The road: a summary of macro thoughts

The road: a summary of macro thoughts

I used to listen to a lot of reggae. Bob Marley, Toots and the Maytals, Jimmy Cliff and Buju Banton played in the background of many of my Sundays in my 20s. But lately, the chorus of Buju Banton’s rendition of “It’s not an easy road” has been haunting me.

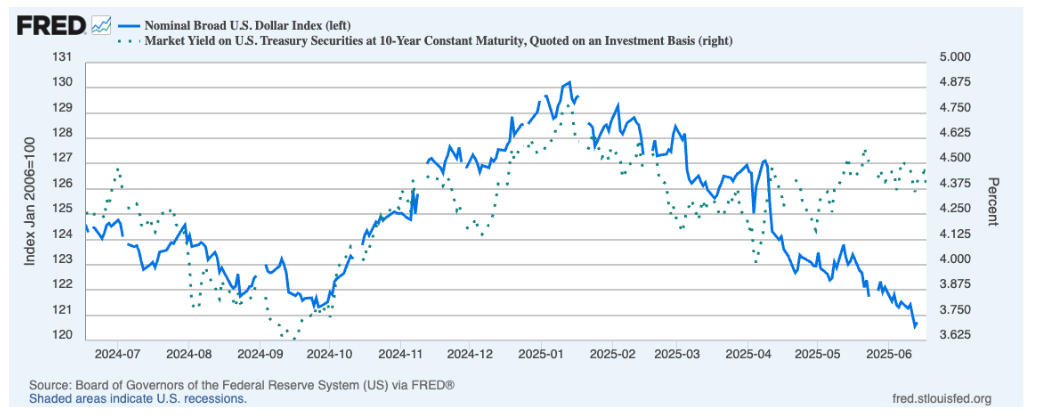

Navigating the world as an investor has not been easy this year. As humans, we all operate under a set of assumptions. For example, when rates go up, the US dollar usually goes up. Not this year.

In short, while we wait to know more, small underlying shifts are taking place.

Tensions in the Middle East are pressuring risk sentiment. While we wait for the White House to declare its next move, provide military support or pursue diplomacy, everyone speculates on the impact. Will oil move higher, or will it not matter? My view is, in the short term, this is not a core issue for US equities—there is asymmetry with the conflict and we have adequate oil supplies (unlike in the 70s). For the longer term, it could have lasting effects on freedoms in the region and how commerce moves around the world.

Trade deals (or lack thereof): they are still somewhat non-existent (except the UK). There had been hopes of deals at the G7 but President Trump left early, citing that Japan was tough and Europe hadn’t yet offered enough. July 9th is approaching (deadline for the Liberation Day pause). If we don’t have any deals by then, I think you could see a short-term reinstatement. This would be bad for risk sentiment, but I do believe the White House’s intentions are to get to deals. The levels of tariffs matter, though. As chair of the Federal Reserve Jerome Powell said on Wednesday: “Someone has to pay for tariffs, and some of it will fall on the end consumer…we need to see the extent of this before deciding on policy.”

The budget and deficit: the Senate published its part of the reconciliation bill, and the big takeaway is this legislation will require more work before hitting the President’s desk (it seems increasingly unlikely that reconciliation will be signed into law by July 4th—the stated goal). This version took away or lowered a bunch of deductions and increased Medicaid cuts. Either way we keep a big deficit. The CBO said the government has until August now until money runs out. The big question is how long can we sustain such large deficits? It’s going to make it damn hard to get rates lower—which hurts us all.

Immigration and deportations: this is a sensitive topic on many fronts. Maybe it’s just the human stories that get to me—from all the angles. But from an investor’s perspective, if our overall labor supply drops, I worry about inflation—more than any other potential inflation-causing issue. Simply put, fewer foreign-born workers could lead to a tighter labor market, which in turn puts upward pressure on wages. This sounds good for US workers, but adds another layer of cost for businesses already deciphering tariff-related input pressures in the short term.

The Fed and rates: Recently, many have speculated the Fed may begin to speak more softly about rates, meaning they will suggest rate cuts could come soon. I think this expectation was set by the recent OpEd by David Malpass where he cited one single volatile stat from the recent jobs report as evidence it is time to cut. With all my points above, I think it’s right to stick to waiting and seeing—no matter how it might help in the short term. The inflationary period in the 2021-2023 period—the first in over 50 years—was hated more than a recession has been. And as I learned early in my career, inflation is the answer to every question. The Fed needs to be sure it won’t come back. And that’s more in flux now.

Longer term, I do think inflation will come down. In fact, I believe AI will all but guarantee that. But right now, we’re “Waiting in vain,” as Bob Marley and the Wailers would sing.

Given all this, we suggest being positioned with balance between what works in inflation and slow growth (dry powder in cash, low vol stocks, some alt assets) and everything turns out ok (cyclical names).

On the bright side, there is growing CapEx which if invested wisely, fuels growth. And over time, earnings growth is what matters. So far, companies have been able to keep doing that, while expectations for earnings this year have come down from 12% to 9%. 2026 is still at 13%. There is likely too much uncertainty to make a big reduction here. But it also shows how much hope is still in the market.

I still have some too.