Freedom to invest: our UK investor survey

The value of your investments and the income you receive from them can go up and down, and you may get back less than you invest. Any examples are for illustration purposes only.

It’s not that Brits are bad savers, it’s just that we’re not great at actually putting our money to work. Our preference for cash over the stock market is a problem the government and industry regulator both want to tackle, and it’s why we launched our own survey to see what the barriers to investing really are as well as what we can all do about it.

Read more

Freedom to Invest

Some of the most interesting findings came from misconceptions around what it takes to start investing, as well as just how different we all are when it comes to having the confidence to make that first investment. First things first, though - are we really hoarding that much cash? Let’s dive in.

UK investors on the world stage: how do we compare?

When it comes to prepping for a rainy day the UK is around the middle of the pack among developed economies in holding about one-third of its financial assets in either cash or savings accounts.[1] 72% of us have saved in the past 12 months, above the OECD average of just 60%[2], so we’re not bad savers by international standards. But, we hold a much smaller percentage of our total assets in investments compared to similar western countries.

Read more

How to start investing

Are you holding too much cash?

Do I need to get every stock pick right?

This holds back returns for Britons who, according to the Investment Association (IA), could have grown £10,000 five years ago into £12,249 today if they had put their money in a typical global equity fund. Putting the same amount in a cash ISA would have eroded its value down to £8,713 in today’s money, given the impact of inflation.[3] That’s enough of a concern that the FCA itself said it plans to reduce the cohort of consumers who have £10,000 sitting in cash by 20%.

“By seeking to eliminate risk — for example, why do we have hundreds of billions of pounds in cash ISAs? — we have failed to drive an investment culture, as we see in other places, that allows people to invest their money. That is actually part of consumer protection; in a way, we have regulated so much that we are not protecting consumers against inflation.”[4]

