Advanced options strategies (Level 3)

Options are some of the most flexible of investment strategies. Whether you're hedging or seeking to grow your investments, options may help you reach the goals you set for your portfolio.

Use this as an educational tool to learn about the options strategies available with Level 3 on Robinhood. Before you begin trading options, it's important to identify an investment strategy that makes sense for you.

Depending on your position, it’s possible for you to lose the principal you invest, or potentially more. So, it's important to learn about the different strategies before diving in.

Level 3 options trading is available in margin accounts, but not in cash accounts or Robinhood Retirement.

Long straddle

What’s a long straddle?

A long straddle is a two-legged, volatility strategy that involves simultaneously buying a call and put with the same strike prices. Both options have the same expiration date and are on the same underlying stock or ETF. Typically, both options are at-the-money.

A long straddle is a premium buying strategy. Since you’re buying 2 options you’ll pay a net debit to open the position. Like most long premium strategies, the goal of buying a straddle is to sell it later, hopefully for a profit. In order to profit, you’ll need a substantial move in the underlying’s price (in either direction).

Although a straddle is designed to profit if the underlying stock moves up or down, buying one can be costly and it has a lower theoretical probability of success than buying a single call or put. Despite this, it’s common for a straddle to have some value left at expiration. Since both options share the same strike price, it’s rare for the underlying stock to expire exactly at the strike price. If it did, it’s possible you’ll lose the entire premium paid for both options.

When to use it

A long straddle is a volatility strategy. You might consider using it when you’re unsure which direction the underlying stock will move, but you think it’s going to make a large move up or down. Also, a long straddle benefits from an increase in implied volatility. Since buying a straddle can be expensive, traders often buy them with shorter-dated options in anticipation of an upcoming event, like an earnings announcement. This is one way to speculate on the outcome of an event when you don’t know which direction the underlying stock will go, but you think it could make a large move up or down.

Building the strategy

To buy a straddle, pick an underlying stock or ETF, select an expiration date, and choose a call and a put. Almost always, both strikes are at-the-money. For example, imagine the underlying stock is trading at $99.78 and the closest strike prices are $99 and $100. The at-the-money strike price would then be $100. An example straddle would be to buy a $100 put and a $100 call with the same expiration date.

Straddles are traded simultaneously using a multi-leg order. A multi-leg order is a combination of individual orders, known as legs. The combined order is sent and both legs must be executed simultaneously on one exchange. You can also leg into the strategy by opening one leg first and the other later using individual orders. This is a more complicated approach and carries certain risks.

After you’ve built the straddle, choose a quantity, select your order type, and specify your price. The net price of the straddle is a combination of the 2 individual options. As such, it will have its own bid/ask spread. When buying a straddle, the closer your order price is to the natural ask price, the more likely your order will be filled.

Due to the nature of multi-leg pricing, many traders will work their orders, trying to get filled closer to the mid or mark price (halfway between the bid and ask prices of the spread). It’s possible you might get a fill, but more likely, you’ll need a seller to drop their asking price. Once you’ve selected a price, confirm your order details, and when you’re ready, submit the order.

The goal

A long straddle is typically used to speculate on the future volatility of the underlying stock and has no directional bias. Instead, you want the underlying stock or ETF to make a large move up or down. If this happens, one option will likely increase in value, while the other typically decreases. This creates potential opportunities to sell the straddle for a profit before expiration. While this may seem like a foolproof strategy, it’s not that simple.

If the market anticipates either higher or lower volatility, the cost of options will also be higher or lower. Essentially, you’ll need the underlying stock to move far enough to offset both the cost and time decay of the straddle. Put another way, the underlying stock must be more volatile than what the market was expecting. And since a straddle is commonly constructed with at-the-money options, the magnitude of the move may need to be substantial.

Cost of the trade

When you buy a straddle you’re buying 2 options: a call and a put. As a result, you pay 2 premiums. For example, imagine an at-the-money call that’s trading for $5 and an at-the-money put for $5.25. You’d pay $10.25 to buy the straddle. And since each option typically controls 100 shares of the underlying asset, your out-of-pocket cost would be $1,025 for each straddle you purchase.

Factors to consider

Look for an underlying stock or ETF that is likely to break out of its range and make a large move in either direction before the expiration date of the options you’ve chosen. Consider one on the lower end of its implied volatility range, with potential to increase over the life of the trade. It may be advisable to look for underlyings with more liquid options that have tighter bid/ask price spreads, larger volumes, and plenty of open interest.

Choose an expiration date that aligns with your expectation for when the underlying price will move. Shorter-dated straddles are cheaper and more commonly used to trade an upcoming event, like earnings. However, time decay will come out of the options almost immediately after the event occurs, potentially resulting in an implied volatility crush (IV crush). Meanwhile, medium- and longer-dated straddles are more expensive but have a longer timeframe for the underlying stock to potentially move while mitigating losses from time decay, which accelerate as the expiration approaches.

Straddles are typically created by using the at-the-money strike price. This means the put and call strike will be identical and closest to the current stock price.

The total premium paid (and how many straddles you purchase) determines your risk. The general guideline for many traders is to risk no more than 2-5% of their total account value on a single trade. For example, if your account value was $10,000, you’d risk no more than $200-$500 on a single trade. Remember that long straddles are costly, and typically have less than a 50% probability of success. Manage your risk accordingly.

How is a straddle different from a strangle?

Although long straddles and long strangles are both volatility strategies, there are major differences between them:

A straddle consists of a call and put with the same strike price, whereas a strangle consists of a call and put with different strike prices.

A straddle typically uses at-the-money options, whereas a strangle typically uses out-of-the-money options.

The value of a straddle is more reactive to price changes of the underlying stock compared to a strangle. This means the same price change of the underlying will typically cause the straddle to gain or lose more value than a strangle.

A straddle is typically more expensive than a strangle but has a higher probability of success.

Because the 2 options of a straddle share the same strike price, more often than not, one option will have value at expiration while the other will expire worthless. Meanwhile, both options of a strangle can and often do expire worthless.

Straddles are less sensitive to time decay and will hold a larger percentage of their value throughout equal time periods, assuming all other factors remain constant.

