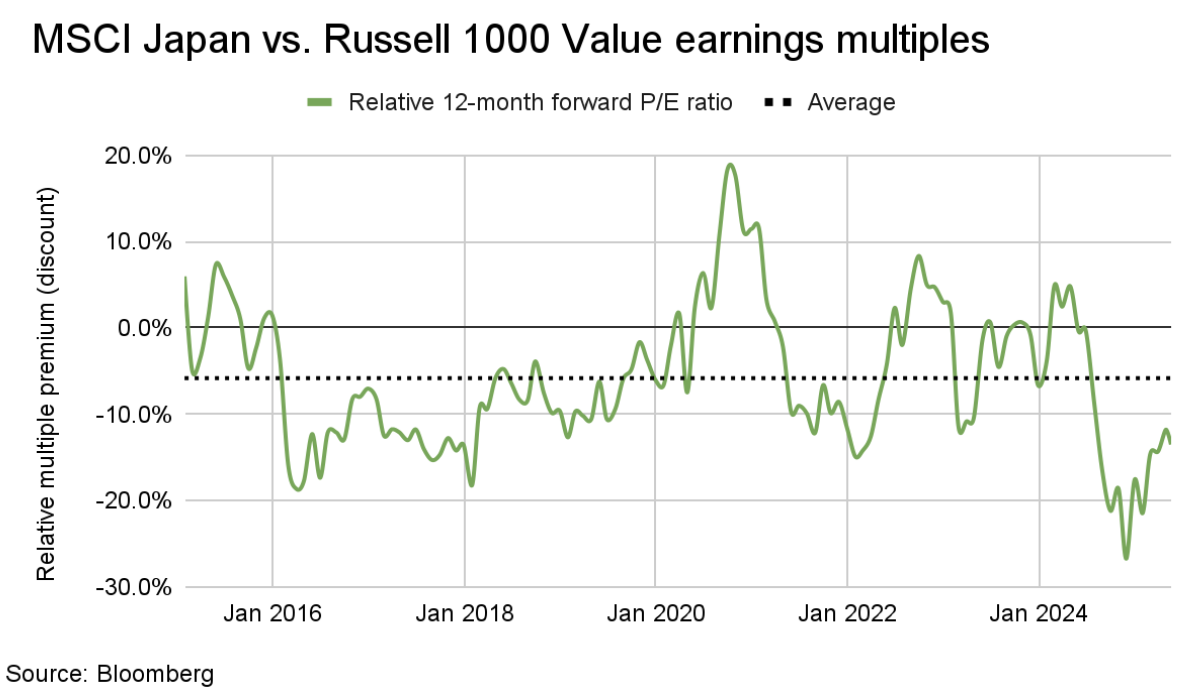

And valuations reflect this, too

Given Japan’s more value-oriented, industrial-focused nature, we compared the earnings multiple of MSCI Japan Index to a US value index: Russell 1000 Value Index. Current multiples are trading at steeper discounts than long-term averages, signaling that markets are already pricing in weaker growth expectations. Potentially too low, considering that so far, US demand has held up.

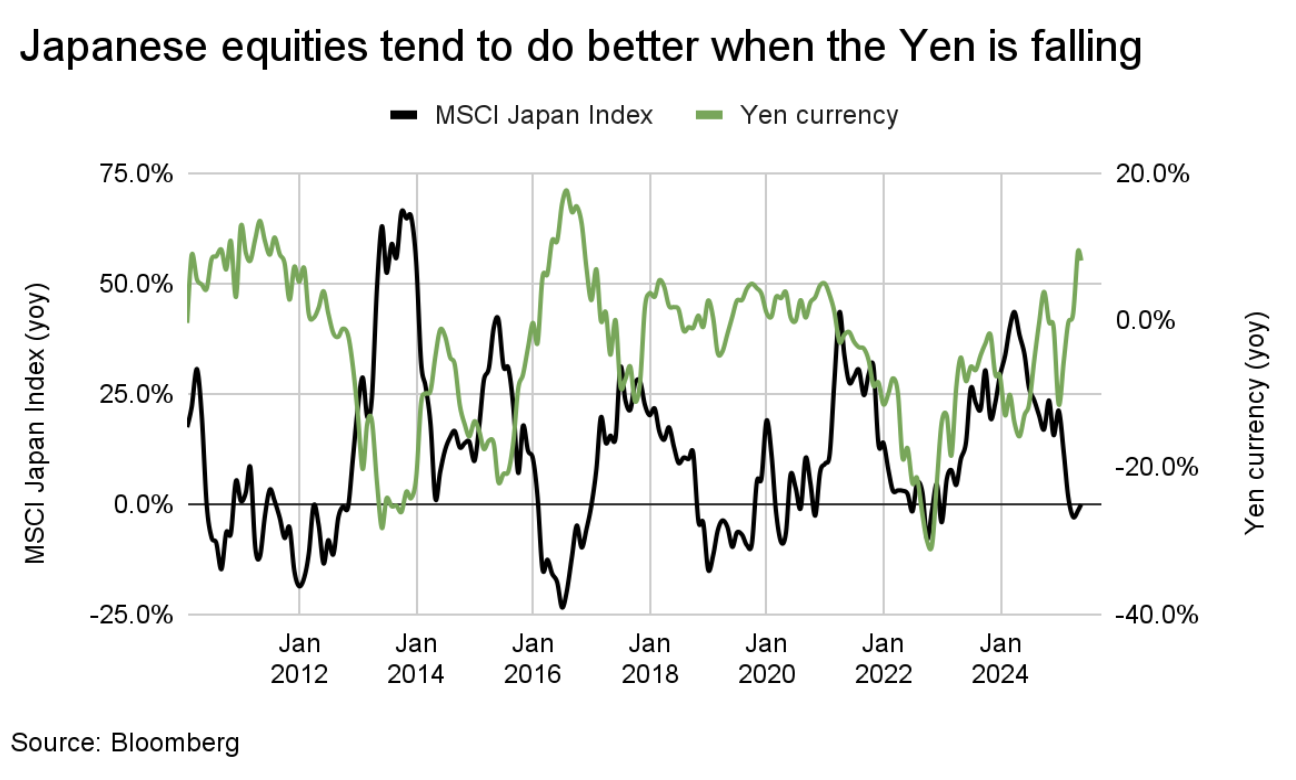

Currency also plays a critical role—both fundamentally and from a market return perspective. On the fundamental side, Japanese companies earn a large share of their revenue overseas, so a weaker yen typically benefits them when those foreign earnings are converted back into the yen.

From a market perspective, you can see from the chart above, the relationship has historically been negative. This means a stronger yen often coincided with weaker equity returns. Current dynamics are mixed on the future direction of the yen.

Trump has been vocal about wanting a weaker US dollar.

A ballooning US deficit has made some global investors question dollar dominance. However, it also means interest rates stay elevated, making it stronger. These two may offset each other.

Then there’s monetary divergence. Higher inflation in Japan could push the BOJ to hike interest rates, while in the US, markets are pricing in a 25bps cut in September—unless inflation re-accelerates. This dynamic could narrow rate differentials, strengthening the yen. This is not guaranteed, though.

All in, we believe Japan’s economic recovery remains intact while markets have already priced in many of the most negative headwinds. Clearer guidance on tariffs and a more supportive currency backdrop could help unlock the next leg of upside.