Economic Secretary to the Treasury, Emma Reynolds

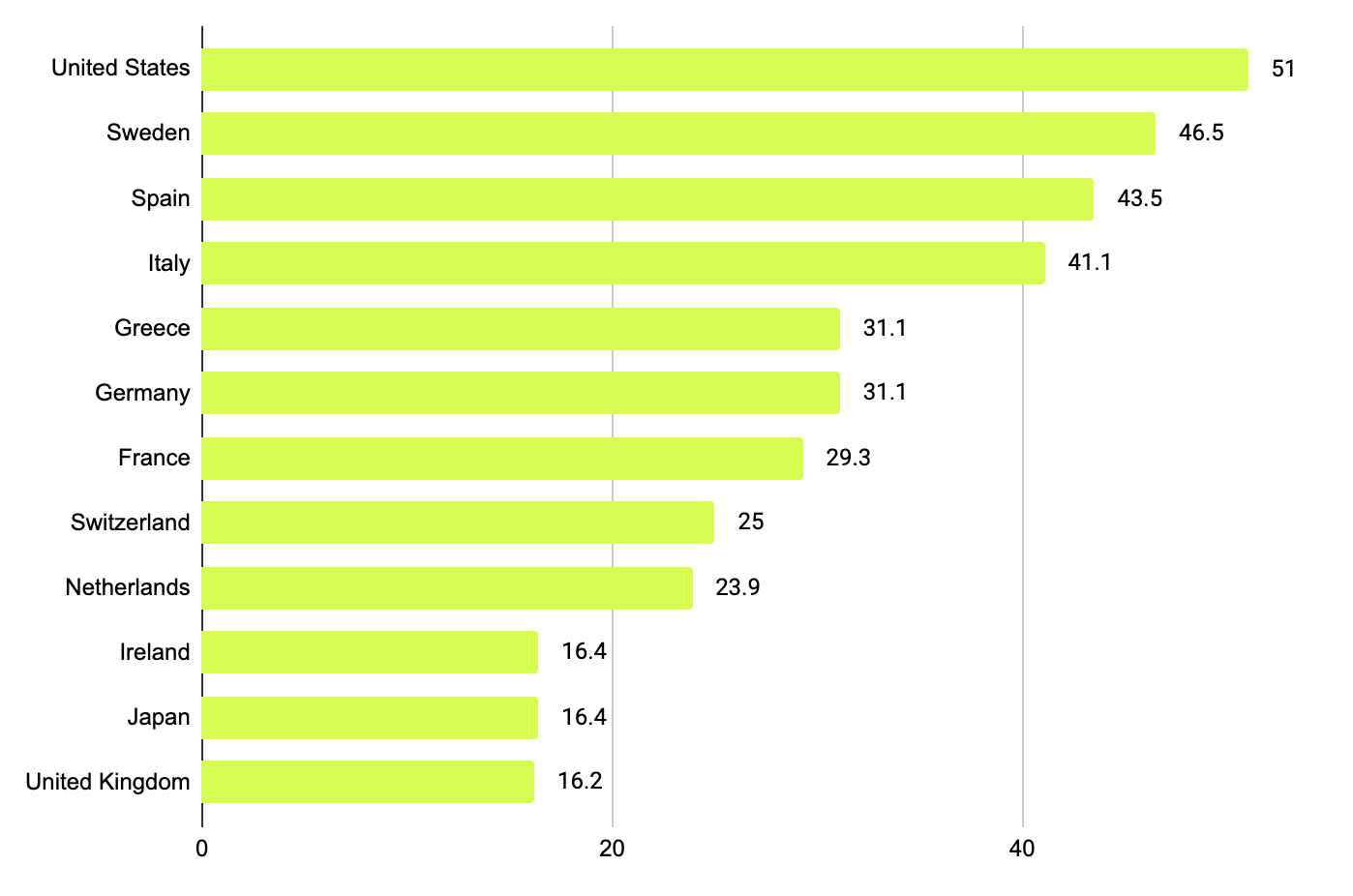

It’s maybe no surprise then that, while households in the US hold half their financial assets in equities or investment funds, that portion is just one sixth in the UK. Investing in equities and funds is also significantly more common among our European peers like France, Germany, Italy and Spain than it is in the UK.[5]

Share of household financial assets in equities and investment funds

Source: OECD, NAAG, 2022

The odd thing is that, according to an ING survey of risk attitudes across 15 countries, UK consumers understand the risk-reward trade-off inherent in investing and should be ready to invest. So, the barrier isn’t that we don’t understand the potential benefits of investing. Instead, we’re put off by something else.

What are some of the biggest barriers to getting the UK investing?

1. Cost

On average, the group we surveyed thought they would need at least £2,383 to start investing in a stocks and shares ISA.

Within under-represented groups there are significant variations in the perception of this barrier. For example, the minimum investment perceived for a stocks and shares ISA among women aged 35-54 is more than 50% higher than the perceived minimum than among women aged over 55. But it is in the minority ethnic group that this perception barrier really stands out. Potential investors from minority ethnic backgrounds assume the minimum sum to access each of the prompted investment types is significantly higher. In the case of the standard stocks and shares ISA that is held by millions of Britons, the perceived amount is 85% higher.

2. Confidence

The second most cited reason for not investing among women was not feeling confident they could make good investment decisions.

Whereas 63% of men feel confident in making their own investment decisions, only 39% of women feel the same.[6] 63% of women also said complex jargon put them off. All this despite evidence that shows women are just as knowledgeable about investment principles as men.[7]

Interestingly, we also found that confidence didn’t necessarily rise as we spoke to people with higher levels of education. If you are more exposed to statistics, complex products and awareness of behavioural biases, is it a case of realising everything you don’t know as well as what you do?

3. Risk

In our study, the single most cited reason among both men and women for not investing was considering it to be too risky. Women were significantly more likely to cite this as a reason than men. Digging into this, though, it was often the language used to talk about investment risk that was the hurdle, as it would put people off rather than offer a rounded view of what risk actually means in investing. There’s clearly work to be done here. It also links to another overarching theme throughout the survey, namely that we don’t feel educated enough around financial literacy.

Breaking down barriers starts here

There were a lot more findings in the full survey but all pointed to a general feeling of underpreparedness and detachment from where to learn about investing in an uncomplicated way.

It’s why we try to talk to our users in a way that feels helpful and accessible, and reach them through the app in their hand, as well as through regular communications elsewhere, keeping them up to date, informed and with enough guidance to constantly refine their investment toolkit.

Democratising finance for all is our goal and that starts with giving the UK the confidence to take the first step. Have a read of the full report here.

Sources:

[1] OECD, NAAG, 2022 [2] HM Treasury, Spring Statement, March 2025 [3] The Investment Association, press release, March 2025 [4] House of Lords Financial Services Regulation Committee, 5 February 2025 [5] OECD/INFE International Survey of Adult Financial Literacy Competencies, 2016 [6] Aviva, ‘Breaking down barriers to the gender investment gap’, 2024 [7] Hargreaves Lansdown

Important information

When investing, your capital is at risk. The value of your investments, and the income you receive from them, can go down as well as up and you may get back less than you invest. Forecasts aren’t a reliable guide to future results or returns.

Make sure to do your own research on what investments are right for you before investing or consider seeking expert financial advice. Please note that this article is meant for information and does not constitute any financial advice. This is not an offer, recommendation, inducement or invitation to buy, sell, or hold any securities, or to engage in any investment activity or strategy.