P/L Chart at expiration

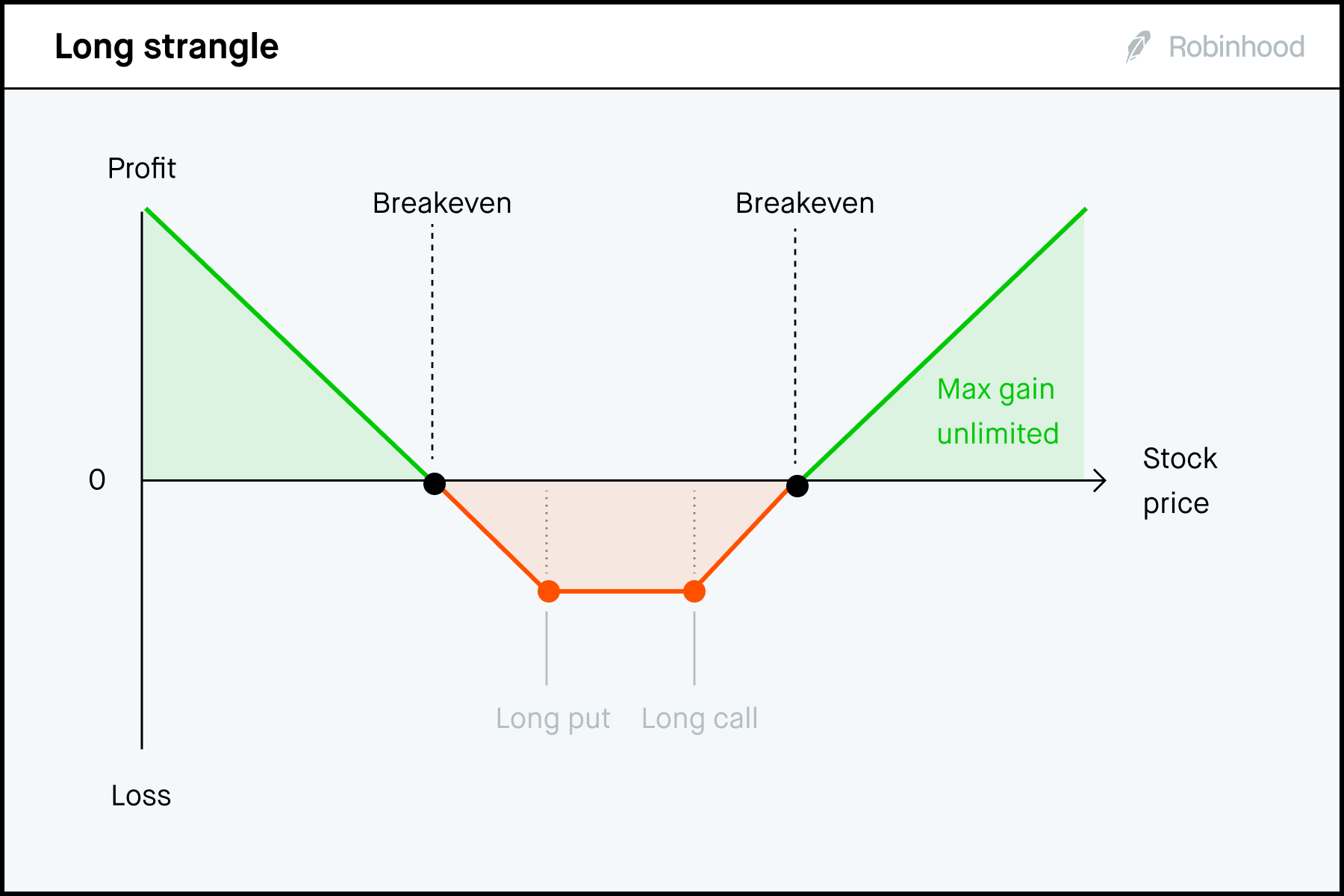

A long straddle has an unlimited theoretical max gain and a theoretical max loss that’s limited to the premium paid. At expiration it profits if the underlying stock is trading above the upper breakeven price or below the lower breakeven price at expiration.

Theoretical max gain

The theoretical max gain is unlimited, because it contains a long call. A long call has theoretically unlimited profit potential, while the theoretical max gain of the long put is also large, but limited, if the underlying stock price falls to $0.

Theoretical max loss

The theoretical max loss is limited to the total premium paid for the straddle. If the underlying stock is trading exactly at the strike price of your straddle at expiration, both options will be out-of-the-money and expire worthless. Although this is possible, it’s unlikely. It’s common for a straddle to expire with some value.

Breakeven point at expiration

At expiration, a straddle has 2 breakeven points—one above the strike price of the straddle, and one below. To calculate the upside breakeven, add the total premium paid to the strike price of the long call. To calculate the downside breakeven, subtract the total premium paid from the put’s strike price.

Is it possible to lose more than the theoretical max loss?

Yes. If either your call or put is exercised, you’ll purchase or sell 100 shares of the underlying stock. In this scenario, you’ll either own stock or possibly be short stock. With either of these positions, it’s possible to experience losses greater than the premium paid for the straddle.

Example

Imagine XYZ stock is trading for $100.25. The following lists the options expiring in 60 days. The options shaded in green are in-the-money, the ones shaded in white are out-of-the-money. The at-the-money strike is the $100 strike.

You think the stock price will move in either direction over the next 2 months and decide to buy the XYZ $100 straddle.

Buy 1 XYZ $100 Put for ($5.85)

Buy 1 XYZ $100 Call for ($7.70)

= Total net debit is ($13.55)

The theoretical max gain to the upside is unlimited, because there’s no limit to how high the XYZ’s stock price can rise. Meanwhile, the theoretical max gain to the downside is $8,645. This is calculated by subtracting the total premium paid ($13.55) from the strike price of the put ($100).

The theoretical max loss occurs if XYZ closes exactly at $100 at expiration. In this scenario, both options would be out-of-the-money and expire worthless. Your loss would be limited to the total premium paid for the straddle, which was $13.55 per share, or $1,355 total. Although this is possible, the probability of XYZ closing exactly at $100 on expiration is typically low.

The breakeven points at expiration are $86.45 or $113.55. Remember, there are 2 breakeven prices at expiration for a straddle. The lower breakeven is calculated by subtracting the total premium paid ($13.55) from the put strike price ($100). The higher breakeven is calculated by adding the total premium paid ($13.55) to the call strike price ($100).

This is a theoretical example. Actual gains and losses will depend on a number of factors, such as the actual prices and number of contracts involved.

Managing the trade

A long straddle benefits if the underlying stock price rises or falls sharply and quickly. In addition, if implied volatility rises, both options will likely increase in value if all other factors remain constant. Around 30-45 days to expiration, time decay begins to accelerate and the closer your straddle is to expiration, the more extrinsic value each option will lose each day. Ultimately, the value of the call or put will only be worth its intrinsic value (the in-the-money amount) at expiration.

At some point, you’ll need to decide whether or not to sell your straddle or hold it into expiration. If the combined position is profitable, consider taking action before expiration. The longer you wait, the more extrinsic value will come out of both options. Of course, this may be offset by any movement in the underlying stock price.

Meanwhile, a decreasing implied volatility and a stable, sideways moving stock price will hurt the value of your straddle. This isn't ideal. If the position is worth less than your original purchase price, you can attempt to cut your losses and close it before expiration. While it isn’t common, if both options are out-of-the-money at expiration, the position will expire worthless, and you’ll take a max loss on the trade.

Option Greeks

A long straddle contains both a long call and put. The Greeks are netted to arrive at a net delta, gamma, theta, vega, and rho for the combined position. When the trade is established, the straddle is delta and rho neutral. It has a negative theta, a positive gamma, and a positive vega. Over time, these can change as the underlying stock moves up or down.

If the stock rises, the put’s deltas will decrease and the call’s deltas will increase. Conversely, if the stock drops, the long put’s deltas will increase and the long call’s deltas will decrease. If implied volatility increases, vega will likely increase the value of both options. As time goes by, theta will reduce the value of both options.

Bottom line, this strategy is about movement—you want the underlying stock to make a large move in either direction before time decay kicks in. Meanwhile, a spike in implied volatility will likely benefit both options.

Keep in mind: Option Greeks are calculated using options pricing models and are theoretical estimates. All Greek values assume all other factors remain equal.

Closing the position

Although you have the right to exercise either of your options, typically, this isn't how many traders close a long straddle. Instead, you might consider selling your straddle before expiration to avoid the exercise process and any additional risk that it may introduce. Whichever you choose, it’s best to establish an exit strategy for your trade before you enter it. You can do the following to close a long straddle:

- Sell to close your position

- Leg out of your position

- Exercise early

- Hold through expiration

Sell to close your position

To close your position, take the opposite actions that you took to open it. For a long straddle, this involves simultaneously selling-to-close both the long call and long put. Typically, you’ll collect a net credit to close your position. In doing so, you’ll realize any profits or losses associated with the trade. If you sell your straddle for more than your purchase price, you’ll profit. If you sell it for less than your purchase price, you’ll realize a loss. And if you sell it at the same price as your purchase price, you’ll break even.

Leg out

Some traders prefer to leg out of a straddle. You can do this by selling one option, and then selling the other option later, using separate orders. This approach includes both benefits and risks. You can do this to help mitigate liquidity concerns or change the structure of your strategy.

Exercise early

When you own a straddle, you have the right to buy or sell 100 shares of the underlying asset at the strike price by expiration (assuming you have the required buying power to exercise the call or necessary shares to exercise the put). Typically, you’d only consider doing this if one of your options is in-the-money at expiration.

However, if you exercise before expiration, you’ll forfeit any extrinsic value (time value) remaining in the option. For this reason, it rarely makes sense to exercise a call or put option prior to expiration. However, there are some scenarios where exercising early could make sense, including:

To capture an upcoming dividend payment. Remember, shareholders receive dividends, options holders do not. If your call option is in-the-money, and the remaining extrinsic value is less than the upcoming dividend, it could make sense to exercise the call of your straddle prior to the ex-dividend date.

To ensure you’re capturing the intrinsic value of the option. If you cannot sell to close your call or put option for at least its intrinsic value (the in-the-money amount), you can exercise the option and offset it with the necessary sale or purchase of shares to close the resulting long or short underlying stock position.

To reduce your margin interest. Interest rates are an important factor in determining whether or not to early exercise a put option. While there is no hard or fast rule, you may choose to exercise a deep in-the-money put to reduce your margin interest (assuming you bought the stock or ETF on margin). When you sell shares, you reduce your margin balance.

Finally, don't exercise an out-of-the-money option. If you do this, you’re simply buying or selling shares at a worse price than what they’re currently priced in the open market. If you want to own the shares, it’s often better to sell your long call, and then buy the shares in a separate transaction. If you want to sell the shares, it’s often better to sell your put, and then sell the shares in a separate transaction.

Hold through expiration

Holding your position into expiration can result in a max gain or loss scenario and carries certain risks that you should be aware of. Learn more about expiration, exercise, and assignment.

If both options expire out-of-the-money, both options will expire worthless and be removed from your account. You’ll lose the premium you paid for both options and will realize a max loss.

If one option expires in-the-money, and the other expires out-of-the-money, one of your options will be automatically exercised. 100 shares of the underlying will either be purchased (if the call is exercised) or sold (if the put is exercised) for every contract exercised. The other option will expire worthless and be removed from your account. If you don't have the necessary buying power or shares to support the exercise, Robinhood may attempt to place a Do Not Exercise (DNE) request on your behalf.

Note: If you don’t want your options to be exercised, you can submit a Do Not Exercise (DNE) request by contacting our Support team. To implement a DNE request, you can submit it after 4 PM ET, and we must receive it by no later than 5 PM ET on the expiration date. (This only applies to regular market hour days.)

Additional risks

For a long straddle, be cautious of automatic exercise. As mentioned, if your call option is in-the-money at expiration, your long call will automatically be exercised, and you’ll buy 100 shares of the underlying for each contract that’s exercised. If you don’t have the available funds to support the exercise, your account will be in a deficit.

If your put option is in-the-money at expiration, your long put will automatically be exercised, and you’ll sell 100 shares of the underlying for each contract that’s exercised. If you don’t own the underlying shares, this will result in a short stock position, which has undefined risk, and isn't allowed at Robinhood.

Important: To help mitigate these risks, Robinhood may close your position prior to market close on the expiration date; however, this is done on a best-effort basis. Ultimately, you're fully responsible for managing the risk within your account.

What happens if a corporate action impacts the underlying asset?

Sometimes, the option’s underlying stock can undergo a corporate action, such as a stock split, a reverse stock split, a merger, or an acquisition. A corporate action can impact the option you hold, such as changes to the option’s structure, price, or deliverable.

Long strangle

What’s a long strangle?

A long strangle is a two-legged, volatility strategy that involves simultaneously buying a call and put with different strike prices. Both options have the same expiration date and are on the same underlying stock or ETF. Typically, both options are out-of-the-money and equidistant from the underlying stock price.

A long strangle is a premium buying strategy. Since you’re buying 2 options you’ll pay a net debit to open the position. Like most long premium strategies, the goal of buying a strangle is to sell it later, hopefully for a profit. In order to profit, you’ll need a substantial move in the underlying’s price (in either direction).

Although a strangle is designed to profit if the underlying stock moves up or down, buying strangles can be costly, and they can have a low theoretical probability of success. If the underlying stock or ETF doesn’t move far enough, it’s possible you’ll lose the entire premium paid for both options.

When to use it

A long strangle is a volatility strategy. You might use it when you’re unsure which direction the underlying stock will move, but you think it’s going to make a large move up or down. In addition, a long strangle benefits from an increase in implied volatility and is a cheaper alternative to buying a straddle. However there are tradeoffs between the 2 strategies.

Building the strategy

To buy a strangle, pick an underlying stock or ETF, select an expiration date, and choose a call and a put. Typically, the 2 strikes are out-of-the-money and equidistant from the current underlying stock price.

For example, if the underlying stock is trading at $100, an example strangle would be buying the $95 put and the $105 call. If you have a stronger feeling about the stock moving up or down you could also skew your strangle, meaning your options aren't equidistant from the underlying stock price. This is a more complex approach to the strategy and would be considered a variation.

Strangles are traded simultaneously using a multi-leg order. A multi-leg order is a combination of individual orders, known as legs. The combined order is sent and both legs must be executed simultaneously on one exchange. You can also leg into the strategy by opening 1 leg first and the other later using individual orders. This is a more complicated approach and carries certain risks.

After you’ve built the strangle, choose a quantity, select your order type, and specify your price. The net price of the strangle is a combination of the 2 individual options. As such, it will have its own bid/ask spread. When buying a strangle, the closer your order price is to the natural ask price, the more likely your order will be filled.

Due to the nature of multi-leg pricing, many traders will work their orders, trying to get filled closer to the mid or mark price (halfway between the bid and ask prices of the spread). It’s possible you might get a fill, but more likely, you’ll need a seller to drop their asking price. Once you’ve selected a price, confirm your order details, and when you’re ready, submit the order.

Note: There’s also a variation of a strangle that involves buying 2 in-the-money options. It’s called a “gut strangle” and is a seldom-used strategy. While it might work in rare circumstances, the cost and risk associated with buying a guts strangle generally keeps some traders away from this variation.

The goal

A long strangle is typically used to speculate on the future volatility of the underlying stock and has no directional bias. Instead, you want the underlying stock or ETF to make a large move up or down. If this happens, one option will likely increase in value, while the other typically decreases. This creates potential opportunities to sell the strangle for a profit before expiration. While this may seem like a foolproof strategy, it’s not that simple.

If the market anticipates higher volatility, the cost of options will be higher, and vice versa. Essentially, you’ll need the underlying stock to move far enough to offset the cost of the strangle. Put another way, the underlying stock must be more volatile than what the market was expecting. And since a strangle is commonly constructed using out-of-the-money options, the magnitude of the move may need to be substantial.

Cost of the trade

When you buy a strangle you’re buying 2 options, a call and a put. As a result, you pay 2 premiums. For example, imagine a call trading for $2 and a put $2.25. You’d pay $4.25 to buy the strangle. And since each option typically controls 100 shares of the underlying asset, your out-of-pocket cost would be $425 for each strangle you purchase.

Factors to consider

Look for an underlying stock or ETF that is likely to break out of its range and make a large move in either direction before the expiration date of the options you’ve chosen. Consider one on the lower end of its implied volatility range, with potential to increase over the life of the trade. It may be advisable to look for underlyings with more liquid options that have tighter bid/ask price spreads, larger volumes, and plenty of open interest.

Choose an expiration date that aligns with your expectation for when the underlying price will move. Shorter-dated strangles are cheaper, but will be more impacted by time decay. Longer-dated strangles are more expensive and more sensitive to changes in implied volatility. Meanwhile options expiring in 60-90 days provide a window for the underlying stock to potentially move while balancing costs and mitigating losses from time decay, which accelerate as expiration approaches.

Strangles are typically created using out-of-the-money strike prices. That means the put’s strike will be below the current underlying stock price and the call’s strike will be above it. The closer your strikes are to the underlying stock price, the more expensive it will be, but the probability of success is greater. Meanwhile, the further out-of-the-money your strikes are, the less expensive the strangle will be, but the probability of success will be much lower.

The total premium paid (and how many strangles you purchase) determines your risk. Many traders adhere to the general guideline of not risking more than 2-5% of their total account value on a single trade. For example, if your account value was $10,000, you’d risk no more than $200-$500 on a single trade. Ultimately, it’s up to you to decide. Remember that long strangles are costly, and typically have less than a 50% probability of success. Manage your risk accordingly.

How is buying a strangle different from buying a straddle?

Although long strangles and long straddles are both volatility strategies, there are many differences between them.

Strangles consist of a call and put with different strike prices. Straddles consist of a call and put with the same strike price.

Strangles are typically created using out-of-the-money options, whereas a straddle typically uses at-the-money options.

The value of a strangle is less reactive to price changes of the underlying compared to a straddle. This means the same price change of the underlying will typically cause the straddle to gain or lose more value than a strangle.

A long strangle is typically cheaper than buying a straddle but has a lower probability for success.

The options within a strangle can and often do expire worthless. Meanwhile, because the 2 options of a straddle share the same strike price, more often than not, one option will have value at expiration while the other will expire worthless.

Strangles are more sensitive to time decay. Meanwhile, a straddle will hold a larger percentage of its value throughout equal time periods, all other factors remaining constant.

P/L Chart at expiration

A long strangle has an unlimited theoretical max gain and a limited theoretical max loss. At expiration, it profits if the underlying stock is trading above the upper breakeven price, or below the lower breakeven price.

Theoretical max gain

The theoretical max gain is unlimited because it contains a long call. A long call has theoretically unlimited profit potential, while the theoretical max gain of the long put is also large, but limited if the underlying stock price falls to $0.

Theoretical max loss

The theoretical max loss is limited to the total premium paid for the strangle. If the underlying stock is trading between the 2 strike prices at expiration, both options will be out-of-the-money and expire worthless.

Breakeven point at expiration

At expiration, a strangle has 2 breakeven points—one above the call strike and one below the put strike. To calculate the upside breakeven, add the total premium paid to the strike price of the long call. To calculate the downside breakeven, subtract the total premium paid from the put’s strike price.

Is it possible to lose more than the theoretical max loss?

Yes. If either your call or put is exercised, you’ll purchase, or sell 100 shares of the underlying stock. In this scenario, you’ll either own stock, or possibly be short stock, and it’s possible to experience losses greater than the premium paid for the strangle.

Example

Imagine XYZ stock is trading for $100.25 The following lists the options expiring in 60 days. The options shaded in green are in-the-money, the ones shaded in white are out-of-the-money.

You think the stock price will move in either direction over the next 2 months. You decide to buy the $95/$105 strangle expiring in 60 days.

Buy 1 XYZ $95 Put for ($4.20))

Buy 1 XYZ $105 Call for ($4.95)

= Total net debit is ($9.15)

The theoretical max gain to the upside is unlimited because there’s no limit to how high the XYZ’s stock price can rise. Meanwhile, the theoretical max gain to the downside is $8,585. This is calculated by subtracting the total premium paid ($9.15) from the strike price of the put ($95). Although this is unlikely, it’s always possible.

The theoretical max loss is $9.15 per share, or $915 total. Max loss occurs if XYZ closes between $95 and $105 at expiration. In this scenario, both options would be out-of-the-money, and expire worthless.

The breakeven point at expiration is $85.85 or 114.15. Remember, there are 2 breakeven points at expiration. The lower breakeven is calculated by subtracting the total premium paid ($9.15) from the lower put strike price ($95). The higher breakeven is calculated by adding the total premium paid ($9.15) to the higher call strike price ($105).

This is a theoretical example. Actual gains and losses will depend on a number of factors, such as the actual prices and number of contracts involved.

Managing the trade

A long strangle benefits if the underlying stock price rises or falls sharply and quickly, ideally above or below the strike prices of the strangle. In addition, if implied volatility rises both options will likely increase in value, all other factors held constant.

Around 30 days to expiration, time decay begins to accelerate and the closer your strangle is to expiration, the more extrinsic value each option will lose each day. Ultimately, the value of your strangle will only be worth its intrinsic value (the in-the-money amount) at expiration.

At some point, you must decide whether or not to sell your strangle, or hold it into expiration. If the combined position is profitable, consider taking action before expiration. The longer you wait, the more extrinsic value will come out of both options. Of course, this may be offset by any movement in the underlying stock price.

Meanwhile, a decreasing implied volatility, and a stable, sideways moving stock price will hurt the value of your strangle. This isn't ideal. If the position is worth less than your original purchase price you can attempt to cut your losses and close it before expiration. If both options are out-of-the-money at expiration, the position will expire worthless, and you’ll take a max loss on the trade.

Option Greeks

A long strangle involves both a long call and put. The Greeks are netted to arrive at a net delta, gamma, theta, vega, and rho for the combined position. When the trade is established, the strangle is delta and rho neutral. It has a negative theta and a positive gamma and vega. Over time, delta and gamma can change as the underlying stock moves up or down.

If the stock rises, the put’s deltas will decrease and the call’s deltas will increase. Conversely, if the stock drops, the long put’s deltas will increase and the long call’s deltas will decrease. If implied volatility increases, vega will likely increase the value of both options. As time goes by, theta will reduce the extrinsic value of both options.

Bottom line, this strategy is about movement—you want the underlying stock to make a large move in either direction before time decay kicks in. Meanwhile, a spike in implied volatility will likely benefit both options.

Keep in mind: Option Greeks are calculated using options pricing models and are theoretical estimates. All Greek values assume all other factors remain equal.

Closing the position

Although you have the right to exercise either of your options, typically, this isn't how many traders close a long strangle. Instead, you might consider selling your strangle before expiration to avoid the exercise process, and any additional risk that it may introduce. Whichever you choose, it’s best to establish an exit strategy for your trade before you enter it. To close a long strangle you can do the following that's described in this section:

- Sell to close your position

- Leg out of your position

- Exercise early

- Hold through expiration

Sell to close your position

To close your position, take the opposite actions that you took to open it. For a long strangle, this involves simultaneously selling-to-close both the long call and long put. Typically, you’ll collect a net credit to close your position. In doing so, you’ll realize any profits or losses associated with the trade. If you sell your strangle for more than your purchase price, you’ll profit. If you sell it for less than your purchase price, you’ll realize a loss. And if you sell it at the same price as your purchase price, you’ll break even.

Leg out of your position

Some traders prefer to leg out of a strangle. You can do this by selling one option, and then selling the other option later, using separate orders. This approach includes both benefits and risks. You can do this to mitigate liquidity concerns or change the structure of your strategy.

Exercise early

When you own a strangle, you have the right to buy or sell 100 shares of the underlying asset at the strike price by expiration (assuming you have the required buying power to exercise the call or necessary shares to exercise the put). Typically, you’d only consider doing this if one of your options is in-the-money at expiration.

However, if you exercise before expiration, you’ll forfeit any extrinsic value (time value) remaining in the option. For this reason, it rarely makes sense to exercise a call or put option prior to expiration. However, there are some scenarios where exercising early could make sense, including:

To capture an upcoming dividend payment. Remember, shareholders receive dividends, options holders do not. If your call option is in-the-money, and the remaining extrinsic value is less than the upcoming dividend, it could make sense to exercise the call of your strangle prior to the ex-dividend date.

To ensure you’re capturing the intrinsic value of the option. If you cannot sell to close your call or put option for at least its intrinsic value (the in-the-money amount), you can exercise the option and offset it with the necessary sale or purchase of shares to close the resulting long or short underlying stock position.

To reduce your margin interest. Interest rates are an important factor in determining whether or not to early exercise a put option. While there is no hard or fast rule, you may choose to exercise a deep in-the-money put to reduce your margin interest (assuming you bought the stock or ETF on margin). When you sell shares, you reduce your margin balance.

Finally, don't exercise an out-of-the-money option. If you do this, you’re simply buying or selling shares at a worse price than what they’re currently priced in the open market. If you want to own the shares, it’s often better to sell your long call, and then buy the shares in a separate transaction. If you want to sell the shares, it’s often better to sell your put, and then sell the shares in a separate transaction.

Hold through expiration

Holding your position into expiration can result in a max gain or loss scenario and carries certain risks that you should be aware of. Learn more about expiration, exercise, and assignment.

If both options expire out-of-the-money, both options will expire worthless and be removed from your account. You’ll lose the premium you paid for both options and will realize a max loss.

If one option expires in-the-money and the other expires out-of-the-money, one of your options will be automatically exercised. 100 shares of the underlying will either be purchased (if the call is exercised) or sold (if the put is exercised) for every contract exercised. The other option will expire worthless and be removed from your account. If you don't have the necessary buying power or shares, Robinhood may attempt to place a Do Not Exercise (DNE) request on your behalf.

Note: If you don’t want your options to be exercised, you can submit a Do Not Exercise (DNE) request by contacting our Support team. To implement a DNE request, you can submit it after 4 PM ET, and we must receive it by no later than 5 PM ET on the expiration date. (This only applies to regular market hour days.)

Additional risks

For a long strangle, be cautious of automatic exercise. As mentioned, if your call option is in-the-money at expiration, your long call will automatically be exercised, and you’ll buy 100 shares of the underlying for each contract that’s exercised. If you don’t have the available funds to support the exercise, your account will be in a deficit.

If your put option is in-the-money at expiration, your long put will automatically be exercised, and you’ll sell 100 shares of the underlying for each contract that’s exercised. If you don’t own the underlying shares, this will result in a short stock position, which has undefined risk, and isn't allowed at Robinhood.

Important: To help mitigate these risks, Robinhood may close your position prior to market close on the expiration date; however, this is done on a best-effort basis. Ultimately, you are fully responsible for managing the risk within your account.

What happens if a corporate action impacts the underlying asset?

Sometimes, the option’s underlying stock can undergo a corporate action, such as a stock split, a reverse stock split, a merger, or an acquisition. A corporate action can impact the option you hold, such as changes to the option’s structure, price, or deliverable.

Call debit spread

What’s a call debit spread?

A call debit spread is one type of vertical spread. It’s a bullish, two-legged options strategy that involves buying a call option and selling another with a higher strike price. Both options have the same expiration date and underlying stock or ETF. This strategy is also known as a long call vertical, long call spread, or bull call spread.

A call debit spread is a premium buying strategy. Typically, the debit you pay for buying the lower-strike call is greater than the credit you’ll receive for selling the higher-strike call. Therefore, you’ll pay a net debit to open the position. It’s called a spread because the value of the position is based on the difference or spread between the strike prices.

When to use it

A call debit spread is a bullish strategy because ideally you want the price of the underlying to rise beyond the short strike. You might consider a call debit spread when you’re bullish but believe the upside move will be limited. If you’re extremely bullish, buying a call may provide a more desirable profit potential.

Compared to a long call, a call debit spread is less expensive. In a sense, the short call helps finance the purchase of the long call. This limits the theoretical max gain but increases your theoretical probability of success by lowering the breakeven price the stock needs to reach by expiration. The tradeoff is your potential profit is much lower. Meanwhile, buying a call offers unlimited profit potential, but has a lower probability of success.

Building the strategy

To buy a call spread, pick an underlying stock or ETF, select an expiration date, and choose the strike prices. Typically, a call debit spread is constructed in one of 2 ways:

- Buying an in-the-money call option and selling an out-of-the-money call option (called an “in and out” spread)

- Buying and selling out-of-the-money call options

Debit spreads traded simultaneously using a spread order. A spread order is a combination of individual orders, known as legs. The combined order is sent and both legs must be executed simultaneously on one exchange. You can also leg into the strategy by opening one leg first and the other later using individual orders. This is a more complicated approach and carries certain risks.

The width of the spread is the distance between the short and long strike prices and is a key detail. A narrower spread has a lower potential profit but requires less collateral and has less theoretical risk. Meanwhile, a wider spread has a higher potential profit but is more expensive and has greater theoretical risk.

After you’ve built the spread, choose a quantity, select your order type, and specify your price. The net price of the spread is a combination of the individual options (the one you’re buying and the one you’re selling). As such, the debit spread will have its own bid/ask spread. When buying a spread, the closer your order price is to the natural ask price, the more likely your order will be filled.

Due to the nature of spread pricing, many traders will work their orders, trying to get filled closer to the mid or mark price (halfway between the bid and ask prices of the spread). It’s possible you might get a fill, but more likely, you’ll need a seller to drop their asking price. Once you’ve selected a price, confirm your order details, and when you’re ready, submit the order.

The goal

A call debit spread is commonly used to speculate on the future direction of the underlying stock. When buying a call spread you want both options to increase in value. This happens when the underlying stock price rises (ideally above the long and short call strikes) and implied volatility increases. Prior to expiration, if the spread is worth more than your original purchase price, you can attempt to close it for a profit.

If you hold the position through expiration, and the underlying stock is trading above the strike price of your short call, both options should expire in-the-money, your long call will be exercised, and your short call will likely be assigned, resulting in a max gain on the trade.

Cost of the trade

To buy a call debit spread, you must pay a net debit. Let’s say, the long call is worth $4 and the short call is worth $2. The net debit to purchase this call spread is $2 ($4 minus $2). Since a standard option controls 100 shares of the underlying, you’d need $200 to purchase one spread. To buy 10 spreads, you’d need $2,000, and so on.

Factors to consider

Look for an underlying stock or ETF whose price is trending up or likely to increase soon. Consider one on the lower end of its implied volatility range, with potential to increase over the life of the trade. It may be advisable to look for underlyings with more liquid options that have tighter bid/ask price spreads, larger volumes, and plenty of open interest.

Choose an expiration date that aligns with your expectation for when the underlying price will increase. Technically, you can choose any available expiration date, but the textbook approach is to generally buy a call spread with about 30-60 days until expiration. This provides a window of time for the underlying price to potentially go up, while not spending too much time waiting for the time value of the short call to decay.

Which strike prices you choose to buy and sell is an important consideration.

- Buying an in-the-money call and selling an out-the-money call (in and out spread) balances the considerations of wanting the long strike to be in-the-money while allowing the underlying to rise up to the short strike. Often, traders will look to buy the first in-the-money call and sell an out-of-the-money call based on their preferred risk and reward ratio.

- Buying an out-of-the-money call and selling an out-the-money call. This is a more bullish approach. While the cost of this spread can be cheaper than an in and out spread, the theoretical probability of success is lower. Essentially, you’ll be paying less to make more, but will need the underlying stock to increase a greater amount.

Important: It’s best to avoid buying an in-the-money call spread. An in-the-money call spread is when both strike prices are below the underlying stock price. Although it may appear to have a high probability of success, your short call may be assigned early and you might be exposed to dividend risk. Instead, you can achieve a similar risk and reward profile by selling an out-of-the-money put spread with the same strikes while avoiding these risks.

The net debit and width of the spread determine the risk and reward of the trade. For example, if you bought a 10-point wide spread for $1, you’d be risking $100 to make $900 and would theoretically have a 10% of success. If you paid $5 for the same 10-point spread, you’d be risking $500 to make $500, and would theoretically have a 50/50 chance of success. Taking this into account, some traders adhere to the general guideline of not paying less than ¼ or more than ½ the width of the spread. This roughly translates to a 25-50% theoretical chance of success on the trade. Ultimately, you decide which risk and reward ratio is appropriate based on your opinion of how far the underlying stock will move by expiration.

How is a call debit spread different from only buying a call?

Buying a call option and buying a call spread are both bullish strategies. They’re opened for a debit, and perform best when the underlying stock or ETF makes a significant move to the upside. Both strategies include a long option and the theoretical max loss is limited to the total premium paid.

However, a call debit spread includes a short call, which changes the risk profile of the trade. Since the underlying stock or ETF can rise to virtually any number, buying a call option has unlimited profit potential. Yet, a call debit spread has limited profit potential. By selling a call at a higher strike price, a call debit spread will always be cheaper than buying a single call option (assuming the same long call). While this decreases your risk and increases your theoretical probability of success, it also limits your potential gains.

P/L Chart at expiration

A call debit spread has both defined theoretical profit and loss. At expiration, it profits if the underlying stock is trading above the breakeven price.

Theoretical max gain

The theoretical max gain is limited to the width of the spread, minus the net debit paid. To realize a max gain, the underlying stock price must close above the strike price of the short call at expiration.

Theoretical max loss

The theoretical max loss is limited to the net debit paid to open the spread. Max loss occurs when the price of the underlying closes below the strike price of the long call at expiration, and both calls expire worthless.

Breakeven point at expiration

At expiration, the breakeven point is calculated by adding the net debit to the strike price of the long call.

Is it possible to lose more than the theoretical max loss?

Yes. If you close the short call and keep the long call, the risk profile (as described earlier) no longer holds true. Your risk and reward will be that of a long call until expiration. If your long call is exercised, you’ll purchase 100 shares of the underlying stock. Owning shares can result in losses greater than the premium paid for the call option.

Example

Imagine XYZ stock is trading for $100. The following lists the options expiring in 30 days. The options shaded in green are in-the-money, the ones shaded in white are out-of-the-money.

You’re bullish and expect XYZ stock to rise above $105 over the next 30 days. You decide to buy the $100/$105 call debit spread:

Buy 1 XYZ $100 Call for ($3.70)

Sell 1 XYZ $105 Call for $1.75

= Total net debit is ($1.95)

The theoretical max gain is $3.05 per share, or $305. This is calculated by taking the width of the spread ($5) and subtracting the net debit paid ($1.95). Max gain is realized if the price of the underlying stock closes above $105 at expiration. The long call will be exercised and the short call should be assigned.

The theoretical max loss is the premium paid, which is $1.95 per share, or $195 total. Max loss occurs if the price of the underlying closes below $100 at expiration. Both calls should expire worthless.

The breakeven point at expiration is $101.95. This is calculated by taking the strike price of the long call ($100) and adding the net debit paid ($1.95).

This is a theoretical example. Actual gains and losses will depend on a number of factors, such as the actual prices and number of contracts involved.

Managing the trade

A call debit spread benefits if the underlying stock price rises above the strike price of your short option and implied volatility increases. These outcomes would likely increase the value of your call spread. That being said, the value of your short call will always offset the value of your long call. As a result, the total value of the spread will fluctuate at a slower rate compared to a single option strategy.

If the position is profitable, consider taking action before expiration. Typically, vertical spreads are managed during the week of expiration, although not always. That being said, the strategy won't approach its maximum gain or loss until it’s near expiration and the time value of both options is greatly reduced. Often, traders will exit the position for slightly less than max value to free up capital and avoid going through exercise and assignment.

If the underlying stock price falls and implied volatility decreases, the value of both options will likely decrease. This isn't ideal. If the spread is worth less than your original purchase price, you can attempt to cut your losses and close the position before expiration. You can also try to leg out by closing the short call and keeping the long call. This allows you to realize some profit on the short call, while leaving the long call intact in case the stock reverses and begins to rise.

As expiration nears, you may need to proactively manage your position if the underlying stock is trading between the 2 strikes. If no action is taken, at expiration your long call will be automatically exercised and your short call would expire worthless. This may result in a long stock position, and a potential max loss that is greater than theoretical max loss of the spread.

Keep in mind: Any time you have a short call option in your position, there’s a possibility of an early assignment, which exposes you to certain risks, like short stock or dividend risk.

Option Greeks

A call debit spread involves both a long and short call. The Greeks are netted to arrive at a net delta, gamma, theta, vega, and rho for the spread.

When the trade is established, the spread has a positive delta and negative theta. Meanwhile, gamma and vega will be slightly positive, which means the position benefits from upward movement in the underlying stock and an increase in implied volatility. Depending on where the underlying stock price is relative to either strike price, gamma, theta, and vega can be either positive or negative.

Bottom line, this strategy is about delta and theta—you want the underlying stock price to rise as quickly as possible before time decay accelerates.

Keep in mind: Option Greeks are calculated using options pricing models and are theoretical estimates. All Greek values assume all other factors are held equal.

Closing the position

Although the strategy is designed to reach max profit at expiration, you might consider closing it before then in order to free up capital and avoid the risk of going through exercise and assignment. Whichever you choose, it’s best to establish an exit strategy for your trade before you enter it. To close a call debit spread you can do the following that's described in this section:

- Sell to close the spread

- Leg out of the spread

- Hold the spread through expiration

Sell to close the spread

To close your position, take the opposite actions that you took to open it. For a call debit spread, this involves simultaneously selling-to-close the long call option (the one you initially bought to open) and buying-to-close the short call option (the one you initially sold to open).

Typically, you’ll collect a net credit to close your position. In doing so, you’ll realize any profits or losses associated with the trade. If you sell your spread for more than your purchase price, you’ll profit. If you sell it for less than your purchase price, you’ll realize a loss. And if you sell it at the same price as your purchase price, you’ll break even.

Keep in mind: Prior to expiration, you’ll unlikely be able to close the position for a max gain or max loss. In many cases, you may have to collect slightly less than theoretical value in order to close the position as expiration approaches.

Leg out of the spread

Some traders prefer to leg out of a call debit spread. You can do this by buying to close the short call option, and then selling to close the long option later, using separate orders. This approach includes both benefits and risks. You can do this to mitigate liquidity concerns or change the structure of your strategy. That being said, by doing this you could create a greater gain or loss than the max theoretical gain or loss of the original strategy.

Note: At Robinhood, to leg out of a call debit spread you must buy to close the short call option first before you can sell to close your long option.

Hold the spread through expiration

Holding your position into expiration can result in a max gain or loss scenario and carries certain risks that you should be aware of. Learn more about expiration, exercise, and assignment.

If the underlying’s price is below the long strike price, then both options should expire worthless and will be removed from your account. You’ll realize a max loss on the position.

If the underlying’s price is above the short strike price, both options will expire in-the-money. Your long call will be automatically exercised and you’ll likely be assigned on your short call. You’ll realize a max gain on the position.

If the underlying’s price closes above the long strike but below the short strike, your long call will be exercised and your short call will likely expire worthless. Be cautious of this scenario. If your long call is exercised, you’ll be left with a long stock position. Your individual investing account will display a reduced buying power or account deficit as a result of the early assignment. Meanwhile, your short call will no longer exist to offset the exercise. This may potentially result in losses greater than the theoretical max loss of the call debit spread.

Important: To help mitigate this risk, Robinhood may close your entire spread prior to market close on the expiration date; however, this is done on a best-effort basis. Ultimately, you are fully responsible for managing the risk within your account.

Additional risks

For call credit spreads, be cautious of an early assignment or an upcoming dividend.

An early assignment occurs when an option that was sold is exercised by the long holder before its expiration date. If you’re assigned on the short call option of your call debit spread, you can take one of the following actions by the end of the following trading day:

- Buy the shares at the current market price

- Exercise your long call option (thereby buying the shares at the long strike price)

In either circumstance, your individual investing account may temporarily show a reduced buying power or account deficit as a result of the early assignment. Exercise of the long call is typically settled within 1-2 trading days, and restores buying power partially or fully. To learn more, see Early assignments.

Dividend risk is the risk that you’ll be assigned on a short call option the night before the ex-dividend date (where you have to pay the dividend to the exerciser). This is one of the biggest risks of trading spreads with a short call option and could result in a greater loss (or lower gain) than the theoretical max gain and loss scenarios described earlier. Traders can avoid this by closing their position during regular trading hours prior to the ex-dividend date. To learn more, see Dividend risks.

What happens if there’s a corporate action on the underlying asset?

Sometimes, the option’s underlying stock can undergo a corporate action, such as a stock split, a reverse stock split, a merger, or an acquisition. Any corporate action will impact the option you hold, potentially resulting in changes to the option, such as its structure, price, and deliverable.

Call credit spread

What’s a call credit spread?

A call credit spread is a type of vertical spread. It’s a bearish, two-legged options strategy that involves selling a call option and buying another with a higher strike price. Both options have the same expiration date and underlying stock or ETF. This strategy is also known as a short call vertical, short call spread, or bear call spread. It’s called a spread because the value of the position is based on the difference or spread between the 2 strike prices.

A call credit spread is a premium selling strategy. Typically, the credit you receive for selling the lower-strike call is greater than the debit you’ll pay to buy the higher-strike call. Therefore, you’ll collect a net credit to open the position. Although you receive a cash credit at the outset, your potential profit or loss isn't realized until the position is closed.

When to use it

A call credit spread is a bearish strategy because ideally you want the price of the underlying to stay below the short strike. You might consider using it when you expect the price of the underlying stock to moderately decrease and implied volatility is on the high end of its range. If you’re extremely bearish, buying a put option may provide a more desirable profit potential. Although a call credit spread has a lower potential profit, it benefits from time decay and has a higher theoretical chance for success. Meanwhile, a put option offers a higher profit potential.

Building the strategy

To sell a call spread, pick an underlying stock or ETF, select an expiration date, and choose the strike prices. Credit spreads are typically constructed using out-of-the-money options, which are traded simultaneously using a spread order.

A spread order is a combination of individual orders, known as legs. The combined order is sent and both legs must be executed simultaneously on one exchange. You can also leg into the strategy by opening one leg first and the other later using individual orders. This is a more complicated approach and carries certain risks.

The width of the spread is the distance between the short and long strike prices and is a key detail. A narrower spread has a lower potential profit but requires less collateral and has less theoretical risk. Meanwhile, a wider spread has a higher potential profit but is more expensive and has greater theoretical risk.

After you’ve built the spread, choose a quantity, select your order type, and specify your price. The net price of the spread is a combination of the individual options (the one you’re buying and the one you’re selling). As such, the credit spread will have its own bid/ask spread. When selling a spread, the closer your order price is to the natural bid price, the more likely your order will be filled.

Due to the nature of spread pricing, many traders will work their orders, trying to get filled closer to the mid or mark price (halfway between the bid and ask prices of the spread). It’s possible you might get a fill, but more likely, you may need a buyer to increase their bid. Once you’ve selected a price, confirm your order details, and when you’re ready, submit the order.

The goal

A call credit spread is commonly used to generate income. When selling a call spread, you want both options to decrease in value. This happens when the underlying stock price falls (ideally staying below the short call strike), time passes, and implied volatility drops. Prior to expiration, if the spread is worth less than your original selling price, you can attempt to close it for a profit. If you hold the position through expiration, and the underlying stock is trading below the strike price of the short call, both options should expire worthless, and you’ll keep the full premium.

Cost of the trade

Although you collect a credit for selling a call spread, you’re required to put up enough cash collateral to cover the potential max loss of the spread. This collateral is netted against the amount of the credit you receive and is calculated by taking the width of the spread, subtracting the total premium collected, and then multiplying that number by 100.

Let’s say, you sell a 5-point wide call spread for $2. Because a standard option controls 100 shares of the underlying, you’ll collect $200 for selling the spread. Meanwhile, the collateral required will be $500, which is the width of the spread multiplied by 100. If you sold 10 spreads, you’d collect $2,000, but the required collateral would be $5,000, and so on.

Factors to consider

Look for an underlying stock or ETF that is trending sideways or one you think may decrease soon. Consider choosing an underlying that’s on the higher end of its implied volatility range, with potential to decrease over the life of the trade. It may be advisable to look for underlyings with more liquid options that have tighter bid/ask price spreads, larger volumes, and plenty of open interest.

Choose an expiration date that optimizes your window for success. Options expiring in 30-45 days tend to provide the best window to sell a call spread. This is when time decay begins to accelerate. If you choose a further-dated expiration, you’ll collect more premium but your capital will be tied up longer while you’re waiting for the options to decay. Meanwhile, if you choose a shorter-dated expiration, you might not receive enough premium to make the trade worthwhile.

When selecting strike prices, the most common approach is to use out-of-the-money options. Out-of-the-money calls are when the strike price is higher than the underlying stock price. This approach has the highest theoretical probability of success and can be profitable at expiration if the stock price drops, stays where it’s at, or rises slightly (as long as it stays below your short strike).

Important: It’s best to avoid selling an in-the-money call spread. In-the-money options are when the strike price is below the underlying stock price. Although you’ll collect more premium upfront, this approach has a much lower probability of success, and it might lead to an early assignment and dividend risk. Instead, you can achieve a similar risk/reward profile by buying an out-of-the-money put spread with the same strikes.

The amount of premium you collect determines the risk and reward ratio of the trade. Many traders will look to collect roughly ⅓ the width of the spread. For example, if selling a 1-point wide spread, they’d look to collect around $0.33. A 5-point spread, around $1.65. A 10-point spread, $3.33 in premium, and so on. If the potential premium collected is less than this, the reward may not be worth the risk for some. If it’s more than this ratio, it may signal that the market is pricing in more implied volatility, which is worth investigating before placing the trade. While this isn’t an absolute rule to be followed, it’s a helpful guideline.

How is a call credit spread different from selling a naked call?

A short naked call has undefined risk because the underlying stock or ETF can rise to virtually any number and so can the value of a call. Meanwhile a call credit spread contains a long call, which theoretically defines your risk. Although you collect a larger premium for selling a naked call, it comes with the risk of undefined losses, which is why you cannot use this strategy at Robinhood.

P/L Chart at expiration

A call credit spread has both defined theoretical profit and loss. At expiration, it profits if the underlying stock is trading below the breakeven price.

Theoretical max gain

The theoretical max gain is limited to the credit you receive for selling the spread. To realize a max gain, the underlying stock price must close at or below the short strike on the expiration date, and both options must expire worthless.

Theoretical max loss

The theoretical max loss is equal to the width of the spread, minus the net credit collected. If the underlying stock price closes above the strike price of the long call (the one with a higher strike price) on the expiration date, the short option will likely be assigned, and your long option will be automatically exercised. This will result in a max loss on the trade.

Breakeven point at expiration

At expiration, the breakeven point is calculated by adding the net credit collected to the strike price of the short call (the lower strike price).

Is it possible to lose more than the theoretical max loss?

Yes. If you close one leg of the spread and keep the other, the risk profile (as described earlier) no longer holds true. If you buy to close the short call, your risk will be that of a long call until expiration. If your short call is assigned, you could also realize a greater max loss on the trade.

Example

Imagine XYZ stock is trading for $99.75. The following lists the options expiring in 30 days. The options shaded in green are in-the-money and the ones shaded in white are out-of-the-money.

You’re bearish and expect XYZ stock to stay below $102 over the next 30 days. You decide to sell the $102/$105 call credit spread:

Sell 1 XYZ $102 Call for $2.80

Buy 1 XYZ $105 Call for ($1.75)

= Total net credit is $1.05

The theoretical max gain is $1.05 per share, or $105 total. This is the net credit received for selling the spread. Max gain occurs if XYZ stock closes at or below $102 at expiration, and both options expire worthless.

The theoretical max loss is $1.95 per share, or $195. It’s calculated by taking the width of the spread ($3) and subtracting the net credit received ($1.05). Max loss occurs if XYZ closes above $105 at expiration.

The breakeven point at expiration is $103.05. It’s calculated by taking the strike price of the short call ($102) and adding the net credit collected ($1.05).

This is a theoretical example. Actual gains and losses will depend on a number of factors, such as the actual prices and number of contracts involved.

Managing the trade

A call credit spread benefits if the underlying stock price stays below the strike price of your short option, time goes by, and implied volatility decreases. These outcomes would likely decrease the value of your call spread. That being said, the value of your long call will always offset the value of your short call. As a result, the total value of the spread will fluctuate at a slower rate compared to a single option strategy.

If the position is profitable, consider taking action before expiration. You can try to close the spread, or leg out by closing the short call and keeping the long call. This allows you to realize some profit on the short call, while leaving the long call intact in case the stock reverses and begins to rise. Just remember, the strategy won't approach its maximum gain or loss until it’s near expiration and the time value of both options is greatly reduced.

If the underlying stock price climbs and implied volatility rises, the value of both options will likely increase. This isn't ideal. If the spread is worth more than your original selling price, you can attempt to cut your losses and close the position before expiration. This would result in a loss on the trade.

As expiration nears, you may need to proactively manage your position if the underlying stock is trading between the strikes. If no action is taken, at expiration your short call will likely be assigned and your long call would expire worthless. This may result in a short stock position, and a potential max loss that is greater than theoretical max loss of the spread.

Keep in mind: Any time you have a short call option in your position, there’s a possibility of an early assignment, which exposes you to certain risks, like short stock or dividend risk.

Option Greeks

A call credit spread involves both a long and short call. The Greeks are netted to arrive at a net delta, gamma, theta, vega, and rho for the spread.

When the trade is established, the spread has a negative delta and a positive theta. Meanwhile, gamma and vega will be slightly negative which means the position benefits from no movement in the underlying stock and a decrease in implied volatility. Depending on where the underlying stock price is relative to either strike price, gamma, theta, and vega can be either positive or negative. Rho is essentially neutral.

Bottom line, this strategy is about delta and theta—you want the underlying stock price to decline and need time to pass.

Keep in mind: Option Greeks are calculated by using options pricing models and are theoretical estimates. All Greek values assume all other factors are held equal.

Closing the position

Although the strategy is designed to reach max profit at expiration, you might consider closing it before then in order to free up capital and avoid the risk of going through exercise and assignment. Whichever you choose, it’s best to establish an exit strategy for your trade before you enter it. To close a call credit spread you can do the following that's described in this section:

- Buy to close the spread

- Leg out of the spread

- Hold the spread through expiration

Buy to close the spread

To close your position, take the opposite actions that you took to open it. For a call credit spread, this involves simultaneously buying-to-close the short call option (the one you initially sold to open) and selling-to-close the long call option (the one you initially bought to open).

Typically, you’ll pay a net debit to close your position. In doing so, you’ll realize any profits or losses associated with the trade. If you buy to close your spread for less than you sold it for, you’ll profit. If you buy to close it for more than you sold it for, you’ll realize a loss. And if you buy to close it at the same price as your sale price, you’ll break even.

Keep in mind: Prior to expiration, you’ll unlikely be able to close the position for a max gain or max loss. In many cases, you may have to collect slightly less than theoretical value in order to close the position as expiration approaches.

Leg out of the spread

Some traders prefer to leg out of a call credit spread. You can do this by buying to close the short call option, and then selling to close the long option later, using separate orders. This approach includes both benefits and risks. You can do this to mitigate liquidity concerns or change the structure of your strategy. That being said, by doing this you could create a greater gain or loss than the max theoretical gain or loss of the original strategy.

Note: At Robinhood, to leg out of a call credit spread you must buy to close the short call option first before you can sell to close your long option.

Hold the spread through expiration

Holding your position into expiration can result in a max gain or loss scenario and carries certain risks that you should be aware of. Learn more about expiration, exercise, and assignment.

If the underlying’s price is below the short strike price, then both options should expire worthless. The options will be removed from your account and you’ll realize a max gain on the position.

If the underlying’s price is above the long strike price, both options will expire in-the-money. You’ll most likely be assigned on your short call and your long call will be automatically exercised. You’ll keep the credit received, but you’ll realize a max loss on the position.

If the underlying’s price closes above the short strike but below the long strike, your short call will likely be assigned and your long call will expire worthless. Be cautious of this scenario. If your short call is assigned you’ll be left with a short stock position, which carries undefined risk. Meanwhile, your long call will no longer exist to offset the assignment. This may potentially result in losses greater than the theoretical max loss of the call credit spread.

Important: To help mitigate this risk, Robinhood may close your position prior to market close on the expiration date; however, this is done on a best-effort basis. Ultimately, you are fully responsible for managing the risk within your account.

Additional risks

For call credit spreads, be cautious of an early assignment or an upcoming dividend.

An early assignment occurs when an option that was sold is exercised by the long holder before its expiration date. If you’re assigned on your short call, you can take one of the following actions by the end of the following trading day:

- Buy the shares at the current market price

- Exercise your long call (thereby buying the shares at the long strike price and realizing a max loss)

In either circumstance, your individual investing account may temporarily display a reduced buying power or an account deficit as a result of the early assignment. An exercise of the long call is typically settled within 1-2 trading days, and restores buying power partially or fully. To learn more, see Early assignments.

Dividend risk is the risk that you’ll be assigned on your short call option the night before the ex-dividend date (where you have to pay the dividend to the exerciser). This is one of the biggest risks of trading spreads with a short call option, which could result in a greater loss (or lower gain) than the theoretical max gain and loss scenarios, as described earlier. Traders can avoid this by closing their position during regular trading hours prior to the ex-dividend date. To learn more, see Dividend risks.

What happens if there’s a corporate action on the underlying asset?

Sometimes, the option’s underlying stock can undergo a corporate action, such as a stock split, a reverse stock split, a merger, or an acquisition. Any corporate action will impact the option you hold, potentially resulting in changes to the option, such as its structure, price, and deliverable.

Put debit spread

What’s a put debit spread?

A put debit spread is one type of vertical spread. It’s a bearish, two-legged options strategy that involves buying a put option and selling another with a lower strike price. Both options have the same expiration date and underlying stock or ETF. This strategy is also known as a long put vertical, long put spread, or bear put spread.

A put debit spread is a premium buying strategy. Typically, the debit you pay for buying the higher-strike put is greater than the credit you’ll receive for selling the lower-strike put. Therefore, you’ll pay a net debit to open the position. It’s called a spread because the value of the position is based on the difference, or spread, between the strike prices.

When to use it

A put debit spread is a bearish strategy because ideally you want the price of the underlying to fall below the short strike. You might consider a put debit spread when you’re bearish, but believe the downside move will be limited. If you’re extremely bearish, buying a put may provide a more desirable profit potential.

Compared to a long put, a put debit spread is less expensive. In a sense, the short put helps finance the purchase of the long put. This limits the theoretical max gain, but increases your probability of success by raising the breakeven price the stock needs to fall to by expiration. The tradeoff is your potential profit is much lower, whereas buying a put offers a larger profit potential but has a lower probability of success.

Building the strategy

To buy a put spread, pick an underlying stock or ETF, select an expiration date, and choose the strike prices. Typically, a put debit spread is constructed in one of two ways:

- Buying an in-the-money put option and selling an out-of-the-money put option (called an “in and out” spread)

- Buying and selling two out-of-the-money put options

Debit spreads traded simultaneously using a spread order. A spread order is a combination of individual orders, known as legs. The combined order is sent and both legs must be executed simultaneously on one exchange. You can also leg into the strategy by opening one leg first and the other later using individual orders. This is a more complicated approach and carries certain risks.

The width of the spread is the distance between the short and long strike prices and is a key detail. A narrower spread has a lower potential profit but requires less collateral and has less theoretical risk. Meanwhile, a wider spread has a higher potential profit but is more expensive and has greater theoretical risk.